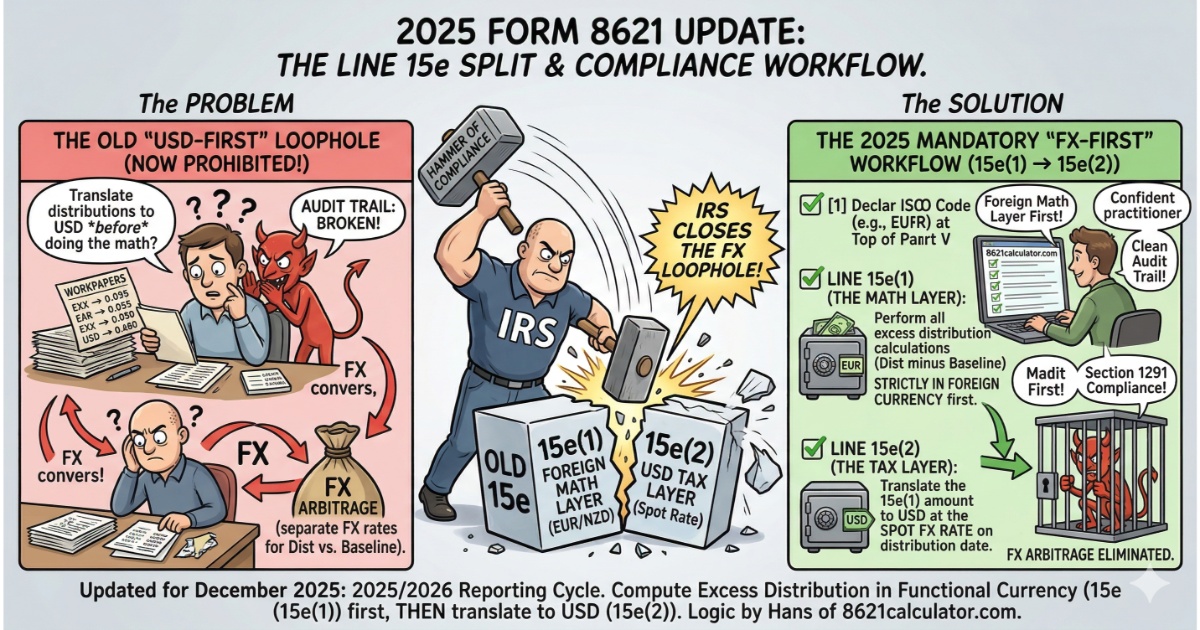

💡 Key Takeaways: Form 8621 Line 15e Compliance

- The 2025 Revision: Line 15e is now split into 15e(1) (Math Layer in foreign currency) and 15e(2) (Tax Layer translated to USD), strictly enforcing the currency sequence.

- Functional Currency First: If distributions are paid in a foreign currency, you must perform the entire calculation up to Line 15e(1) in that currency to comply with IRC §1291(b)(3)(E).

- Spot Rate Translation: Excess distribution amounts must be translated into USD at Line 15e(2) using the exact transaction-date spot rate as supported by IRC §989(b)(1).

- Elections E/G/H Routing: Deemed dividends from purging elections bypass the 125% historical averaging test and flow directly into Line 15e(2) in USD.

Form 8621 Line 15e Architecture: The Part V §1291 Calculation Chain

USD vs. Foreign Currency: When Can Line 15e(1) Skip Translation?

Only if the PFIC actually distributed the cash in US Dollars.

IRC §1291(b)(3)(E) mandates that the §1291 determination be made in the functional currency. You must perform the entire computation through Line 15e(1) in the declared foreign currency, translating to USD only at Line 15e(2) using the distribution-date spot rate.

The math is simplified. Enter "USD" as the Currency Code. Complete Lines 15a through 15e(1) in USD, and simply carry the exact same amount down to Line 15e(2).

