Missed vs defective Form 8621 executive summary

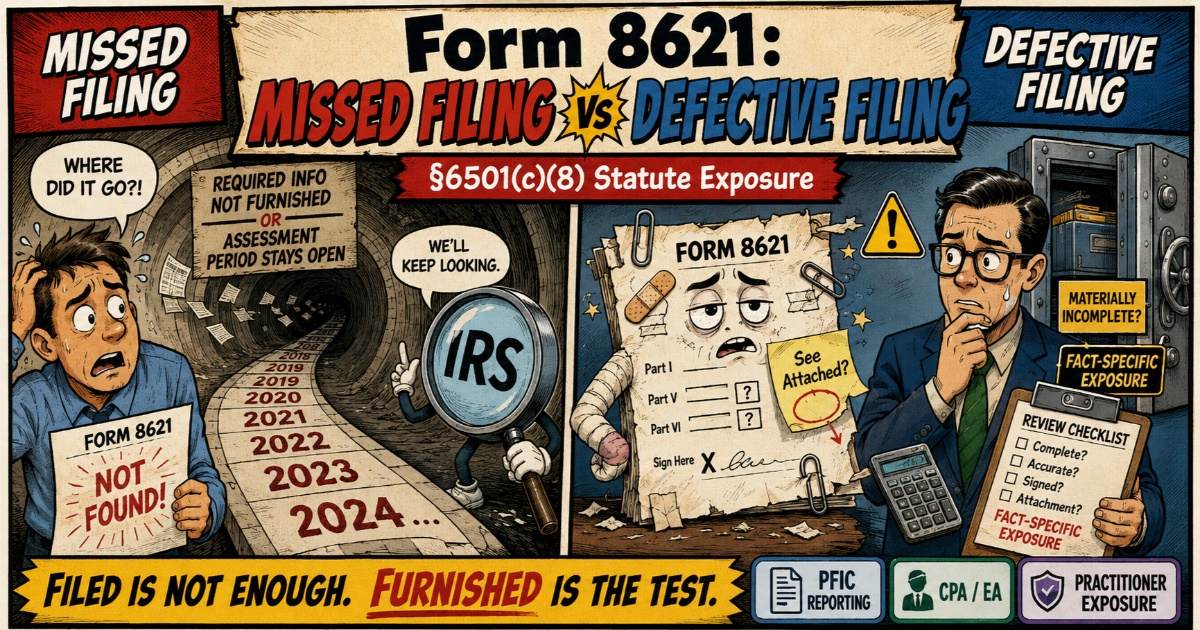

Missed vs defective Form 8621 filings create different legal consequences. A completely missed Form 8621 can leave the tax year open under IRC §6501(c)(8) until the required PFIC information is furnished and the applicable assessment period later expires. A filed Form 8621 may start the §6501(a) assessment period only if it furnishes the information required under §1298(f) with enough specificity to allow the IRS to identify the PFIC item and compute the related tax exposure. A materially incomplete Form 8621 can still leave §6501(c)(8) exposure open.

§6501(c)(8) does not punish arithmetic. It punishes missing information. Under §6501(c)(8)(A), the assessment period does not expire before 3 years after the IRS receives the information required under §1298(f). A clean Form 8621 starts closure. A blank Form 8621 does not. A materially defective Form 8621 sits in the danger zone: filed on paper, but potentially not “furnished” for §6501(c)(8) purposes.

Missed Form 8621 filing and §6501(c)(8) open statute exposure

Authority: IRC §6501(c)(8)

Failure to file Form 8621 for a PFIC subject to §1298(f) reporting requirements can keep the related assessment period open until the required information is furnished and the applicable period later expires. The failure point is statutory: no required §1298(f) information, no §6501(c)(8) closure.

1. The Assessment Period Stays Open Until Required Information Is Furnished

Under §6501(c)(8)(A), the assessment period for tax with respect to any return, event, or period to which the missing PFIC information relates does not expire before 3 years after the required information is furnished. This is not merely an arithmetic correction rule; it is an information-furnishing rule.

Taxpayer A held a PFIC from 2012–2020 and sold it in 2020. They filed their Form 1040 timely each year but omitted Form 8621.

Result: Despite the general 3-year statute expiring, the missing §1298(f) information can keep assessment exposure open for the PFIC-related return, event, or period. If an audit begins later, the examiner may require reconstruction of the acquisition lots, annual PFIC status, distributions, disposition gain, and §1291 tax and interest mechanics going back to the holding period.

