💡 Key Takeaways: Form 8621 Line 16a Compliance

- Filing Mandate: A detailed Line 16a statement is mandatory if you report a positive amount on Line 15e(2) (excess distribution) or Line 15f (disposition gain).

- Statute of Limitations Risk: Missing or incomplete Line 16a attachments may suspend the audit statute of limitations under IRC §6501(c)(8).

- Lot-Level Precision: Recomputing throwback taxes requires lot-by-lot holding period counts (excluding acquisition date, including payment date) rather than average pooling.

- Due-Date Anchors: Interest start dates must track exact statutory due dates, factoring in weekend shifts under IRC §7503 and historical IRS COVID postponements.

What Is Form 8621 Line 16a?

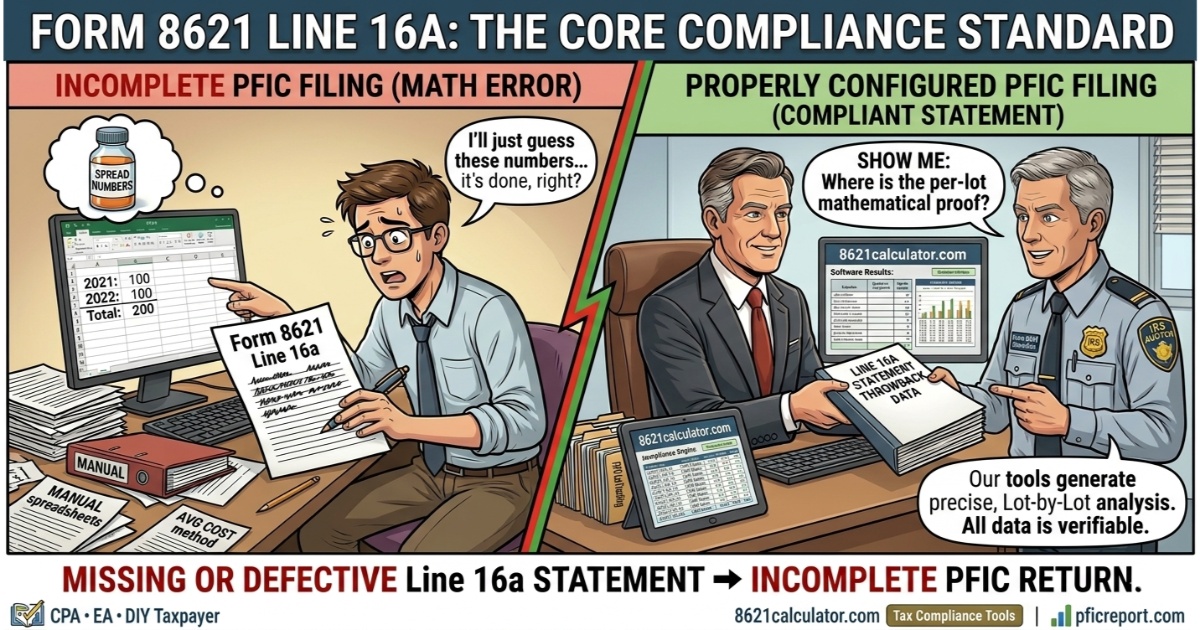

The practical audit standard is recomputability. A Line 16a statement should not merely state a final tax amount. It should show enough lot-level and year-by-year detail for the computation to be independently checked.

Form 8621 Line 16a refers to the required attached statement supporting the Part V §1291 computation. It is required when a PFIC shareholder reports a positive amount on:

- Line 15e(2), excess distribution amount, or

- Line 15f, gain on disposition.

The statement must show:

- the holding period for each share or qualifying block;

- the daily allocation of the excess distribution or gain across that holding period; and

- the annual aggregation of those daily allocations by tax year.

Those annual allocation amounts then support the deferred tax and §6621 interest computations reported on the later Part V lines.

Why Line 16a Is Mandatory

The IRS Instructions require a statement for each excess distribution and disposition when Line 15e(2) or Line 15f is positive.