Purging Elections (E, G, H): Why Deemed Dividends Bypass Line 15a

Three specific Part II elections bypass the Lines 15a through 15e(1) reporting sequence entirely, routing directly to Line 15e(2). This is one of the most misunderstood routing mechanics in the 2025 form structure.

- Election E (Deemed Dividend, QEF transition): "Enter the excess distribution on line 15e(2) of Part V."

- Election G (Deemed Dividend, former PFIC): "Enter the excess distribution on line 15e(2), Part V."

- Election H (§1298(b)(1) deemed dividend): "Enter the excess distribution on line 15e(2), Part V."

Elections E, G, H vs. Actual Distributions: Line 15e Routing Table

| Event Type | Description | Bypasses 15a–15e(1)? | Enters On | Currency |

|---|---|---|---|---|

| Election E | Deemed dividend on QEF transition (purging election) | Yes — Complete bypass | Line 15e(2) directly | USD |

| Election G | Deemed dividend under former PFIC rules | Yes — Complete bypass | Line 15e(2) directly | USD |

| Election H | Deemed dividend under PFIC-to-CFC transition rules | Yes — Complete bypass | Line 15e(2) directly | USD |

| Election F | Deemed sale — transition to QEF or MTM | Yes — Bypasses 15e entirely | Line 15f directly | USD |

| Actual Distributions | Cash or DRIP dividends received during the year | No — Must flow through the 125% test | Line 15a → 15e(1) | Declared currency → Translated at 15e(2) |

Form 8621 Line 15e(2) Translation: Distribution-Date Spot Rate Requirements

IRC §1291(b)(3)(E) provides the direct PFIC rule: if distributions are received in a foreign currency, the §1291 determination must be made in that currency, and the excess distribution determined in that currency is then translated into U.S. dollars.

Line 15e(2) is the translation point. After Line 15e(1) determines the excess distribution in the declared currency, that amount is translated into USD for the Line 16 allocation.

IRC §989(b) supports using the spot rate on the distribution date for an actual distribution. This is why a distribution-date spot rate is stronger than an annual average rate, year-end rate, or blended rate.

Applying Spot Rates to Multiple Distribution Dates: Per-Transaction Accuracy

Each distribution included in Line 15e(2) should be translated into USD using the spot rate on the date of receipt, rather than any averaged or period-based rate.

The 8621calculator.com engine follows this transaction-date methodology by applying verifiable daily FX rates (e.g., OANDA historical rates) to each distribution event.

| Rate Type | Appropriate for Line 15e(2)? |

Authority / Basis | Risk if Used |

|---|---|---|---|

| Daily spot rate on exact transaction date | ✔ Yes — Most Defensible | IRC §989(b); Reg. §1.985-1(c)(6) | Correct approach when properly documented |

| Treasury annual average rate | ✖ Not appropriate | — | Does not reflect transaction-date realization; May overstate or understate USD excess distribution |

| Annual average rate (OANDA / Bloomberg) | ✖ Not appropriate | — | Still a blended rate, not transaction-specific; Same distortion risk as Treasury average |

| Year-end rate | ✖ Not appropriate | — | Mismatches timing of income recognition; Can materially distort §1291 allocation and interest |

| Verifiable daily rate source (OANDA, Bloomberg, bank feed) | ✔ Acceptable | Supports transaction-date translation | Must retain supporting documentation |

Why Line 15e(1) May Result in Zero: Three Legal Excess Distribution Scenarios

The Form 8621 instruction provides that if Line 15e(1) is zero or less, and no disposition occurred, the remainder of Part V is not completed.

However, a zero result at Line 15e(1) can arise from different legal conditions, each with distinct implications.

| Cause of 15e(1) = 0 | Legal Basis | Meaning | Form 8621 Action | §1291 Impact |

|---|---|---|---|---|

| Line 15a ≤ Line 15d | IRC §1291(b) | Current distribution is a non-excess distribution under the 125% test | Stop at Line 15e(1) | No §1291 tax or interest; reported as ordinary income |

| First Year of Holding | IRC §1291(b)(2)(B) | Statute prohibits excess distributions in the initial year | Stop at Line 15e(1) | No §1291 tax or interest; reported as ordinary income; cost basis and distribution history carry forward for future §1291 calculations |

| Zero Distributions | N/A | No triggering event occurred during the tax year | Do not complete Part V (unless disposition applies) | No income or §1291 exposure for the year |

Not all zero results at Line 15e(1) are the same.

