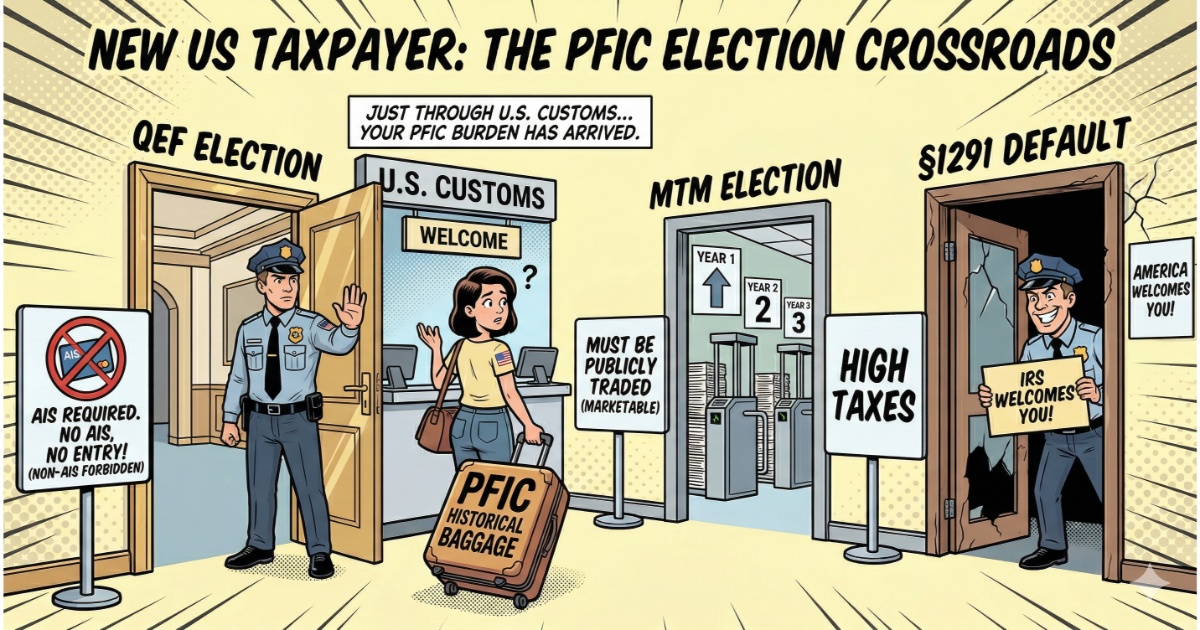

In practice, many CPAs follow a simple rule of thumb: QEF election first, Mark-to-Market (MTM) second, and §1291 only as a last resort. However, practitioners who regularly work with PFIC reporting know that the reality is often more complex. When foreign funds were acquired before becoming a U.S. taxpayer, the choice of first-year PFIC election can significantly affect how those gains are treated on Form 8621.

A poor election on Form 8621 may result in higher tax, taxation of gains earned before U.S. residency, or substantially higher tax when the investment is eventually sold — and in some situations, the often-criticized §1291 regime may actually produce the optimal outcome.

What Is the PFIC First-Year Election Problem for New U.S. Residents?

A PFIC is any foreign corporation where either (1) 75% or more of gross income is passive income (Income Test), or (2) 50% or more of assets produce passive income (Asset Test), as defined under IRC §1297. Foreign ETFs, mutual funds, and unit trusts are almost universally classified as PFICs under these tests.

The problem for new U.S. residents is timing and irreversibility: the moment an individual becomes a U.S. tax person — through the Substantial Presence Test (IRC §7701(b)) or upon receiving a green card — any foreign fund they already hold becomes subject to PFIC rules. The first-year election made on Form 8621 locks in how all future gains, distributions, and dispositions from that fund will be taxed for the entire U.S. holding period. A wrong choice — or no choice at all — is generally irrevocable and can be extremely costly.

Is There a PFIC “First-Year Exception” for New U.S. Residents?

There is no blanket “PFIC first-year exception” that makes foreign funds tax-free for a new U.S. tax resident. What does exist is a first-year election window: a timely QEF election under IRC §1295(b)(2) — made without a purging election in the first year — or a §1296 MTM election for marketable PFIC stock. If no valid election is made by the deadline, the §1291 default regime applies automatically. The real opportunity is making the right first-year election before the tax return due date.

