Quick Answers: PFIC Streamlined Filing and Late Form 8621

Can I include late Form 8621 in Streamlined Filing?

Does Streamlined Filing reset PFIC §1291 history?

Can I make a retroactive MTM or QEF election in Streamlined Filing?

What is the biggest PFIC risk in Streamlined Filing?

Can Streamlined Filing Fix Late Form 8621? SFOP vs SDOP

| Compliance Feature | SFOP (Foreign Offshore) | SDOP (Domestic Offshore) |

|---|---|---|

| Taxpayer Status | Non-resident taxpayers | U.S. resident taxpayers |

| Returns Required | 3 years original or amended 1040s + 6 years FBARs | 3 years amended 1040s only + 6 years FBARs |

| Offshore Penalty | Zero (0%) | 5% of highest aggregate foreign asset value |

| Form 8621 Rule | Full §1291 history from acquisition date required | Full §1291 history from acquisition date required |

Both procedures require a Form 14653 or 14654 — a signed certification under penalties of perjury that your failure was non-willful (due to negligence, inadvertence, or mistake).

Streamlined is the IRS's one-time penalty-relief path for non-willful offshore noncompliance. Form 8621 is the math test. A complete §1291 calculation, backed by a clean Line 16a statement, shows good-faith correction. Bad PFIC math can waste the only clean filing opportunity you get.

Do not force fake retroactive QEF or MTM elections. If prior PFIC years fall under §1291, calculate §1291: excess distributions, gain allocation, FX, basis, and §6621 interest.

Late PFIC election positions should be supported by the applicable legal authority and the taxpayer's facts.

Streamlined protects the non-willful correction path. It does not protect election manipulation.

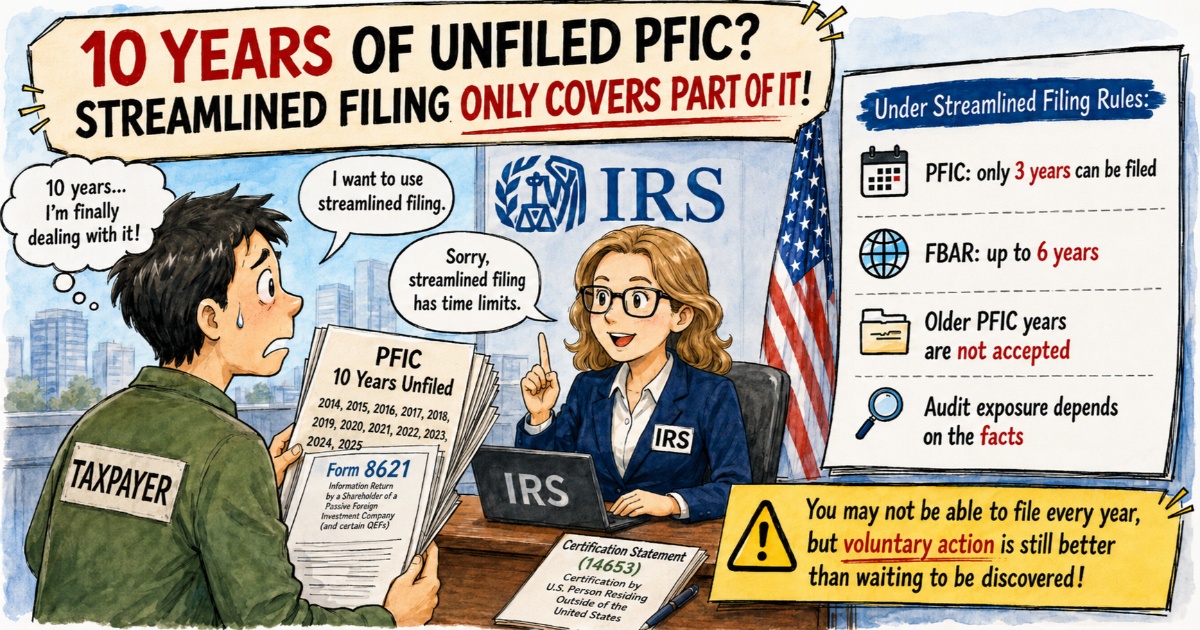

The §1291 Full-History Requirement: Why 3 Years Is Not Enough

The Streamlined window covers 3 tax years. The §1291 throwback calculation covers the entire holding period from acquisition. These are two different clocks.

Why truncation fails:

§1291(b)(2)(A) allocates the excess distribution ratably across every day held. If you truncate a 15-year

holding period to fit the 3-year Streamlined window, the denominator is wrong. Consequently, the allocation,

the deferred tax, and the §6621 interest chain are all mathematically invalid. [See: Full §1291 Methodology]

A correct Streamlined submission requires:

- 3 Form 1040s (the Streamlined window).

- Form 8621 for each PFIC in those 3 years.

- Full history: If acquired in 2008 and reported in 2026, the §1291 computation must cover 2008–2026.