- 125% test → non-excess distribution

- First-year rule → excess disallowed by statute

- No distribution → no triggering event

Although Part V stops in all cases, the legal basis differs, which affects how amounts are treated elsewhere in the return.

Part V stops ≠ no income.

Amounts reported on Line 15a are generally treated as ordinary income and must still be reported on

Form 1040 (e.g., dividend reporting lines).

The Calculation Pipeline: Flowing Line 15e(2) into the Line 16 Lookback Allocation

Line 15e(2) is the final output of the excess distribution determination. It is the USD amount used in the §1291 lookback computation at Line 16.

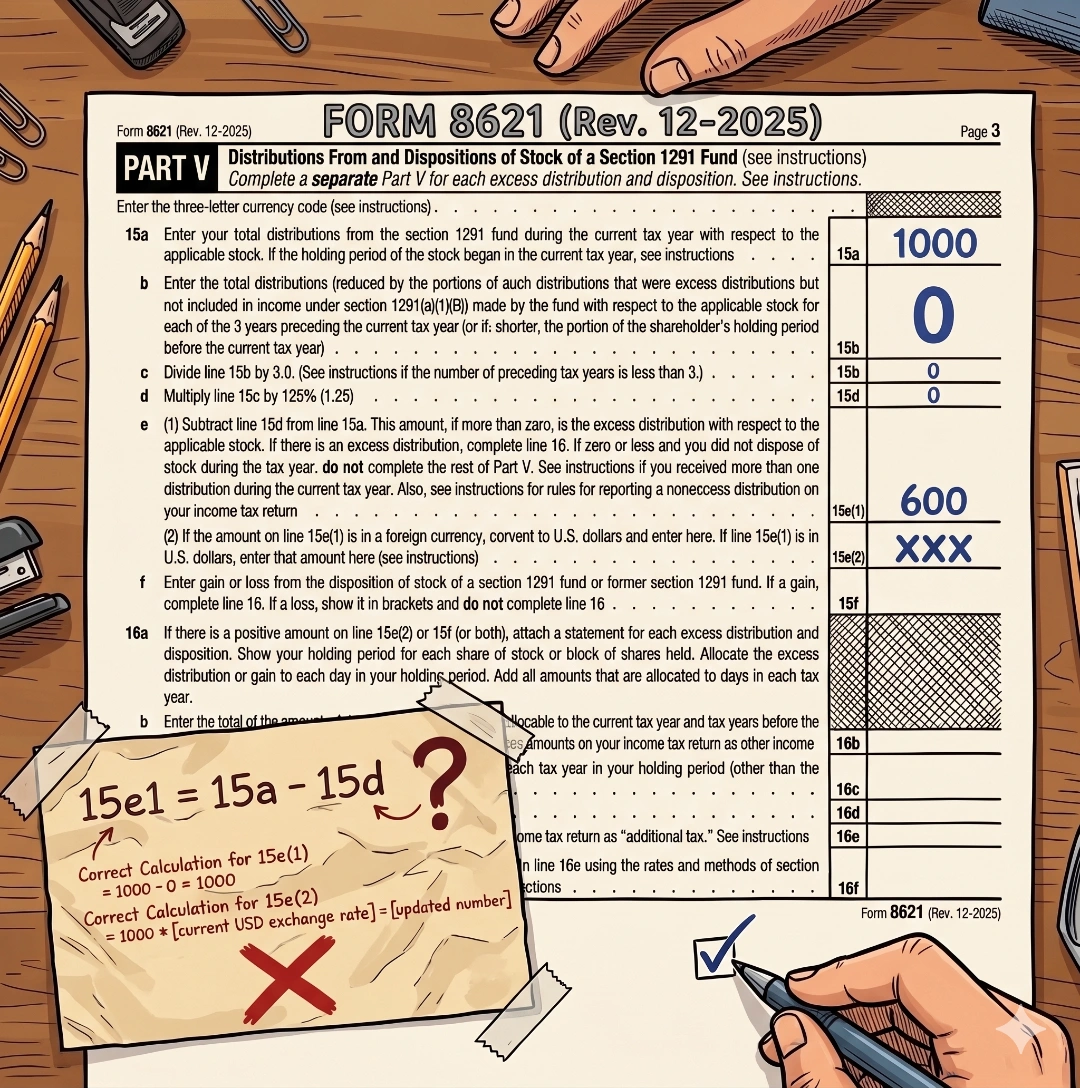

The "Reporting Gap": Why Line 15e(1) ≠ Line 15a minus Line 15d

A common error among practitioners is assuming that Line 15e(1) = Line 15a − Line 15d as a single annual total.

The problem is not the subtraction itself; Form 8621 performs this subtraction at Line 15e(1). The problem is performing that subtraction on a single annual aggregate when the §1291 rules require share-by-share or same-holding-period block computations.

IRC §1291(b)(3)(A) requires the determination to be made on a share-by-share basis, although shares with the same holding period may generally be grouped.

This statutory filter is the primary cause of the "gap." It dictates that any lot acquired in the current tax year produces zero excess distribution, regardless of the distribution amount.

Case Study: Per-Lot Line 15e(1) Calculation with First-Year Exclusion

You have the following activity:

| Date | Details | Units | Value |

|---|---|---|---|

| 2024-01-15 | Purchase | 200 | 500 |

| 2024-05-15 | Purchase | 200 | 600 |

