Technical Reference

📅 May 10, 2026

⏱️ 9 min read

📂 Form 8621 Guide

By Hans

PFIC Calculation Specialist · Creator of 8621calculator.com

If no valid QEF or MTM election was made on time, the cleanup years generally remain under the default

§1291 regime.

The Common Mistake

Filing Form 8621 late does not, by itself, validate a back-year QEF or MTM election. While Streamlined

Filing may fix late reporting requirements, it does not bypass the strict statutory deadlines for making

a valid election.

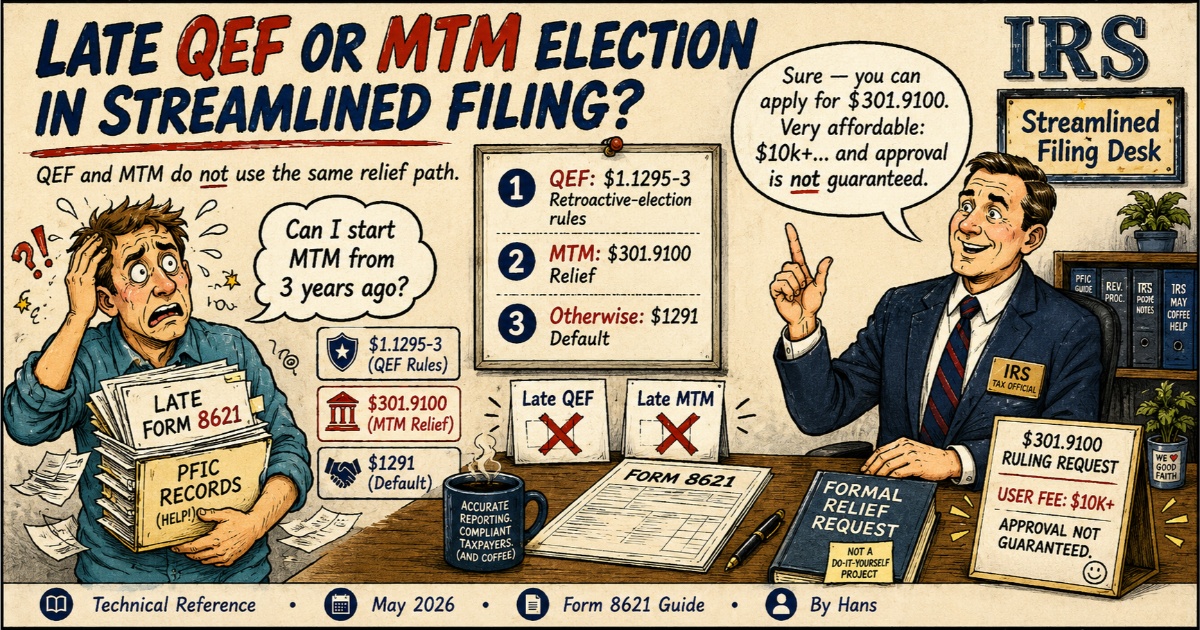

QEF: Retroactive Relief Is Narrow

A retroactive QEF election is possible only under the special rules of Treas. Reg.

§1.1295-3.

The IRS Form 8621 instructions explain two routes:

| Route |

Meaning |

| Protective statement |

The taxpayer previously preserved the

right

to make a retroactive QEF election. |

| IRS consent |

The taxpayer asks the IRS for permission,

usually based on strict reasonable-reliance facts. |

For most Streamlined filers, the protective statement route is unavailable because nothing

was filed earlier. The consent route is also narrow. “I did not know about PFIC” is usually

not enough. Relief generally requires showing reasonable reliance on a qualified tax professional who failed

to identify the issue. Ordinary §301.9100 relief is not available for late QEF elections.

MTM: Late Election Requires §301.9100 Relief

A retroactive MTM election is not automatic either. Treas. Reg. §1.1296-1(h)(1)(iii)

states

that a late §1296 election may be permitted only under §301.9100 relief. You cannot simply

check the MTM box on an old Form 8621 and assume the election works.

The practical barrier is hindsight. By the time a taxpayer files Streamlined returns, the

fund’s later performance is already known. The IRS is wary of allowing late MTM relief because the election

could be used selectively after seeing gains or losses. Relief requires showing reasonable good faith and

that granting it will not prejudice the government’s interests.

Hans

Late Election Costs: The §301.9100 Barrier

§301.9100 relief is IRS permission for a late tax election. For PFIC, it allows a retroactive MTM election. In 2025, the standard fee is $14,500. Reduced fees apply for lower incomes: $3,450 (under $400k) or $9,775 (under $1M). Approval is rare if the IRS suspects "hindsight" to avoid tax.

Practical Result in Streamlined

Unless formal relief is obtained, the Streamlined cleanup usually proceeds under §1291

for prior PFIC years. This means sales, redemptions, fund switches, or withdrawals may require:

- Allocation across the holding period.

- Tax at prior-year highest ordinary income rates.

- Interest using the IRS underpayment rates under §6621.

- Daily compounding under §6622.

Hans

Conclusion & Next Steps

Section 1291 excess distribution calculations are not spreadsheet math. They require full holding-period

reconstruction, prior-year allocation, historical tax-rate mapping, §6621 interest, and daily

compounding

under §6622. For serious PFIC compliance, manual spreadsheet shortcuts are not realistic.

Related Questions on PFIC Election Relief

Can I make a current-year MTM election even if prior years stay under §1291?

Yes, potentially. A taxpayer may be able to make a valid MTM election for the current year if the PFIC

stock qualifies as marketable stock, even if prior years remain under §1291. The transition year still

requires careful coordination.

What if the PFIC is not marketable stock?

If the fund is not marketable stock under the section 1296 rules, an MTM election is not available. In

that case, the taxpayer generally must evaluate §1291 or, if eligible and supported by proper

information, a QEF approach.

Do I need a separate relief request for each PFIC?

Usually yes. PFIC elections are made separately for each PFIC. If late-election relief is sought, the

analysis must be done fund by fund rather than at the account level.

Is “I did not know about PFIC” enough for late-election relief?

Usually no. For retroactive QEF relief or late MTM relief, the IRS generally expects more than simple

ignorance. Relief often depends on structured facts, such as reasonable reliance on a qualified tax

professional and satisfaction of the applicable procedural requirements.

Internal Resources

Disclaimer: This site provides global PFIC compliance guides, cross-border risk analysis, and

the algorithmic architecture powering our calculation engines. We engineer tax compliance technology; we do

not

prepare tax returns. All content is strictly for technical reference and does not constitute official tax

advice. Verify all tax positions independently.

Current as of May 2026 · Based on Form 8621 (Rev. 12/2025)