Why New Zealand KiwiSaver, PIE Funds, and NZ ETFs Create PFIC Risk

Locally, KiwiSaver and PIE funds look completely harmless because the tax is handled seamlessly inside the wrapper at your Prescribed Investor Rate (PIR).

The U.S. tax risk triggers when the product is treated as a foreign corporation and its income or assets are primarily passive. Whether you hold a balanced KiwiSaver option, a PIE managed fund, an NZX ETF, or an investment option, the holding can fall into PFIC review territory.

The U.S. tax code does not treat PIR or PIE status as controlling PFIC classification. If the underlying fund pools money to invest in passive assets—like shares or bonds—the IRS may review the underlying pooled fund arrangement under PFIC rules. New Zealand tax-advantaged status does not control the U.S. result.

Start with: What Is a PFIC?

New Zealand PFIC Risk Matrix: KiwiSaver, PIE Funds, Smartshares ETFs and Term PIEs

Use the matrix to classify the holding before analyzing Form 8621.

| New Zealand Asset / Platform | PFIC Risk | U.S. Form 8621 Issue |

|---|---|---|

| KiwiSaver fund options — ANZ, ASB, BNZ, Westpac, Milford, Fisher Funds, Simplicity | 🔴 | Wrapper classification first; pooled assets commonly trigger §1297 review. |

| PIE managed funds — Kernel, InvestNow, Milford, Fisher Funds, AMP | 🔴 | Foreign pooled fund earning passive income; individual lots need review. |

| Smartshares / NZX ETFs — USF, FNZ, TWF, NZG, NZX50 | 🔴 | NZ fund wrapper domicile commonly overrides underlying U.S. index exposure. |

| Kernel funds — S&P 500, Global 100, NZ 50 | 🔴 | PIE fund structure requires entity-classification and annual PFIC review. |

| Simplicity investment funds | 🔴 | Diversified trust structures require fund-of-funds analysis. |

| Sharesies holding NZ-domiciled funds | 🔴 | Custodian wrapper does not shield underlying NZ PFIC assets. |

| Term PIE deposits — ANZ, ASB, BNZ, Westpac | 🟡 | PIE wrapper and entity classification require review; not the same as an ordinary bank term deposit. |

| KiwiSaver first-home withdrawal | 🟡/🔴 | Withdrawal may create redemption, distribution, or disposition analysis depending on the underlying fund and U.S. classification. |

| KiwiSaver fund switch — Growth to Balanced / provider transfer | 🔴 | Switch may trigger unit redemption and acquisition lot-level review. |

| PIE unit cancellations for PIR tax or fees | 🔴 | May require lot-level disposal, redemption, or basis analysis for Form 8621. |

| Direct NZX operating shares — Mainfreight, Spark, Infratil, Meridian | 🟢 | Usually lower PFIC risk; investment-heavy companies still require review. |

| U.S.-domiciled ETFs through Hatch / Sharesies / Stake — VOO, VTI, IVV | 🟢 | U.S. fund domicile; generally outside PFIC rules. |

| Ordinary NZ bank term deposits / savings accounts | 🟢 | Not a PFIC; interest remains reportable on Form 1040. |

| Direct residential property | 🟢 | Direct real estate is not a foreign corporation. |

New Zealand Fund PFIC Examples: KiwiSaver, Smartshares USF, Kernel, Simplicity and PIE Funds

Common NZ-listed pooled funds and their U.S. tax classification. Domicile drives the PFIC status, not the exchange or index.

