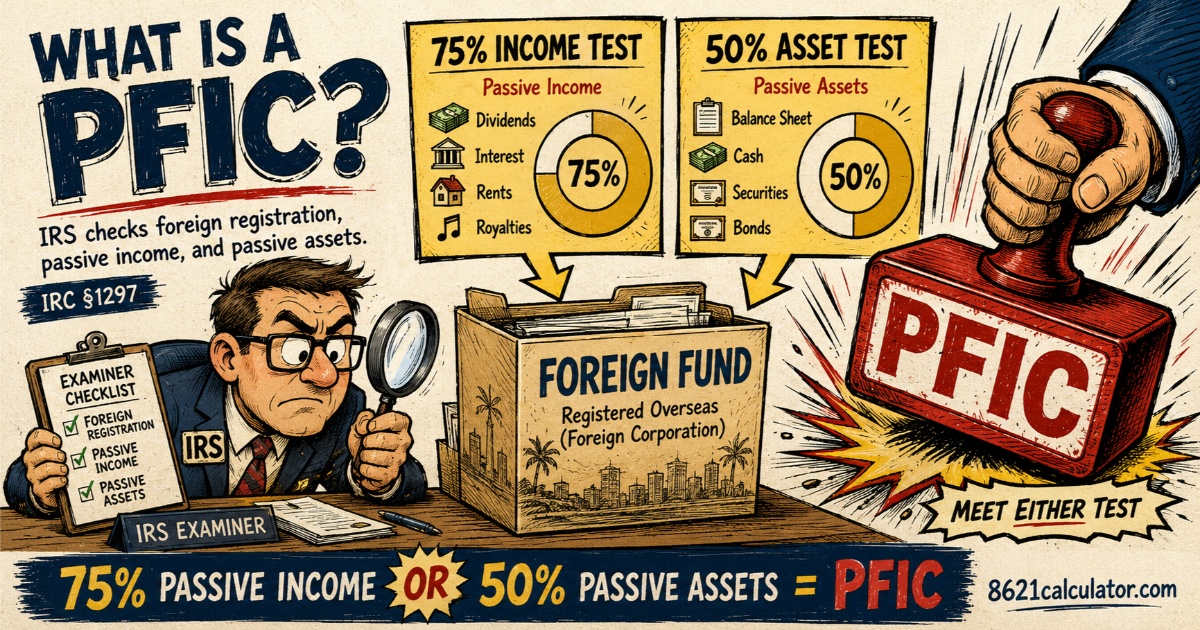

The Income Test

75% or more of its gross income for the taxable year is passive income.

The Asset Test

50% or more of its average assets during the taxable year produce passive income, or

are held for the production of passive income.

Only one test is required. Meeting either test is enough to classify a foreign

corporation as a PFIC.

Passive income is defined under IRC §1297(b), generally by reference to foreign personal holding company income under IRC §954(c), including dividends, interest, rents, royalties, annuities, and certain gains.

Practical Takeaway

Most PFIC problems for U.S. persons abroad come from ordinary foreign funds, not exotic offshore schemes. Foreign mutual funds, ETFs, managed funds, and pooled investment products commonly hold passive assets and earn passive income, so they often fall within the PFIC definition.

Common examples include Irish-domiciled UCITS ETFs (e.g., VWRA, IWDA), holdings within Japan NISA and iDeCo accounts, and local Indian mutual funds and ELSS schemes.