A compliant statement must disclose:

| Requirement | Meaning | Common Failure |

|---|---|---|

| Statement attached | Separate Line 16a schedule must be included | Only entering totals on Form 8621 |

| Per-share or per-block holding period | Each lot must be traceable | Aggregating all shares by year |

| Daily allocation | Allocation must be by day, not rough annual split | Using yearly percentages |

| Annual aggregation | Daily amounts must be totaled by tax year | No recomputable year-by-year table |

How to Calculate the §1291 Throwback Formula for Line 16a

Line 16a is a mandatory disclosure that provides the mathematical proof of your §1291 computation. The statement should show that the excess distribution or disposition gain was allocated ratably to each day in the holding period and then aggregated by tax year.

For each year in the holding period, the allocation is:

1. Precision Day-Count (The "Exclude Start" Rule)

For a recomputable §1291 statement, follow the Form 8621 day-count logic: exclude the acquisition date, but include the distribution or disposition date.

Sample Case (Buy 07/15/2019 | Sell or Distribution 03/28/2023):

- Total Days Held: 1,352 Days

- 2019 Days: 169 (Excludes 07/15)

- 2020 Days: 366 (Leap Year)

| Year | Days | Start* | End |

|---|---|---|---|

| 2019 | 169 | 2020-07-15 | 2024-04-15 |

| 2020 | 366 | 2021-05-17 | 2024-04-15 |

| 2021 | 365 | 2022-04-18 | 2024-04-15 |

| 2022 | 365 | 2023-04-18 | 2024-04-15 |

| 2023 | 87 | Current | - |

2. Why these dates are mandatory for Audit Defense:

- Interest Start: Interest should be computed using the statutory due-date framework for the tax year to which the prior-year allocation is assigned. For 2019 and 2020, COVID-postponed federal due dates must be considered; for later years, IRC §7503 weekend and holiday shifts may also affect the due-date anchor.

- Interest End: For a 2023 disposition, interest accrues until the due date of the 2023 return (04/15/2024).

- Anti-Pooling: If you have multiple lots (e.g., from 2019 and 2021), do not combine them. Each lot must have its own independent table with specific Interest Start/End windows to avoid "phantom interest" on newer shares.

| Audit Check | Common Preparer Error | 8621calculator / Line 16a Standard |

|---|---|---|

| Start Date | Fixed April 15 | Statutory Shifts (COVID & §7503) |

| End Date | Sale Date | Tax Return Due Date (04/15/2024) |

| Lot Logic | Pooled Gains | Independent Per-Lot Allocation |

Multiple Distributions & Dispositions

Line 16a is a required supporting statement, not a summary line. To ensure the §1291 computation is verifiable, the attachment must maintain strict separation for each event.

Per-Distribution

Each excess distribution within the same tax year should be supported by its own Line 16a calculation, because each distribution has its own measurement date and §1291 allocation period ending on that distribution date.

Per-Lot Disposition

Each acquisition lot must be calculated and disclosed separately. Each lot has its own acquisition date, holding period, and allocation profile.

Current-Year vs Prior-Year Treatment

The Line 16a statement produces annual allocation amounts. Form 8621 then separates those amounts between current-year / pre-PFIC-year amounts and prior PFIC-year amounts on later lines:

| Portion | Treatment |

|---|---|

| Current-year / pre-PFIC-year allocation | Treated under Line 16b; no §6621 throwback interest |

| Prior PFIC-year allocation | Taxed at the highest marginal rate for each historical year; §6621 interest applies |

This separation is where many manual spreadsheets fail, especially when aggregating lots incorrectly.

Historical Highest Tax Rates

For prior PFIC years, IRC §1291(c)(2) uses the highest rate in effect for that year.

| Years | Highest Individual Rate |

|---|---|

| 2018–present | 37% |

| 2013–2017 | 39.6% |

| 2003–2012 | 35% |

| 2002 | 38.6% |

| 2001 | 39.1% |

| 1993–2000 | 39.6% |

For older holding periods, use the highest rate applicable to each specific tax year, not a broad range estimate.

Why FIFO and Lot-Level Tracking Matter

Line 16a cannot be computed correctly unless the preparer identifies exactly which shares were sold. Unless the taxpayer has contemporaneous specific-identification records, FIFO is generally the most audit-defensible method for dispositions. This is a reconstruction convention rather than a special PFIC-specific ordering rule.

Each lot has its own:

- acquisition date

- basis

- holding period

- days allocated to each year

- deferred tax and §6621 interest chain

Pooling lots destroys this required mathematical accuracy.