First-Year PFIC Reporting Timeline

- Day 1 of U.S. Tax Residency — PFIC obligation begins (IRC §7701(b): Substantial Presence Test or green card issuance date)

- December 31 of the First Tax Year — MTM year-end mark-to-market calculation date; fund FMV snapshot required for §1296 reporting

- April 15 (Following Year) — Form 8621 due date; QEF and MTM elections must be made on this return

- October 15 (With Form 4868 Extension) — Extended election deadline; both QEF and MTM elections remain available with a valid extension

- After the Deadline — Rev. Proc. 2020-27 relief may apply for certain retroactive QEF elections; late-election remedies are limited and granted only at IRS discretion

Foreign Funds Held Before Becoming a U.S. Tax Resident

The first-year PFIC problem is most acute for taxpayers who accumulated foreign fund investments before immigrating. These funds may carry years of unrealized appreciation, no prior QEF history, and often no AIS. The first-year election must account for this pre-residency gain — how it is taxed depends entirely on which regime applies going forward.

This challenge is highly relevant for Indian nationals moving to the US with existing mutual fund portfolios, Chinese nationals with A-share or WMP holdings, UK residents relocating to the US with ISA or SIPP accounts, and Japanese nationals with NISA/iDeCo balances.

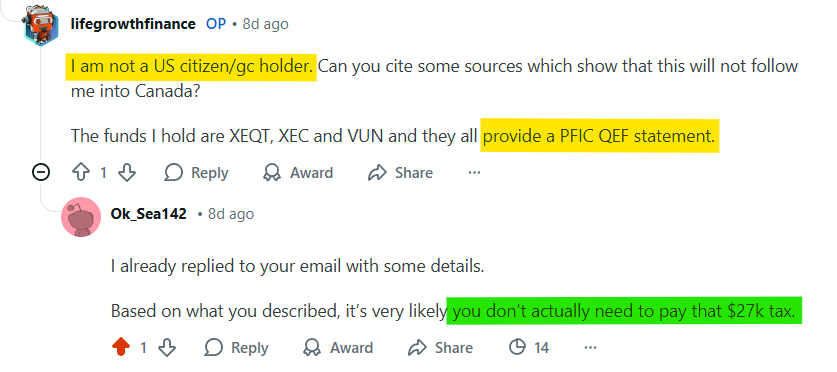

The single most important preliminary question is: Does your fund provide a PFIC Annual Information Statement (AIS)? This determines whether a QEF election is even available. For most foreign funds, the answer is no — which means the real first-year choice is MTM vs §1291.

| Foreign asset held before U.S. residency | Typical first-year PFIC issue | AIS available? | Country guide |

|---|---|---|---|

| Indian mutual funds / SIP / ELSS | §1291 or MTM; INR FX conversion; no AIS in most cases | ✗ Rarely | India PFIC Guide |

| Canadian ETFs (XEQT, VUN, VGRO) | AIS may exist for some ETFs; QEF/MTM/§1291 all require analysis | ✓ Some funds | Canada PFIC Guide |

| UK ISA / OEIC / UCITS funds | IRS does not recognize ISA tax exemption; MTM common election | ✗ Rarely | UK PFIC Guide |

| Irish-domiciled ETFs (VWRA, IWDA, CSPX, VUAA) | UCITS classified as PFIC; §1296 MTM most practical election | ✗ | Ireland ETF Guide |

| Taiwan ETFs (0050, 0056, 00878) | TWD FX conversion; dividend withholding; MTM vs §1291 analysis | ✗ | Taiwan PFIC Guide |

| Australian managed funds / ETFs | AMMA statements are not PFIC AIS; §1291 or MTM likely | ✗ | Australia PFIC Guide |

| Singapore CPF / unit trusts / SRS | Wrapper vs underlying fund; CPF exemption not recognized by IRS | ✗ Rarely | Singapore PFIC Guide |

Comparing First-Year PFIC Elections on Form 8621: QEF, §1296 MTM, and §1291

First-Year QEF Election: IRC §1295(b)(2) and the AIS Requirement

A common misconception among new U.S. taxpayers—and the core source of the $27,000 panic in our case analysis—is the belief that they must perform a "deemed sale" to activate a QEF election for previously held foreign funds.

