Quick Answer: How Is PFIC Tax Calculated?

PFIC tax is calculated by identifying the PFIC regime, measuring the gain or annual inclusion, and reporting the result on Form 8621. PFIC calculation is widely considered one of the most difficult areas of individual international tax reporting because it can require holding-period allocation, IRS interest, FX conversion, basis tracking, and Line 16a workpapers. This is why complex cases often require a dedicated PFIC tax calculator or detailed Form 8621 workpapers.

§1291 usually requires prior-year allocation and interest. QEF and MTM usually require annual PFIC data, year-end fair market value, basis tracking, and election history.

VFV PFIC Tax Example: Same S&P 500 Exposure, Different U.S. Tax Result

A Canadian-domiciled ETF such as VFV can track the same S&P 500 exposure as a U.S.-domiciled ETF such as VOO, but the U.S. tax result may be very different if VFV is treated as a PFIC.

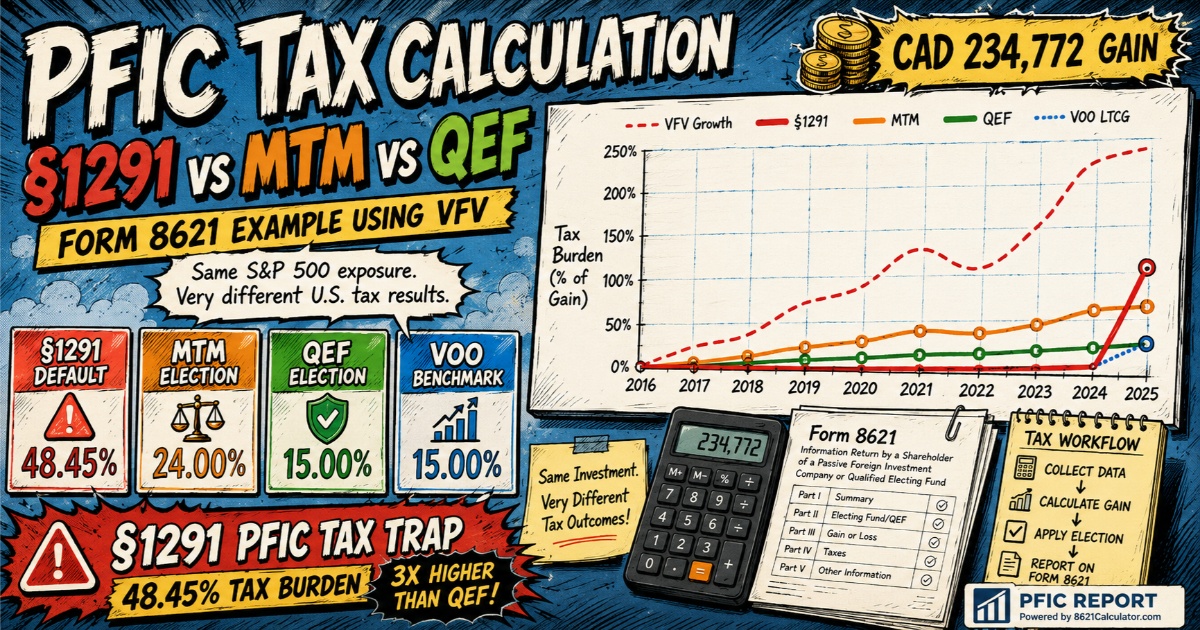

In this simplified example, the taxpayer invests about CAD 100,000 in VFV on January 4, 2016, and sells the full position on December 31, 2025 for CAD 334,740, producing an approximate CAD 234,772 gain.

The table below compares that same gain under default §1291, §1296 MTM, QEF, and a non-PFIC VOO benchmark.

| Date | Detail | Price (CAD) | Units | Value (CAD) |

|---|---|---|---|---|

| 2016-01-04 | Buy | 49.76 | 2,009 | 99,968 |

| 2025-12-31 | Sale | 166.62 | −2,009 | 334,740 |

By contrast, the QEF result is closest to the long-term capital gain benchmark, assuming the required PFIC Annual Information Statement data exists and the election was timely made. MTM avoids the worst §1291 deferral results, but it creates annual ordinary-income inclusion and cash-flow pressure.

For the broader Canadian ETF context, including VFV, XEQT, Canadian PFIC Annual Information Statements, TFSA, RRSP, and Canadian brokerage issues, see the Canada PFIC guide.

PFIC Tax Calculation Comparison: §1291 vs MTM vs QEF

The table below compares the modeled U.S. tax burden on a CAD 234,772 gain under each regime. This comparison assumes a 24% ordinary income rate and a 15% long-term capital gains benchmark, ignoring FX, state taxes, and annual distributions to isolate the impact of the PFIC regime.

| Calculation Method | Effective Tax Burden | Tax on Gain (CAD) | Calculation Impact |

|---|---|---|---|

| §1291 Default Regime | 48.45% | 113,746.91 | Gain allocated across the holding period, plus deferred tax and §6621 interest. |

| §1296 MTM Election | 24.00% | 56,345.22 | Annual mark-to-market inclusion as ordinary income; no default §1291 interest charge for elected years. |

| QEF Election | 15.00% | 35,215.76 | AIS-based annual inclusion; net capital gain character may be preserved when requirements are met. |

| VOO Benchmark | 15.00% | 35,215.76 | Non-PFIC U.S.-domiciled ETF benchmark using simplified long-term capital gain treatment. |

Why §1291 Creates the Highest PFIC Tax Burden

The default §1291 regime is the punitive fallback method when no valid QEF or MTM election applies. When a taxpayer sells a PFIC or receives an excess distribution, the gain is not treated like ordinary long-term capital gain. Instead, the calculation allocates the excess amount across the PFIC holding period.