| NZ fund / product | Common use | PFIC issue |

|---|---|---|

| Smartshares USF | S&P 500 exposure | NZ-domiciled fund, commonly requires PFIC review; not VOO or SPY |

| Smartshares FNZ | NZ Top 50 exposure | NZ fund wrapper, requires PFIC review |

| Smartshares TWF | Total world exposure | NZ-domiciled pooled fund, PFIC review |

| Smartshares NZG | NZ government bond exposure | Bond fund wrapper, requires PFIC review |

| Kernel S&P 500 Fund | U.S. equity exposure | NZ PIE fund wrapper; not a U.S. ETF |

| Kernel Global 100 | Global equity exposure | PIE managed fund review and lot basis data |

| Simplicity Growth / Balanced / Conservative | Diversified fund option | Fund-of-funds structure and PIE data tracking issues |

| ANZ / Milford / Fisher KiwiSaver Growth Funds | Retirement savings | KiwiSaver wrapper plus underlying fund-level PFIC review |

| Term PIE deposit | Cash-like return | PIE wrapper classification matters for PFIC status |

Smartshares USF vs VOO: Same S&P 500 Exposure, Different PFIC Result

Smartshares USF and VOO may both track the S&P 500, but they are different tax objects. USF is a New Zealand-domiciled fund and commonly requires PFIC review. VOO is a U.S.-domiciled ETF and is generally not PFIC stock. The exchange, index, and economic exposure do not decide the result. Fund domicile and U.S. tax classification do.

KiwiSaver and PFIC: Retirement Wrapper, Fund Options and Form 8621

KiwiSaver should not be analyzed as a simple retirement account or ordinary brokerage account. The first U.S. question is how the KiwiSaver arrangement is classified. Only after the account, ownership, contribution, and treaty position are reviewed can the underlying fund options be tested for PFIC exposure. Employer contributions, government contributions, fund switches, provider transfers, and first-home withdrawals may all affect the U.S. workpaper.

PIE Unit Cancellations: The New Zealand Form 8621 Trap Many Preparers Miss

PIE funds and KiwiSaver providers may cancel units to pay PIR tax, fees, or fund-level charges. A New Zealand statement may show this as an internal adjustment rather than a cash sale. For Form 8621, the U.S. workpaper may still need to analyze the unit cancellation as a disposal, redemption, or basis-adjustment event, with units, NZD proceeds, basis, gain or loss, and NZD-to-USD translation reviewed at lot level.

U.S.–New Zealand Tax Treaty, KiwiSaver, PIE Status and PFIC Classification

Under Article 1(3), the U.S.–New Zealand treaty preserves the U.S. right to tax its citizens under domestic law (the Savings Clause). The treaty does not automatically turn KiwiSaver or PIE funds into U.S.-qualified retirement assets, and it does not switch off IRC §1297 or Form 8621 when PFIC triggers exist.

New Zealand PIR tax paid, PIE tax-deferred status, and retirement labels do not override U.S. tax classification. Form 8621 may be required when a filing trigger exists.

Form 8621 Filing Triggers for KiwiSaver, PIE Funds, Fund Switches and Withdrawals

| NZ action | PFIC trigger | NZ-specific example |

|---|---|---|

| KiwiSaver fund switch | possible PFIC disposition | Growth → Balanced / provider transfer |

| KiwiSaver provider transfer | fund redemption and purchase review | ANZ → Simplicity / Milford → Kernel |

| Employer contribution | new PFIC acquisition lot / income review | employer contribution buys fund units |

| Government contribution | income and basis review | annual government contribution buys units |

| PIE unit cancellation | possible disposal, redemption, or basis event | units cancelled for PIR tax or fees |

| PIE distribution / reinvestment | distribution plus new acquisition | reinvested fund income / DRP lots |

| First-home withdrawal | redemption, distribution, or disposition review | KiwiSaver first-home withdrawal |

| Retirement withdrawal | §1291 / MTM disposition review | withdrawal after long holding period |

| NZX ETF sale | PFIC disposition | sell USF, FNZ, TWF, NZG |

| Long-term hold with no sale | annual reporting review | year-end PFIC value / elections |