2. IRS May Examine More Than the PFIC Line Item

Under §6501(c)(8)(A), failure to furnish §1298(f) information keeps open the assessment period for tax “with respect to any tax return, event, or period to which such information relates.” Under §6501(c)(8)(B), if the taxpayer proves reasonable cause and not willful neglect, the extension is limited to the item or items related to the failure. Without reasonable cause, the taxpayer loses the statutory limitation in §6501(c)(8)(B), creating broader exposure for the return, event, or period to which the missing PFIC information relates.

See IRM 20.1.9 (International Penalties) for examiner guidelines on assessing penalties for failure to file information returns.

3. §1291 Interest Uses the Code’s Underpayment Interest Mechanics

Under IRC §1291(c), the deferred tax amount is treated as an underpayment for the relevant prior PFIC allocation year. Interest then runs under the Code’s underpayment interest mechanics, including §6601, the rate rules under §6621, and daily compounding under §6622 where applicable. Interest applies separately to each allocation year under §1291(c)(3).

For a deep dive, see our guide on PFIC Interest Calculation Mechanics.

Defective Form 8621 filing and fact-specific statute exposure

Authority: IRC §6501(a), §6694

1. Filing May Start the Clock Only if Required Information Was Furnished

The critical distinction is whether the filed form furnishes the information required to be reported. A filed Form 8621 may start the §6501(a) assessment period only if it identifies the PFIC item and provides enough data for the IRS to evaluate the related tax exposure. A materially incomplete filing can remain exposed under §6501(c)(8).

- Standard Period: 3 years per §6501(a).

- Substantial Omission: 6 years per §6501(e)(1)(A) if omitted gross income exceeds 25%.

2. The Danger Zone: The Beard Line of Cases

Under the Beard line of cases, a document generally must provide sufficient data, purport to be a return, represent an honest and reasonable attempt to satisfy the tax law, and be signed under penalties of perjury.

- It must contain sufficient data to calculate tax liability.

- It must represent an honest and reasonable attempt to satisfy the tax law.

- It must purport to be a return.

- It must be executed under penalties of perjury.

A Form 8621 filed with “See Attached” but no calculation statement may fail to furnish the required information for §6501(c)(8) purposes. For a detailed breakdown of the required attachment logic, see Form 8621 Line 16a Statement.

Form 8621 missed filing vs defective filing risk matrix

A summary of exposure based on filing status:

| Scenario | SOL | Audit Scope | Interest Exposure | Practitioner Risk |

|---|---|---|---|---|

| Missed Form 8621 | Does not expire before 3 years after required §1298(f) information is furnished | Broad unless §6501(c)(8)(B) reasonable cause limits scope | §1291(c) deferred tax charge plus §6601 / §6621 / §6622 interest mechanics where tax exists | Extreme |

| Filed but materially incomplete | Disputed; may remain open under §6501(c)(8) if required information was not furnished | PFIC item or broader return/event/period depending facts | Same as applicable PFIC regime | High |

| Filed but computationally wrong | Usually §6501(a) 3 years; §6501(e) may apply if substantial omission exists | Generally finite | Underpayment interest; §1291(c) if excess distribution or disposition gain exists | Moderate |

| De minimis exception applies | No annual §1298(f) filing duty for that PFIC year | None from Form 8621 annual reporting | None from annual reporting | Low |

Table 1: Form 8621 Compliance Risk Comparison Matrix.

For Form 8621 filing exemptions, annual §1298(f) reporting exceptions, and de minimis thresholds, see Form 8621 Filing Exemption Rules.

Form 8621 remediation workflow for closing an open year

Remediation typically involves filing delinquent or corrected forms for years still open under §6501(c)(8) or another applicable limitations rule. Accurate calculation often requires a full historical reconstruction.

For late PFIC cleanup strategy and streamlined filing considerations, see PFIC Streamlined Filing.

Do not remediate only the sale year. Under §1291(a), gain on disposition is treated as an excess distribution and allocated across the shareholder’s holding period. Under §1291(c), prior-year allocations trigger deferred tax and interest mechanics. Therefore, a 2020 sale can require rebuilding acquisition lots, distributions, foreign tax paid, exchange rates, and PFIC status back to 2012.

- Identify PFIC Years: Determine the start of the holding period.

- Retrieve Transaction History: Gather all buy/sell/dividend data.

- Reconstruct Basis (FIFO): Match lots strictly (No Average Basis). See Why Excel Fails for PFIC.

- Allocate Excess Distributions: Apply §1291 ratio to prior years.

- Compute Interest: Calculate daily compounded interest per allocation year.