| 2024-09-15 | Purchase | 200 | 600 |

| 2025-05-15 | Purchase | 200 | 700 |

| 2025-09-15 | Purchase | 200 | 700 |

| 2025-12-15 | Distribution | — | 300 |

Step 1 — Total holdings at distribution date

Total units: 200 × 5 = 1,000 units

Step 2 — Allocate distribution per unit

2025-12 Distribution: 300

Per unit distribution: 300 ÷ 1,000 = 0.30

So each 200-unit lot receives → 200 × 0.30 = 60

Step 3 — Form 8621 Per-Lot Structure

| Lot | Purchase Date | Units | Distribution Allocation |

Holding Year |

15d (Threshold) |

15e (Excess) |

|---|---|---|---|---|---|---|

| Lot 1 | 2024-01-15 | 200 | 60 | 1 | 0 | 60 |

| Lot 2 | 2024-05-15 | 200 | 60 | 1 | 0 | 60 |

| Lot 3 | 2024-09-15 | 200 | 60 | 1 | 0 | 60 |

| Lot 4 | 2025-05-15 | 200 | 60 | 0 | — | 0 |

| Lot 5 | 2025-09-15 | 200 | 60 | 0 | — | 0 |

Step 4 — Apply §1291 rules (The Result)

- Line 15a = 300

- Old lots portion = 60 × 3 = 180

- Current-year lots portion = 60 × 2 = 120

Maximum 180

At most 180 can enter the 15e(1) excess distribution test. (Subject to the 125% historical average test).

Zero Excess

Per §1291(b)(2)(B), the 120 cannot produce excess distribution in the first year of the holding period.

Line 15a shows the full 300 distribution, but only the 180 allocated to pre-2025 lots can enter the §1291 excess-distribution test. The 120 allocated to 2025 lots is ordinary income, not excess distribution.

In short, that missing 120 is:

- ✔️ included in Line 15a

- ❌ excluded from Line 15e(1)

- ✔️ treated as ordinary income

The First-Year Exclusion (§1291(b)(2)(B)) dictates that current-year lots must be excluded from Line 15e(1) but remain fully taxable as ordinary dividends on Form 1040.