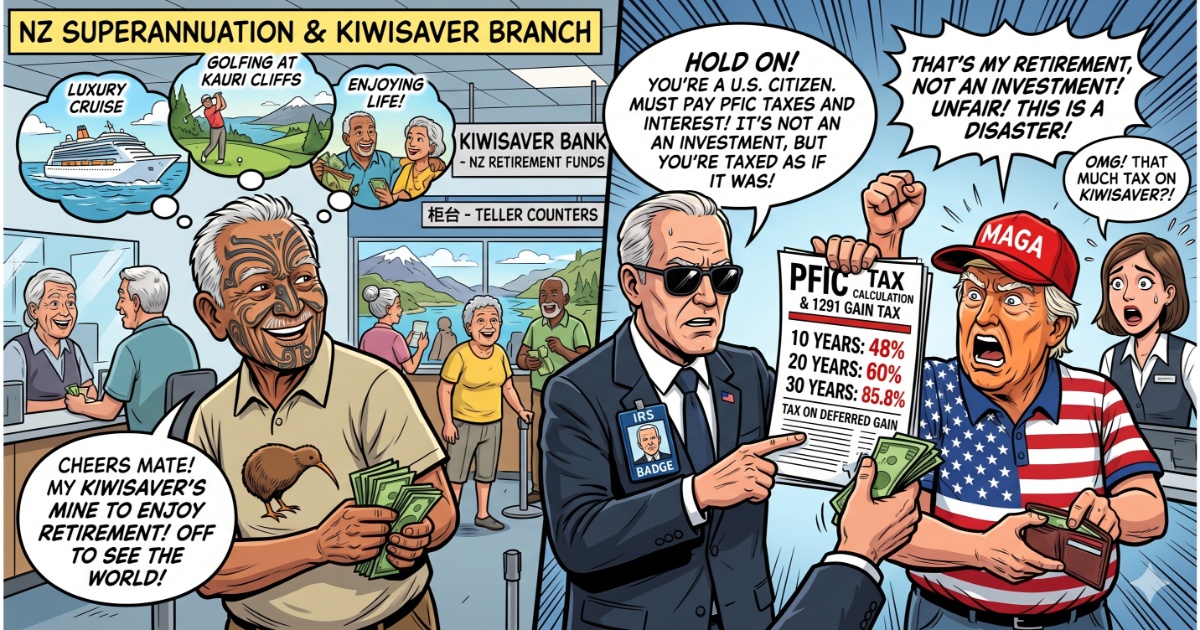

Risk Scenario: PFIC §1291 Tax and Interest Cost Over Time

Table A models a $10,000 PFIC gain under §1291 using actual historical U.S. tax rates and IRS quarterly underpayment interest rates. The punitive interest can accumulate over time, often exceeding the underlying tax liability on the gain.

Waiting until sale or IRS contact can make the PFIC calculation harder because §1291 interest increases with time. PFIC tax is punitive by design, aimed at neutralizing the benefit of offshore tax deferral. For years of unreported KiwiSaver, Streamlined Procedures may be the only realistic way back into compliance.

Table A: PFIC §1291 Interest Calculation Over Time

(Single purchase on yyyy-01-01 → sale on 2025-12-31)

| Period | Tax | Interest | % Consumed |

|---|---|---|---|

| 5 years | $3,440 | $590 | 40.3% |

| 10 years | $3,622 | $1,227 | 48.5% |

| 20 years | $3,630 | $2,396 | 60.3% |

| 30 years | $3,689 | $4,891 | 85.8% |

| 33 years | $3,714 | $6,200 | 99.1% |

| 35 years | $3,679 | $6,930 | 106.1% |

New Zealand PFIC Case Studies: KiwiSaver, PIE Funds and Form 8621

Case 1 — KiwiSaver Growth-to-Balanced Switch Triggers Multiple Form 8621 Filings

Profile: U.S. citizen in New Zealand with KiwiSaver since 2016.

Local asset: KiwiSaver Growth Fund switched into a Balanced Fund.

Wrong assumption: “I did not withdraw cash. I only changed the fund option inside KiwiSaver.”