In fact, under IRC §1295(b)(2), a QEF election applies only to the shareholder’s holding period during which the shareholder is a United States person. The Instructions for Form 8621 (Part II – Elections / QEF Election) further clarify that if a taxpayer makes a QEF election in the first year they are a U.S. shareholder of the PFIC, the PFIC will generally be treated as a QEF for the entire U.S. holding period. In this situation, no purging election is required.

First-Year §1296 MTM Election for New U.S. Tax Residents

For new U.S. residents whose foreign funds do not provide a PFIC AIS, the §1296 mark-to-market (MTM) election is typically the most practical first-year option — provided the PFIC stock is marketable.

MTM Eligibility: Marketable PFIC Stock

Under IRC §1296, the MTM election is available only for marketable PFIC stock — stock regularly traded on a qualified exchange or market, as defined in Treas. Reg. §1.1296-2. Most publicly listed foreign ETFs and mutual funds that trade on recognized exchanges (e.g., Toronto Stock Exchange, London Stock Exchange, Taiwan Stock Exchange) qualify. Non-traded funds, private vehicles, and insurance-linked products typically do not.

§1296(l) Starting Basis: The Basis Adjustment for New Residents

A first-year MTM election under §1296(l) is not a true cost basis reset. Under IRC §1296(l), when a taxpayer becomes a U.S. person and makes a timely MTM election, the basis for MTM purposes starts at the higher of historical cost or FMV on the residency start date. This allows the PFIC to enter the MTM regime without a purging election and without immediate recognition of pre-residency appreciation as ordinary MTM income.

While §1296(l) prevents pre-residency appreciation from being taxed as ordinary MTM income, pre-residency gains cannot be permanently eliminated. Upon disposition, pre-residency gain is recognized under general tax rules (IRC §1001) — typically as long-term capital gain at 20%.

MTM Annual Obligation, Ordinary Rate Treatment, and Irrevocability

Once a §1296 MTM election is made, it applies to every subsequent tax year in which you hold the PFIC stock as a U.S. person. Each year, you must include in income the excess of the fund’s year-end FMV over its adjusted basis — taxed at ordinary income rates, not capital gains rates. This is the core trade-off: MTM eliminates §1291 throwback complexity but converts annual appreciation into ordinary income. Per the IRS Form 8621 Instructions, the MTM election must be made by the due date of the return for the tax year in which the stock is first marked to market, including extensions. Once made, the election is generally irrevocable unless the PFIC ceases to be marketable or the IRS grants consent to revoke.

Default §1291 Regime: What Happens If No First-Year Election Is Made

If no valid election is made—or if the taxpayer fails to meet the specific requirements for QEF or MTM—the asset automatically falls into the Section 1291 default regime.

- Historical Basis Continuity: Your entire global holding period and original cost are used in future calculations.

- The Pre-Residency Taint: When you eventually receive a distribution or sell the asset, the gains are allocated across your entire holding period. While the portions attributed to your pre-U.S. residency years are taxed without the punitive interest charges, they are still fully taxable.

- Residency-Period Penalties: The portions attributed to your U.S. residency years are subject to the highest marginal tax rates plus daily compounded interest (the "throwback tax").