In practice, preparers may use labels such as "Various" or "Multiple" when multiple acquisition dates are involved. The critical issue is not the label, but whether the attached Line 16a statement provides clear lot-level support.

Foreign Currency and Line 16a

Line 16a must be presented in USD, but the underlying computation must remain traceable to the original foreign-currency transactions.

For dispositions, basis and proceeds should be translated separately at the spot rates on their respective transaction dates. Each lot must retain its own currency history and conversion.

For foreign-currency distributions, do not simply convert every input to USD first if the Form 8621 foreign-currency rule applies. When the relevant distributions are made in a single foreign currency, the excess distribution should be determined in that currency first, and each ratable portion should then be translated into USD using the spot rate on the distribution date.

The key requirement is consistency and traceability. The IRS must be able to reconcile each USD amount in the Line 16a statement back to the original foreign-currency transaction and its corresponding exchange rate.

Worked Example: Two PFIC Lots Sold in 2024

Assume the following transaction details:

| Lot | Purchase Date | USD Basis | Sale Proceeds | Gain |

|---|---|---|---|---|

| Lot A | 2021-03-15 | $20,769 | $22,952 | $2,183 |

| Lot B | 2022-03-15 | $19,602 | $22,952 | $3,350 |

Total §1291 gain: $2,183 + $3,350 = $5,533

Lot A Allocation

| Year | Days | Allocation | Rate | Deferred Tax |

|---|---|---|---|---|

| 2021 | 292 | $465 | 37% | $172 |

| 2022 | 365 | $581 | 37% | $215 |

| 2023 | 365 | $581 | 37% | $215 |

| 2024 | current year | $556 | - | - |

Lot B Allocation

| Year | Days | Allocation | Rate | Deferred Tax |

|---|---|---|---|---|

| 2022 | 292 | $973 | 37% | $360 |

| 2023 | 365 | $1,217 | 37% | $450 |

| 2024 | current year | $1,160 | - | - |

Line Mapping

| Form 8621 Line | Result |

|---|---|

| Line 16a | Attached statement showing day-by-day allocation |

| Line 16b | Amount allocated to current tax year and pre-PFIC years |

| Line 16c | Aggregate increase in tax for prior PFIC years |

| Line 16d | Foreign tax credit allowed for prior PFIC years |

| Line 16e | Net additional §1291 tax after Line 16d credit |

| Line 16f | §6621 interest on the Line 16e prior-year tax |

The worked-example version is the strongest conversion engine because it shows exactly why a manual or software-only Form 8621 entry is not enough.

CPA / EA Audit Risk

A defective Line 16a statement can create three levels of risk:

1. Calculation Risk

Wrong allocation, wrong rate, wrong interest start date, or wrong lot matching.

2. Disclosure Risk

The statement is missing or not recomputable.

3. Statute Risk

Under IRC §6501(c)(8), failure to furnish required PFIC information may keep the statute of limitations open for the entire return.

Common Line 16a Mistakes

| Mistake | Why It Matters |

|---|---|

| No Line 16a attachment | May make the Form 8621 Part V disclosure incomplete |

| Using annual allocation only | Skipping the daily allocation step and jumping directly to rough year percentages |

| Pooling unrelated lots | Blends different holding periods and can distort the annual allocation |

| Using average cost without lot support | May fail to preserve the actual holding period for each share block |

| Wrong current-year allocation | Misstates Line 16b |

| Wrong historical highest tax rate | Misstates Line 16c |

| Missing or incorrect foreign tax credit allocation | Misstates Line 16d |

| Treating Line 16e as current-year income tax | Line 16e is additional tax, not the current-year allocation |

| Wrong interest start or end date | Misstates Line 16f |

| No §6621 / daily-compounding support | Weakens or understates the Line 16f interest calculation |

| Missing PFIC reference ID or entity details | Makes the attachment harder to match to the reported PFIC |

| Failing to carry Line 16e and Line 16f to the correct tax return lines | Creates a Form 1040 reporting error |

CPA-Ready Line 16a Statement Template

A Line 16a statement should let a reviewer trace the amount reported on Line 15e(2) or Line 15f through the §1291 allocation and reconcile it to Lines 16b–16f.