Trigger event: Growth Fund units are redeemed; Balanced Fund units are purchased.

U.S. tax issue: The redeemed Growth Fund creates a PFIC disposition. If gain exists and no QEF or MTM election was in place, §1291 applies to the disposed fund. The new Balanced Fund starts a separate PFIC holding period. One KiwiSaver account therefore triggers more than one Form 8621 when multiple fund options or layered underlying funds are involved. See Fund-of-Funds PFIC Risk.

Case 2 — PIE Unit Cancellations Break the “No Filing” Assumption

Profile: U.S. citizen holding PIE funds through InvestNow, Sharesies, Kernel, or a KiwiSaver provider.

Local asset: NZ-domiciled PIE managed fund or PIE ETF.

Wrong assumption: “My balance is under $25,000, so Form 8621 does not matter.”

Trigger event: The PIE fund cancels units to collect management fees, tax, or fund-level charges.

U.S. tax issue: A unit cancellation looks like a fee on the New Zealand statement. For Form 8621, the unit cancellation may need to be reviewed as a disposal, redemption, or basis-adjustment event. If the cancelled units produce gain or another Form 8621 trigger applies, the small-value reporting exception may not protect the position. The file then needs fund-by-fund Form 8621 review. See Form 8621 Filing Requirements.

Related PFIC Technical Guides

PFIC Classification and Filing Basics

- 🔗 What Is a PFIC under IRC §1297?

- 🔗 Form 8621 Filing Exemption Rules for PFIC Stock

- 🔗 What to Do After Discovering a PFIC

- 🔗 Never Filed Form 8621 for a PFIC?

PFIC Tax Calculations and New Zealand KiwiSaver Data

- 🔗 §1291 Excess Distribution and Interest Calculation

- 🔗 §1291 vs MTM 10-Year PFIC Tax Comparison

- 🔗 PFIC Foreign Exchange Translation Rules for NZD and USD

- 🔗 PFIC Fund Switch and §1291 Disposition Trap

- 🔗 Standardized Form 8621 Line 16a Statement

PFIC Election Strategy: §1291, MTM, and QEF

Choosing Professional Help for KiwiSaver PFIC Cleanup

FAQ: KiwiSaver, PIE Funds, Smartshares USF and Form 8621

Is KiwiSaver a PFIC for U.S. taxpayers?

Are PIE funds PFICs for U.S. citizens in New Zealand?

Are Smartshares USF, FNZ, TWF, or NZG PFICs?

Is Smartshares USF the same as VOO for PFIC purposes?

Does a KiwiSaver fund switch trigger Form 8621?

Can PIE unit cancellations for PIR tax or fees create Form 8621 reporting?

Can a KiwiSaver first-home withdrawal trigger PFIC tax?

Are KiwiSaver employer and government contributions taxable in the U.S.?

Is a PIE term deposit a PFIC trap?

Can I use Hatch, Sharesies, or Stake to buy VOO or VTI and avoid PFIC?

Does my child’s KiwiSaver need Form 8621?

Can TurboTax calculate §1291 tax for KiwiSaver or PIE funds?

Sources and References

- 🔗 IRS Form 8621 and Instructions: Official IRS guidance for PFIC reporting obligations.

- 🔗 IRC §§1291–1298: Statutory framework governing PFIC taxation.

- 🔗 Treas. Reg. §§1.1296-1 and 1.1296-2: Mark-to-Market election and marketable stock rules.

- 🔗 U.S.–New Zealand Tax Treaty: Official treaty documents and technical explanation.

- 🔗 IRD New Zealand (KiwiSaver): Government guidance for retirement savings and PFIC review.

- 🔗 IRD New Zealand (PIE): Official Portfolio Investment Entity tax regime details.

- 🔗 Financial Markets Authority (FMA): NZ government agency regulating financial providers, KiwiSaver schemes, and investment markets.

Current as of May 2026 · Based on Form 8621 (Rev. 12/2025)