Model Assumptions: Foreign S&P 500 ETF

- Holding Period: $100,000 purchase at the beginning of 2016, with a full sale at the end of 2025.

- Taxpayer Rate: Constant 24% U.S. federal ordinary income tax rate.

- Exclusions: Calculations exclude Net Investment Income Tax (NIIT), state taxes, foreign withholding taxes, and transaction costs.

For U.S. taxpayers dealing with their first year of tax residency, understanding these elections is crucial to avoid legacy PFIC traps. For a detailed roadmap on managing these assets during your transition year, refer to the first-year U.S. resident PFIC calculation comparison.

| Country / Market | S&P 500 ETF codes |

|---|---|

| Canada | VFV.TO, ZSP.TO, XSP.TO |

| Ireland / London | CSPX.L, VUAG.L, VUSA.L |

| Australia | IVV.AX |

| Japan | 1655.T, 2558.T, 2633.T |

| Taiwan | 00646.TW |

| South Korea | 360200.KS, 360750.KS, 379800.KS |

| New Zealand | USF.NZ |

| Hong Kong | 3195.HK, 9195.HK |

S&P 500 trackers broadly converge over a 10-year window. The wrapper changes the tax engine, not the index exposure. To show the same PFIC tax split across different foreign S&P 500 wrappers, this article uses two visuals: a static chart for USF.NZ and an interactive chart for VFV.TO.

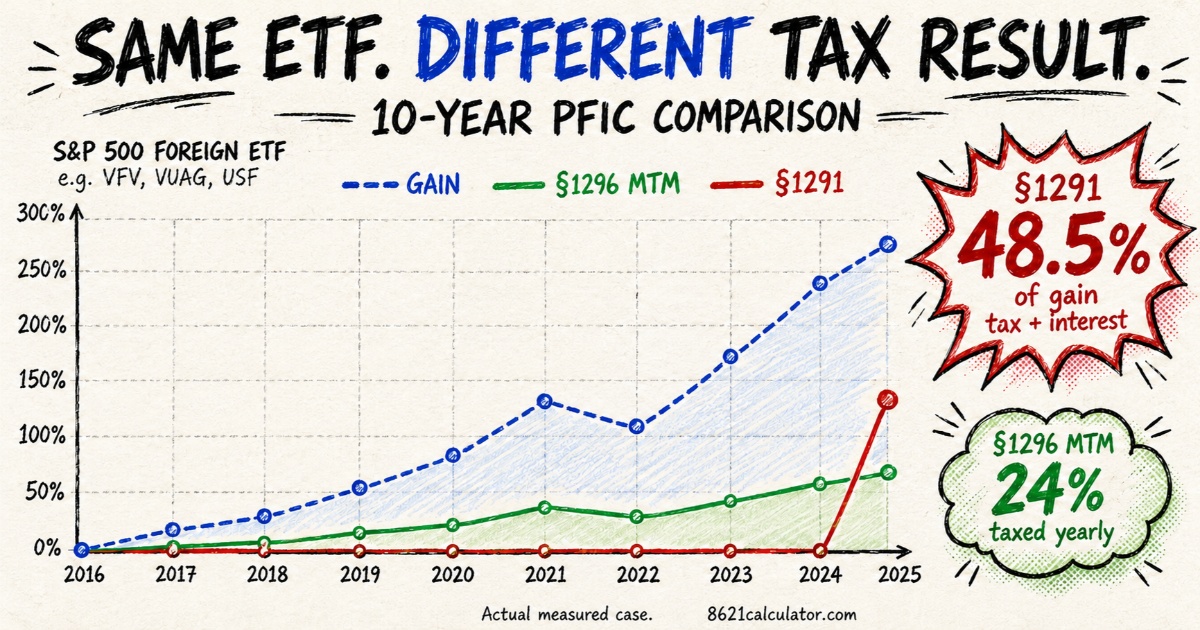

USF.NZ: 10-Year PFIC Tax Pattern Illustration

VFV.TO: 10-Year Interactive PFIC Case Study

VFV.TO actual price movement from early 2016 through year-end 2025 shows roughly 247.8% appreciation. A $100,000 purchase grows to approximately $347,800 before excluded items.

| Event | Date | Price | Units | Total Value |

|---|---|---|---|---|

| Buy | 2016-01-04 | $48.21 | 2074.26 | $100,000 |

| Sell | 2025-12-31 | $167.64 | 2074.26 | $347,729 |

Total Gross Gain: $247,729

Side-by-Side Tax Result: §1291 vs MTM

§1291 Tax Consequences: Excess Distribution and Interest Charge

While §1291 defers taxes during the holding period, it imposes a punitive IRS tax bill at sale, taking nearly 48.5% after 10 years.

Under the §1296 MTM election, you are taxed annually on unrealized gains at your ordinary income rate. However, upon final sale, your total cumulative tax paid exactly equals your total gain multiplied by that flat rate (e.g., 24%).

| Item | §1296 MTM | §1291 Default |

|---|---|---|

| Gross gain | $247,729 | $247,729 |

| Total tax drag | 24% | 48.5% |

| Tax + interest | $59,455 | $120,148 |

| Net profit retained | 76% | 51.5% |

| Net profit | $188,274 | $127,581 |

§1291 is the punishment engine.

2025-end test: at 33 years, §1291 tax plus interest exceeds 99% of the gain. Hold longer, and it starts eating principal.

The IRS should send thank-you letters to PFIC holders past year 30.

PFIC FAQ: §1291 vs §1296 MTM

Common technical questions regarding the long-term impact of IRC §1291 vs. §1296 MTM election.

Is MTM election better than §1291 for a PFIC?

What is the main difference between §1291 and §1296 MTM?

Why does §1291 become worse the longer I hold?

What is the downside of the PFIC MTM election?

Can I switch from §1291 to MTM later?

Internal Resources

- 🔗 PFIC 101: Understanding §1297

- 🔗 Comparing §1291, MTM, and QEF Elections

- 🔗 QEF Calculation Technical Guide

- 🔗 Form 8621 Filing Exemption Rules

- 🔗 FX Translation Rules for PFIC Reporting

- 🔗 Streamlined Filing: What If You Never Filed?

Current as of May 2026 · Based on Form 8621 (Rev. 12/2025)