1. Taxpayer / PFIC Information

- Taxpayer name and TIN

- Tax year

- PFIC name and reference ID

- Currency and FX source, if applicable

2. Event Summary

- Event type: excess distribution or disposition gain

- Source line: Line 15e(2) or Line 15f

- Transaction date

- Total USD amount subject to §1291 allocation

3. Lot-Level Allocation

- Lot ID

- Acquisition date

- Distribution or disposition date

- Units

- Total days held

- Amount allocated to each year

4. Prior-Year Tax and Interest

- Prior PFIC year

- Allocation to that year

- Highest tax rate for that year

- Increase in tax

- Foreign tax credit, if any

- §6621 interest

5. Reconciliation to Form 8621

- Line 16b: Amount allocated to the current tax year and pre-PFIC years

- Line 16c: Aggregate increase in tax for prior PFIC years

- Line 16d: Aggregate foreign tax credit for prior PFIC years

- Line 16e: Additional tax = Line 16c − Line 16d

- Line 16f: Interest under §6621

Download the Excel Template

Use a downloadable Excel template to create a recomputable Line 16a statement showing FIFO lot register, daily allocation, annual aggregation, historical tax rate, §6621 interest, and Form 8621 line mapping.

⚠️ Practitioner Note:

This Excel template is designed to illustrate the mechanics of §1291 allocation, including day-count logic and annual aggregation.

In practice, real client cases often involve multiple acquisition lots, distributions, and statutory date adjustments. These scenarios require precise day-level allocation and interest computations.

For production use, many practitioners rely on specialized tools to ensure recomputability and consistency across multi-year PFIC calculations.

Generate the Statement Automatically

Manual Line 16a preparation is difficult because it requires:

- per-lot tracking

- day-count allocation

- historical tax rates

- §6621 / §6622 interest

- FX translation

- current-year separation

- Form 8621 line mapping

FAQ: Form 8621 Line 16a & PFIC Reporting

Why is Line 16a considered a major compliance risk in PFIC reporting?

Do I only need a Line 16a statement if I have a recognized gain?

Can a missing Line 16a statement be fixed by simply mailing the schedule?

Why is the average cost method generally not used on a Line 16a statement?

How do leap years affect the Line 16a allocation?

Can I use my actual historical tax bracket for the Line 16c calculation?

Can net operating losses (NOLs) from prior years reduce the §1291 throwback tax?

Generally, no. The prior-year portion of a §1291 excess distribution is not recomputed as ordinary taxable income on the historical return. Instead, Form 8621 applies a separate deferred-tax calculation: the amount allocated to each prior PFIC year is taxed at the highest marginal rate in effect for that year, and the result is reported as additional tax on the current return.

Therefore, a taxpayer’s historical NOLs generally do not offset the Line 16c/16e throwback tax computation.

For practitioners, this is a common error: the Line 16a statement should show the §1291 allocation, the highest-rate tax calculation, and the resulting additional tax separately from the taxpayer’s regular historical taxable-income or NOL computation.

When does the IRC §6621 interest start accruing for prior-year allocations?

Do the 2020 and 2021 COVID tax deadline extensions affect the §6621 interest period?

How must §6622 daily compounding be handled?

When should foreign currency (FX) be converted in the §1291 calculation?

Distributions: Determine the excess distribution in the declared foreign currency first, then translate the excess amount to USD using the spot rate on the distribution date.

Dispositions: Translate your basis using the historical spot rate on the acquisition date, and translate your proceeds using the spot rate on the disposition date. Use the resulting USD gain for the Line 16a allocation.

If I sold multiple lots of a PFIC, do I need to detail each lot?

What is the "Various" date issue in PFIC reporting?

What if my professional tax software cannot generate the Line 16a attachment?

Why might a Line 16f total differ slightly from manual calculations?

Do I need a Line 16a statement if I made a valid QEF or MTM election?

Official Sources and References

- 🔗 IRS Form 8621 (PDF): Official IRS PDF form for Passive Foreign Investment Company reporting.

- 🔗 Instructions for Form 8621 (PDF): Official IRS instructions for completing Form 8621.

- 🔗 IRC §1291: Statutory tax rules for PFIC excess distributions and interest calculations.

- 🔗 IRC §6501(c)(8): Indefinite statute of limitations rules for unfiled foreign assets.

- 🔗 IRC §6621: Compounded interest rate rules on underpayment and PFIC deferrals.

Current as of May 2026 · Based on Form 8621 (Rev. 12/2025)