Can You Make a Retroactive QEF or MTM Election in Streamlined Filing?

No. Filing late Forms 8621 in a Streamlined submission does not grant you the right to make retroactive QEF or Mark-to-Market (MTM) elections.

- QEF: Requires explicit IRS consent or a previously filed protective statement.

- MTM: Requires formal §301.9100 relief.

You cannot simply check the election box on an amended return to bypass the §1291 interest charge. Prior years generally remain trapped in the default §1291 regime.

👉 Late QEF and MTM Elections in Streamlined Filing: when and how a late election may be available.

Why Prior PFIC Years May Remain Open Under §6501(c)(8)

Streamlined generally covers 3 tax years. Under §6501(c)(8), a missing Form 8621 can keep the relevant assessment period open until the required information is properly furnished, subject to the statute's reasonable-cause limitations.

| Year Bucket | Streamlined Action | §6501(c)(8) Status |

|---|---|---|

| Years 1–3 | File 1040/1040X + Form 8621 | Covered |

| Years 4–10+ | Not covered | May remain open |

The Reality: No Fix for Older Years

There is no official IRS procedure to close the statute of limitations for PFIC years prior to the 3-year

Streamlined window. You cannot simultaneously submit older forms under Delinquent Filing (DIIRSP) to bypass

this.

The practical result: Streamlined cleans the filing window, not the entire PFIC past. The §1291 math must still start from acquisition, and older missing Form 8621 years may remain open under §6501(c)(8).

Why §1291 Accuracy Matters for Streamlined Non-Willful Certification

In a Streamlined submission, the non-willful certification relies on a good-faith effort to correctly report historical tax obligations. Systematically incorrect §1291 calculations—especially those that consistently understate the tax liability—can undermine the credibility of the submission.

Common PFIC Streamlined Calculation Errors

To ensure compliance, practitioners should avoid these common PFIC calculation errors:

| §1291 Calculation Error | Impact on Liability | Compliance Issue |

|---|---|---|

| Oct 15 Start (vs. April 15) | Understates interest. | Yes — favors taxpayer. |

| Annual Compounding (vs. Daily) | Understates interest. | Yes — violates §6621. |

| Truncating History to 3 Years | Understates tax. | Yes — violates §1291(b). |

| Annual Average FX Rate | Distorts gain/loss. | Low competence signal. |

| Missing Line 16a Statement | Unverifiable math. | Incomplete — audit risk. |

PFIC Streamlined Filing Step-by-Step Workflow

Step 1: Identify all PFIC assets

Review all your non-U.S. financial accounts to identify foreign mutual funds, ETFs, unit trusts, or managed portfolios that trigger PFIC classification. Treat every fund separately; a single brokerage account can require dozens of individual Form 8621s.

Step 2: Perform back-year PFIC calculations

Reconstruct transactions, distributions, and sales in USD and CAD/local currency. Compute the full §1291 history from the exact acquisition date. Apply §6621 daily compounding interest and prepare supporting Line 16a statements where required.

Step 3: Prepare back-year tax returns and Form 8621

Complete Form 8621 for each PFIC for the required streamlined filing years (typically 3 back tax years) and attach them to amended Form 1040X tax returns. Integrate the §1291 deferred tax and interest into the returns.

Step 4: Draft and submit the Streamlined certification

Complete and sign the non-willful certification statement (Form 14653 for SFOP or Form 14654 for SDOP). Apply the required red-ink Streamlined heading at the top of each return and mail the package to the IRS.

- 🔗 IRS — SFOP (Streamlined Foreign): irs.gov — SFOP

- 🔗 IRS — SDOP (Streamlined Domestic): irs.gov — SDOP

- 🔗 IRS — Delinquent International Information Return Procedures: irs.gov — DIIRP

- ⚖️ IRC §1291 — §1291(d)(1) coordination rule: law.cornell.edu §1291

- ⚖️ IRC §1295 — QEF election: law.cornell.edu §1295

- ⚖️ IRC §6501(c)(8) — Indefinite SOL: law.cornell.edu §6501

FAQ: PFIC Streamlined Filing, Late Form 8621, SFOP and SDOP

How many years of Form 8621 must be filed under the Streamlined Procedures? Is 3 years always enough?

Can I use SFOP or SDOP if I missed Form 8621 but filed FBARs?

Do I need one Form 8621 for each PFIC in Streamlined Filing?

What happens to PFIC years before the 3-year Streamlined window?

Does Streamlined Filing remove PFIC §1291 interest?

Does missing Form 8621 affect the IRS statute of limitations?

What PFIC records are needed for a Streamlined submission?

What if my broker no longer provides old PFIC transaction history?

Can I use average exchange rates for PFIC Streamlined calculations?

When should a tax attorney review a Streamlined PFIC case?

What is the biggest Form 8621 calculation mistake in Streamlined Filing?

Current as of May 2026 · Based on Form 8621 (Rev. 12/2025)