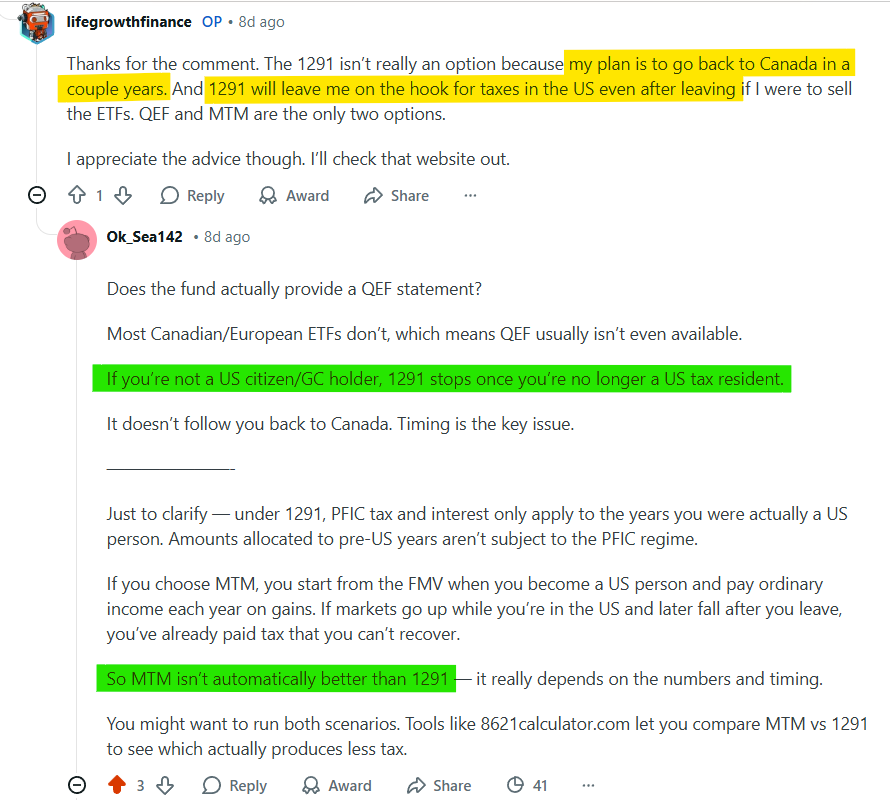

This technical burden is what fueled the "1291 Ghost" Method panic—the fear that PFIC liabilities would linger long after leaving the United States. In reality, this is a common misconception. Under IRC §1291(a) and Treas. Reg. §1.1291-1(b)(7), PFIC rules apply only during periods when a taxpayer is a United States person. Future disposals after you cease to be a U.S. resident do not trigger throwback taxes, meaning the "Ghost" cannot follow you abroad.

Form 8621 Decision Matrix for U.S. Residents: QEF vs. MTM vs. Section 1291

1. Conditions: High (AIS required)

2. Cost Basis: Original Cost. No step-up allowed; pre-arrival gains remain taxable.

3. Starting Status: Pedigreed. Avoids throwback tax if elected in Year 1.

4. Holding Period: Annual tax on fund earnings; remaining gain deferred.

5. Tax Rate: Low (20% LTCG rate for gains)

6. Sale: Capital gain on appreciation over basis.

7. Ending Status (Temp. Residents): Cut off at departure date; prorated QEF income reported.

8. Complexity: Minimal. Direct data entry from PFIC annual information statement.

1. Conditions: Medium (Marketable)

2. Cost Basis: Adjusted (MTM). FMV starting point for MTM inclusions; historical gain remains taxable.

3. Starting Status: Clean Entry. Avoids throwback tax if elected in Year 1.

4. Holding Period: Annual tax on mark-to-market gains at ordinary rates.

5. Tax Rate: Medium (Ordinary rates)

6. Sale: MTM gains (Ordinary) vs. Pre-residency (Capital Gains).

7. Ending Status (Temp. Residents): Cut off at departure date; final MTM gain reported.

8. Complexity: Very High. Lot tracking, basis maintenance, and "Unreversed Inclusion" (UI) monitoring.

1. Conditions: None (Universal)

2. Cost Basis: Original Cost. No step-up allowed; pre-arrival gains remain taxable.

3. Starting Status: Tainted. Throwback exposure across holding period.

4. Holding Period: No annual tax; gain accumulates under §1291.

5. Tax Rate: High (Max rate + interest)

6. Sale: Gain allocated pro-rata; U.S. years taxed with interest.

7. Ending Status (Temp. Residents): Cut off at departure date; no sale, usually no tax.

8. Complexity: Extreme. Full holding-period reconstruction and throwback interest calculations.

The “Ending Status” logic above applies exclusively to Temporary U.S. Residents who lose U.S. tax residency upon departure — specifically individuals on H-1B, H-1B1, L-1, L-2, O-1, TN (NAFTA/CUSMA), E-3 visas, and others who qualify as U.S. tax residents solely through the Substantial Presence Test (IRC §7701(b)) and who do not meet the test in the year after departure.

For U.S. Citizens and Green Card (LPR) Holders, simply leaving the country does not terminate your status as a “United States Person.” You remain subject to worldwide taxation and PFIC reporting regardless of your physical location. Green card holders must formally abandon their status (Form I-407 or a court order) to cease being U.S. persons. EB-5 investor visa holders who have received a green card face the same permanent obligation.