Technical Audit: Systematic Form 8621 Line 15e Calculation Errors

What Happens: Current-year lots incorrectly generate excess distributions because aggregation ignores holding-period structure.

Direction: Excess overstated.

Fix: Compute per lot first, then aggregate. Excess must be determined at the lot level. First-year lots must contribute zero to Line 15e.

What Happens: USD excess distorted because distributions are translated using averaged rates instead of transaction-date rates.

Direction: Either direction.

Fix: Use daily spot rate (e.g., OANDA) for each distribution date. §1291 excess distributions are transaction-based, not annual aggregates.

What Happens: Artificial gain/loss created from FX movement; excess amount becomes dependent on exchange rate choice rather than economic distribution.

Direction: Either direction.

Fix: Perform all computations through Line 15e(1) in the declared Line 15e(1) computation currency; translate to USD only at Line 15e(2).

What Happens: Deemed dividends from purging elections (E, G, or H) are incorrectly subjected to the 125% historical average test. Most commercial tax software packages fail this by dumping everything onto Line 15a, triggering a cascading failure of the excess distribution logic.

Direction: Architectural Logic Failure.

Fix: Per Form 8621 instructions, deemed dividends from purging elections flow directly into Line 15e(2). They completely bypass the 125% test logic of Lines 15a–15d. Mastery of this routing anomaly is a key indicator of expert-level PFIC architectural knowledge.

What Happens: Multiple distributions translated at an incorrect uniform rate, ignoring timing differences.

Direction: Either direction.

Fix: Apply one spot rate per distribution date. Example: four quarterly distributions → four FX rates → sum USD excess.

What Happens: IRS cannot verify holding-period allocation of excess distribution.

Direction: Filing exposure.

Fix: Provide a detailed allocation statement (Line 16a support) whenever Line 15e(2) or Line 15f is positive.

What Happens: §1291 methodology incorrectly applied to funds under a different regime.

Direction: Wrong regime.

Fix: QEF → Part III (Lines 6a–7c); MTM → Part IV (Lines 10–14); Line 15e applies only to §1291 funds (Part V).

All Line 15e errors share the same root cause: failure to respect the three structural rules of §1291 computation:

- Lot-level determination precedes aggregation.

- Distributions are transaction-based, not annual totals.

- Currency translation occurs only after excess is determined.

Any system that violates one of these will produce systematically incorrect Line 15e results.

Practitioner FAQ: Form 8621 Line 15e & §1291 Compliance

Why is Form 8621 Line 15e lower than Line 15a minus Line 15d?

Does Form 8621 Line 15e(2) round to a whole dollar or include cents?

How do I calculate Line 15e if my PFIC distributes in multiple currencies?

Do monthly PFIC distributions require 12 separate Form 8621 Line 16a statements?

If Line 15e(2) is zero but Line 15f is positive, is the Line 16a allocation still required?

Can a late QEF or MTM election avoid §1291 Line 15e excess distribution tax?

What is the difference between Line 15e(1) and Line 15e(2) on the 2025 Form 8621?

How does a purging election (like Election E, G, or H) route on Form 8621 relative to Line 15e?

Can I use the IRS annual average exchange rate to translate Line 15e(1) into Line 15e(2)?

If my PFIC had zero distributions during the year, do I still need to calculate Line 15e?

Official Sources and References

- 🔗 IRS Form 8621 (PDF): Official IRS PDF form for Passive Foreign Investment Company reporting.

- 🔗 Instructions for Form 8621 (PDF): Official IRS instructions for completing Form 8621.

- 🔗 IRC §1291: Statutory tax rules for PFIC excess distributions and interest calculations.

- 🔗 IRC §989(b)(1): Statutory spot rate translation rules for actual distributions.

- 🔗 IRC §6621: Compounded interest rate rules on underpayment and PFIC deferrals.

Current as of May 2026 · Based on Form 8621 (Rev. 12/2025)