- File Delinquent 8621s: Submit forms with the required PFIC information so the §6501(c)(8) assessment period can begin to close.

Typical cross-border cleanups we process include Korean ETF holders who never filed Form 8621, Taiwan ETF investors with missed years, and Hong Kong MPF participants with years of missed filings.

1. Why Excel is Insufficient for Remediation

Spreadsheets lack the rigid logic controls required for §1291 compliance. Common failure points include:

- Failure to track FIFO lot matching.

- Inability to lookup historical U.S. marginal tax rates.

- Lack of Undistributed Earnings tracking.

See Form 8621 Line 16a Statement for examples of required documentation.

Common Form 8621 practitioner errors that create PFIC exposure

We frequently observe the following compliance errors in amended returns:

- Netting Gains and Losses: Improperly offsetting PFIC losses against PFIC gains. §1291 does not permit loss recognition until final disposition. See Can PFIC Gains and Losses Be Netted?

- The “Zero Distribution” Fallacy: Assuming no distributions means no filing is required, ignoring the aggregate value check.

- Misapplication of the Threshold: Believing the $25,000 exception applies even when there is a disposition or excess distribution.

- Misclassifying Dispositions: Reporting PFIC sales on Schedule D as capital gains instead of Form 8621 Part V.

- Incomplete Disclosures: Filing the form with only the entity name, leaving financial data blank.

Form 8621 preparer risk for CPAs and EAs

Under §6694(a), an unreasonable position can trigger preparer penalties where the Form 8621 position lacks substantial authority or adequate disclosure. Under §6694(b), willful, reckless, or intentional disregard creates a higher penalty regime.

Under §6501(c)(8), the client’s open-statute problem also creates long-tail engagement risk: the PFIC issue can surface years after the original return was prepared. A blank Form 8621 is worse than an ugly Form 8621 with a defensible calculation statement. The former may fail to furnish required §1298(f) information. The latter creates a record.

Form 8621 missed and defective filing FAQ for EAs and CPAs

If my client missed Form 8621, do I need to amend the Form 1040?

If the recomputation creates additional Section 1291 or Section 1296 tax, an amended return is generally required so the underpayment can be assessed. If the year has no PFIC tax effect, practitioners commonly file the missing Form 8621, sometimes with a “no-change” 1040-X, to furnish the required PFIC information and begin closing the §6501(c)(8) exposure.

A prior PFIC calculation was wrong — how far back should I recompute?

The most reliable method is to rebuild the PFIC history from the beginning. For both §1291 and §1296, any error in distributions, MTM adjustments, or basis figures makes all subsequent years unreliable. And because identifying the first inaccurate year usually takes more time than reconstructing the entire timeline, starting from year one produces the cleanest and most defensible result — you can’t repair a bad foundation; you rebuild it.

If the PFIC was sold at a loss and there is no tax, do I still need to file Form 8621?

Usually yes, unless a reporting exception applies.

A recognized gain on direct or indirect disposition is an explicit Form 8621 trigger. A loss disposition may still require Form 8621 under the annual §1298(f) reporting regime unless the shareholder qualifies for an exception under Treas. Reg. §1.1298-1(c), including the de minimis exception.

For a §1291 fund, a pure loss is generally not taxed under the §1291 excess-distribution regime. The loss is handled under normal realization and loss-limitation rules. But the reporting question is separate from the tax computation question.

Related PFIC Technical Guides

PFIC Classification and Filing Basics

- 🔗 What Is a PFIC under IRC §1297?

- 🔗 Form 8621 Filing Exemption Rules for PFIC Stock

- 🔗 What to Do After Discovering a PFIC

- 🔗 Never Filed Form 8621 for a PFIC?

PFIC Tax Methods and Calculations

- 🔗 PFIC Excess Distribution Calculator

- 🔗 QEF Election Guide

- 🔗 §1291 vs QEF vs MTM

- 🔗 Form 8621 Line 16a Statement

- 🔗 Why Excel Fails for PFIC

Sources and References

- 🔗 IRC §6501(c)(8): Assessment period for international information returns.

- 🔗 IRC §§1291 and 1298(f): Excess distribution mechanics and PFIC reporting requirement.

- 🔗 IRC §§6601, 6621, 6622: Underpayment interest rules, rates, and daily compounding mechanics.

- 🔗 Treas. Reg. §1.1298-1: Section 1298(f) annual PFIC reporting rules and exceptions.

- 🔗 IRS Form 8621 and Instructions: Official IRS guidance for PFIC reporting obligations.

Current as of May 2026 · Based on Form 8621 (Rev. 12/2025)