Note on F-1 OPT-to-H-1B converters: An F-1 student is generally an “exempt individual” not subject to the Substantial Presence Test. PFIC obligations typically begin only upon H-1B activation and the first year the Substantial Presence Test is met — not during F-1 status itself.

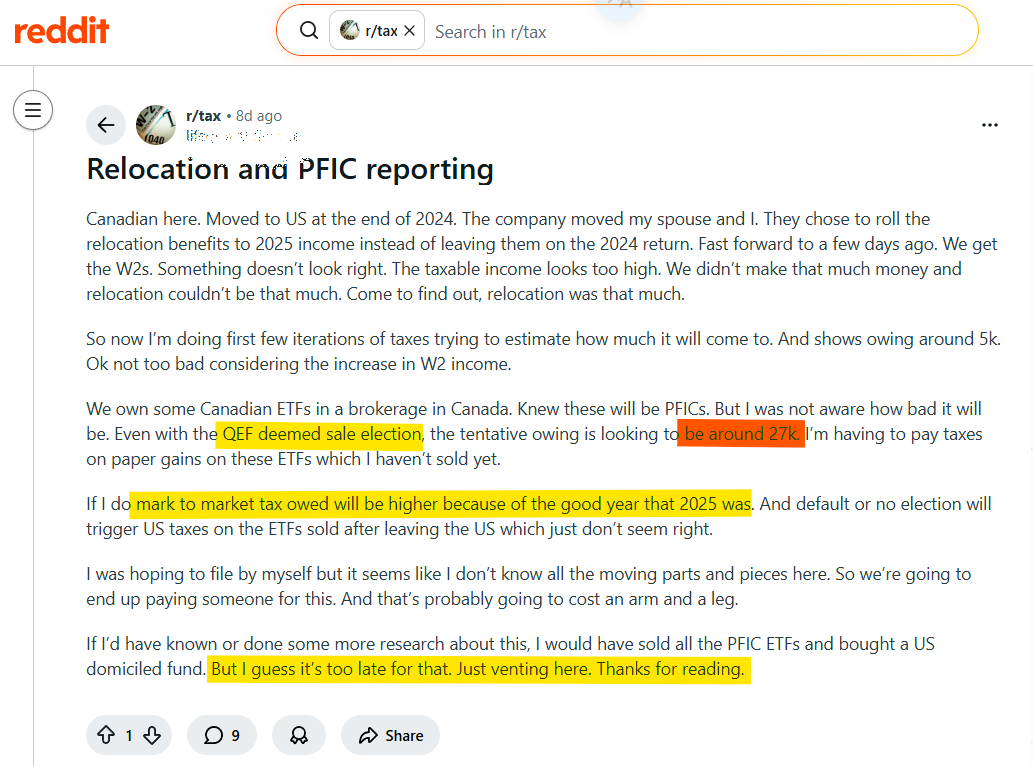

Form 8621 Case Study: Canadian ETFs Brought Into the U.S. Tax System (Real-World Scenario)

This technical analysis is based on a real-world scenario from the r/tax community. It illustrates the immediate tax impact of foreign holdings when the complexity of U.S. international tax rules meets the shock of “phantom” taxation on non-U.S. assets.

- The Relocation Benefit Trap: Company benefits rolled into the following year’s income, bloating the W-2 and creating an unexpectedly high base tax liability before PFIC is even considered.

- The $27k “Paper Tax” Shock: Attempting a QEF “Deemed Sale” purging election to start clean, only to find it requires paying massive tax on unrealized gains in funds that have not been sold.

- Market Timing Misery: Fear that choosing MTM during a bull market (like 2025) will result in even higher taxes than the QEF route, creating a “no-win” scenario.

- Section 1291 “Ghost” Method: Panic over the default method’s complexity and the fear it will trigger U.S. taxes on ETFs long after the taxpayer leaves the U.S.

- Avoidable Regret: The realization that simply liquidating all PFIC funds before moving would have solved everything, but it is now “too late for that.”

- “Cost an Arm and a Leg”: The feeling that the reporting is too complex to handle alone, and expert help will be prohibitively expensive.

Form 8621 Exit Strategy: Does PFIC Tax Apply After Terminating U.S. Residency?