The amounts allocated to prior years are taxed at the highest individual ordinary income tax rate applicable for those years (e.g., 37% or 39.6% depending on the tax year), regardless of your actual tax bracket. On top of that, the IRS adds an interest charge under Section 6621 mechanics, which is compounded daily from the due date of the return for each prior tax year. Over a long holding period, the interest charge can materially increase the effective PFIC tax burden, especially when the gain is back-loaded into a sale year after many years of ownership.

The §1291 method requires precise holding-period calculations and daily interest rate tracking, necessitating detailed Form 8621 Line 16a supporting statements for the tax return. For a deeper breakdown of this mechanism, see the §1291 excess distribution calculation guide and the PFIC interest charge guide.

How MTM Changes the PFIC Tax Calculation

For marketable PFICs, a Section 1296 mark-to-market (MTM) election offers a way to move away from the §1291 deferral-and-interest regime. Under MTM, you treat the investment as if it were sold for its fair market value on the last business day of your tax year.

Any unrealized appreciation is included in your income and taxed as ordinary income in the current year. While MTM removes the IRS interest charge and prior-year allocations for elected years, it converts all gains into ordinary income, stripping away the benefit of lower long-term capital gains rates. Furthermore, you must pay tax on "paper" gains before actually realizing cash from a sale, creating annual cash-flow requirements.

For a technical overview of calculations and basis adjustments under this regime, see the §1296 mark-to-market guide.

How QEF Can Reduce PFIC Tax When AIS Data Exists

The Qualified Electing Fund (QEF) election is generally the cleanest path because it aligns closest to U.S. mutual fund taxation. A QEF election may preserve net capital gain character when valid PFIC Annual Information Statement data is available and the election is timely made.

This path can avoid the default §1291 interest-charge regime for properly elected QEF years. However, making a QEF election requires the fund manager to provide a PFIC Annual Information Statement (AIS) containing precise per-share, per-day income figures. While some Canadian fund managers publish these statements, many UCITS funds do not provide PFIC Annual Information Statements, which often makes QEF impractical.

A QEF election is cleanest when made in the first PFIC year. If made later, prior non-QEF years may still require §1291 reconstruction, a purging election, or late-election relief analysis. For more details, see the QEF election calculation guide.

Is There a Fixed PFIC Tax Rate?

There is no single fixed PFIC tax rate. The tax burden depends on the PFIC regime, election history, holding period, income character, and whether §1291 interest applies:

- §1291: Variable. Gains allocated to prior years are taxed at the highest statutory ordinary rate for those years, plus compounding interest under §6621.

- §1296 MTM: The taxpayer's marginal ordinary income tax rate (ranging up to 37% or 39.6% at the federal level), applied annually to unrealized gains.

- QEF: Pro-rata share of fund ordinary earnings (ordinary income rates) and net capital gains (long-term capital gains rates).

Excess Distribution Regime

Applies when no election is made. Gain allocated across holding period, taxed at prior-year rates, plus IRS interest charge. Most complex path.

Most PunitiveQualified Electing Fund

Annual inclusion of ordinary earnings and net capital gain based on PFIC Annual Information Statement data; may preserve net capital gain character when the required data and timely election are available.

Cleanest PathPFIC Tax Calculator and Form 8621 Workpapers

PFIC tax calculations are difficult to manage reliably in ordinary spreadsheets when the case involves multi-year §1291 allocations, daily interest, FX conversion, partial sales, multiple lots, or MTM basis tracking.

For CPAs, EAs, and advanced taxpayers, accurate lot-level calculation workpapers are required to verify the amounts reported on Form 8621 and to provide the mandatory supporting statements for Line 16a (for §1291 allocations) or Section 1296 schedules.

Common PFIC Tax Mistakes

- Treating foreign ETFs like U.S. ETFs: Many foreign ETFs and mutual funds are treated as PFICs because they are foreign corporations or foreign pooled vehicles that primarily hold passive assets or earn passive income.

- Assuming no sale means no Form 8621: Annual Form 8621 reporting may still apply under §1298(f), even without a sale or distribution, unless an exception applies.

- Assuming QEF without AIS data: A QEF election generally requires PFIC Annual Information Statement data from the fund. Ordinary fund fact sheets or annual reports usually do not provide enough information for QEF reporting.

- Ignoring prior non-QEF years: Making a QEF election in a later year does not clean up prior years. The fund remains subject to §1291 unless a purging election is executed.

- FX translation errors: PFIC calculations often require careful FX treatment for acquisition cost, sale proceeds, distributions, and Form 8621 reporting lines. Using a shortcut FX method can distort the result.

PFIC Tax FAQs

How is PFIC tax calculated?

Is there a fixed PFIC tax rate?

Why is §1291 PFIC tax so high?

Can QEF reduce PFIC tax?

Do I need a PFIC tax calculator?

IRS Sources & Official References

- 🔗 IRS Form 8621 PDF: Official IRS PDF form — Information Return by a Shareholder of a Passive Foreign Investment Company or Qualified Electing Fund.

- 🔗 IRS Form 8621 Instructions: Official IRS instructions covering §1291, §1296, QEF elections, and PFIC reporting requirements (Web and PDF formats).

Recommended Reading

- 🔗 Form 8621 Overview Guide — Reporting Requirements and Elections

- 🔗 §1291 Excess Distribution Calculation Guide

- 🔗 §1296 Mark-to-Market Election Guide

- 🔗 QEF Election Calculation Guide

- 🔗 PFIC §1291 Interest Charge Calculation

- 🔗 Canada PFIC Guide — VFV, XEQT, TFSA, RRSP, and Canadian ETFs

Current as of May 2026 · Based on Form 8621 (Rev. 12/2025)