A major source of anxiety—among temporary U.S. residents—is the fear that PFIC liabilities follow you like a "ghost" after you leave the United States. This misunderstanding of U.S. tax jurisdiction can be definitively debunked using the tax code itself.

The Jurisdictional Anchor for PFIC Liabilities

Under IRC §1291, the excess distribution regime applies only when a United States person receives a distribution or disposes of PFIC stock. Treasury Regulation §1.1291-1 further clarifies that PFIC rules apply only during periods in which the shareholder is a United States person.

Implication for Former U.S. Taxpayers Selling PFICs

Once an individual ceases to be a U.S. person (for example, by becoming a nonresident alien), future gains from the sale of foreign PFIC stock are generally outside U.S. tax jurisdiction. This is primarily because nonresident aliens are generally not taxed on foreign-source capital gains under IRC §865.

Practical Conclusion on Pre-Residency Fund Sales

For internationally mobile professionals, PFIC taxation effectively applies only during the period of U.S. tax residency. Once U.S. tax residency ends, future dispositions of foreign funds are generally outside the scope of the PFIC regime.

"Temporary Residents only pay while 'Under the Flag'. Departure terminates the PFIC obligation permanently."

PFIC Tax Savings Comparison: Simulating QEF vs. MTM vs. Section 1291 Scenarios

Based on the actual growth trajectories of VUN, XEC, and XEQT from 2020 to 2025, it is clear why the investor hesitated to liquidate. For internationally mobile professionals, the choice of reporting method determines whether these significant gains become a tax-free legacy or a massive financial drain.

Form 8621 Simulation Model: 3-Year PFIC Tax Projection

To calculate the mathematical impact, we use a simulation based on the investor's likely $1,000,000 portfolio (derived from the $30k+ MTM tax exposure in 2025). We assume the investor continues to hold (no sales) these assets until departing the U.S. in late 2027.

- Portfolio FMV: ~$1,000,000 (CAD/USD equivalent total).

- Growth Trajectory: 10% annual appreciation (In-line with 2020-2025 data).

- Scenario Window: 3 Tax Years (2025 – 2027) for direct comparison.

- Professional Fees: $300 benchmark fee per Form 8621 annually.

- Reporting Volume: 6 Form 8621s (VUN, XEC, and XEQT layers).

Note: All figures below represent the 3-year cumulative totals (2025–2027) for the simulation.

Pay tax on AIS earnings (Ordinary Earnings Per Share). Based on verified 2024 iShares (XEQT) and Vanguard (VUN) AIS filings.

| IRS Tax Liability | $10,200 |

| Professional Compliance | $5,400 |

| Total Cost | $15,600 |

Taxing 10% annual paper growth at ordinary rates. Purely a cost center in a bull market.

| IRS Tax Liability | $106,000 |

| Professional Compliance | $5,400 |

| Total Cost | $111,400 |

Zero tax exit. Maintaining the default status with no asset liquidations while in the U.S.

| IRS Tax Liability | $0 |

| Professional Compliance | $5,400 |

| Total Cost | $5,400 |

No Basis Step-up utilized.

| Gain | $650,000 |

| AIS Tax | $10,200 |

| Sales Tax (LTCG) | $130,000 |

| CPA & Compliance Fee | $5,400 |

| Liquidation Total | $145,600 |

Selling is identical to holding. §1296(l) Basis used.

| Gain (2027) | $100,000 |

| Prior MTM Tax (25-26) | $71,000 |

| Sales Tax (2027) | $35,000 |

| Historical Gain Tax (20%) | $70,000 |

| CPA & Compliance Fee | $5,400 |

| Liquidation Total | $181,400 |

Interest only accrued from 2025 residency.

| Gain | $650,000 |

| Pre-Resident Tax | $150,300 |

| Resident Tax + Interest | $94,700 |

| CPA & Compliance Fee | $5,400 |

| Liquidation Total | $250,400 |

Frequently Asked Questions: PFIC First-Year Election for New U.S. Tax Residents

1. Is there a PFIC first-year exception for new U.S. residents?

There is no blanket “PFIC first-year exception” that makes foreign funds tax-free. The real opportunity is a first-year election window. If the fund is a PFIC, a timely QEF election may be available if the fund provides a valid PFIC Annual Information Statement, or a §1296 MTM election may be available for marketable PFIC stock. If no valid election applies, §1291 generally controls excess distributions and dispositions.

2. What is a PFIC, and do foreign mutual funds or ETFs usually qualify?

A PFIC is a foreign corporation that meets the passive income test or passive asset test under IRC §1297. Foreign mutual funds, ETFs, UCITS funds, unit trusts, investment-linked funds, and similar pooled investment vehicles commonly require PFIC review. They should not be treated like ordinary foreign stocks without checking the fund structure.

3. What if my foreign fund does not provide a PFIC Annual Information Statement?

Without a valid PFIC Annual Information Statement, a QEF election is generally unavailable. This is common for many non-U.S. mutual funds, ETFs, UCITS funds, and investment-linked products. For a new U.S. tax resident, the practical first-year question then becomes whether §1296 MTM is available or whether the fund remains under default §1291.

4. How do I know if my foreign fund is eligible for MTM?

A §1296 MTM election generally requires marketable PFIC stock. Publicly traded foreign ETFs or listed funds may qualify, but private funds, insurance-linked funds, non-listed mutual funds, and many pooled products may not. The exchange, trading status, fund structure, and ownership record should be checked before assuming MTM is available.

5. When does my Form 8621 reporting obligation begin as a new U.S. tax resident?

Form 8621 reporting generally begins once you are a U.S. person and hold, dispose of, receive certain distributions from, or make an election for PFIC stock. For H-1B, L-1, O-1, or TN visa holders, the start date depends on the Substantial Presence Test and the residency start date rules under IRC §7701(b). For green card holders, U.S. tax residency generally begins when lawful permanent residence status starts.

6. Does the $25,000 / $50,000 PFIC reporting exception apply in the first U.S. tax year?

Possibly, but it is limited. The small PFIC exception may reduce annual §1298(f) reporting for certain low-value PFIC holdings, but it does not apply to every situation. It generally does not protect a taxpayer who has an excess distribution, a disposition gain treated under §1291, or a QEF/MTM election requirement. Small balances still need trigger-by-trigger review.

7. Does a foreign tax-free account protect me from PFIC rules?

Usually not by itself. A foreign account may be tax-free or tax-deferred in the local country, but the U.S. may still review the underlying foreign funds for PFIC purposes. ISAs, TFSAs, NRE/NRO investment holdings, and other foreign wrappers need U.S. analysis. Pension or employment-based retirement arrangements should be reviewed separately because treaty, trust, and account-classification issues may also apply.

8. Can a green card holder use the same PFIC exit strategy as an H-1B or L-1 holder?

Not usually. A temporary visa holder may stop being a U.S. tax resident after leaving the United States if the Substantial Presence Test is no longer met. A green card holder generally remains a U.S. person until lawful permanent resident status is formally abandoned or otherwise terminated. U.S. citizens remain U.S. persons regardless of where they live.

9. Can the Foreign Tax Credit offset PFIC tax and interest?

Foreign tax credits may help with the tax portion in some PFIC calculations, but they do not simply erase PFIC exposure. Under the default §1291 regime, the interest charge is a separate problem and may not be fully offset by foreign tax credits. FTC treatment depends on the income basket, foreign tax type, timing, and the specific Form 8621 calculation.

10. What records should a new U.S. resident collect for first-year Form 8621?

Collect complete fund-level records before preparing the first U.S. return: purchase dates, sale dates, units, distributions, reinvestments, switches, year-end values, currency, exchange rates, cost basis records, broker statements, AIS documents if any, and the exact U.S. residency start date. Form 8621 is usually a transaction-level calculation problem, not just a yes/no filing question.

Not Tax Advice: This case study is provided for educational and illustrative purposes only and does not constitute tax, legal, or investment advice. The analysis is based on simplified assumptions and rounded figures used solely to illustrate PFIC mechanics and potential strategic outcomes. Actual tax results depend on the taxpayer’s specific facts, elections, holding periods, and applicable IRS guidance. This material should not be relied upon for preparing a tax return. Tax laws and interpretations may change, and readers should consult a qualified tax professional for advice specific to their situation. Constructive feedback from the tax community is welcome, and any technical corrections are appreciated.

Current as of May 2026 · Based on Form 8621 (Rev. 12/2025)