Quick Answers for U.S. Taxpayers in Germany with UCITS ETFs

Are German ETF-Sparpläne PFICs for U.S. taxpayers?

Are VWCE, VWRL, EUNL, IWDA, CSPX or VUAA PFICs?

Does German Vorabpauschale or Abgeltungsteuer solve PFIC reporting?

Are German retirement or insurance wrappers protected from PFIC rules?

Germany PFIC Risk Summary

- DRV state pension: usually the cleanest German retirement pillar from a PFIC perspective because the taxpayer does not directly hold individual fund shares during accumulation.

- ETF-Sparplan with IE/LU UCITS ETFs: high PFIC review risk due to automated lot creation and foreign fund wrapper.

- Riester Fondssparplan: complex; U.S.-Germany treaty, FBAR, and fund-level PFIC review required.

- Rürup / fondsgebundene Basisrente: complex; insurance wrapper classification, treaty protection, and fund-level review required.

- bAV / company pension: employer contributions, plan type, and underlying fund-linked options require U.S. tax and pension review.

- U.S.-domiciled ETFs via IBKR or U.S. broker: generally not PFIC stock (though local tax and broker restrictions apply).

Why German Depots, UCITS ETFs and ETF-Sparpläne Create PFIC Risk

For U.S. citizens, green-card holders, and U.S. tax residents living in Germany, the ordinary German investment account can become a PFIC file. The risk usually starts with normal local investing: an ETF-Sparplan, a Depot at Trade Republic or ING, a Deka fund bought through Sparkasse, a DWS fund bought through Deutsche Bank, an MSCI World UCITS ETF, or a private pension wrapper holding investment funds.

The German tax system may treat these products as ordinary investment funds subject to Abgeltungsteuer, Vorabpauschale, Teilfreistellung, or local pension tax rules. The U.S. tax system asks a different question: does the taxpayer directly or indirectly own shares in a foreign corporation that meets the passive income or passive asset test under IRC §1297?

The U.S. analysis follows the fund vehicle. A UCITS ETF tracking the S&P 500, MSCI World, or FTSE All-World can still be a PFIC if the fund itself is Irish, Luxembourg, German, or otherwise non-U.S. domiciled. The index exposure does not turn the fund into a U.S.-domiciled ETF.

See: What Is a PFIC?

Germany PFIC Risk Matrix: ETF-Sparplan, Depot Funds, Riester, Rürup and Insurance Wrappers

🔴 High — Form 8621 review usually required

🟡 Review — Structure, ownership and treaty position control the result

🟢 Low — Usually outside PFIC rules, but FBAR / Form 8938 / income reporting may still apply

| Asset / Platform | Risk | U.S. PFIC Issue |

|---|---|---|

| ETF-Sparplan holding UCITS ETFs | 🔴 | Automated monthly purchases require PFIC lot-level tracking. |

| Trade Republic / Scalable Capital | 🔴 | Platform does not control PFIC; fund domicile does. |

| ING / DKB / Comdirect / Consorsbank | 🔴 | Broker tax reports do not replace Form 8621. |

| VWCE / EUNL / IWDA / CSPX / VUAA | 🔴 | Ireland- or Luxembourg-domiciled UCITS ETFs. |

| Deka / DWS / Union Investment funds | 🔴 | German or Luxembourg fund wrapper; separate review. |

| German money market funds | 🔴 | Cash-like yield may still be a Geldmarktfonds or non-U.S. pooled fund, not a bank deposit. |

| Fondsgebundene Rentenversicherung | 🔴/🟡 | Insurance classification and sub-fund review. |

| Riester / Rürup pension options | 🔴/🟡 | Pension classification and fund-level review. |

| bAV / company pension funds | 🟡 | Treaty and ownership facts control the U.S. result. |

| German direct stocks: SAP, Siemens | 🟢/🟡 | Lower PFIC risk; operating-company facts matter. |

| Tagesgeld / Festgeld / bank deposits | 🟢 | Usually not PFIC; FBAR/8938 reporting applies. |

| German government bonds | 🟢 | Direct debt is not PFIC; income reporting applies. |

| U.S.-domiciled ETFs: VOO, VTI, SPY | 🟢 | Generally avoid PFIC; German tax review needed. |

Popular German UCITS ETF PFIC Examples: VWCE, EUNL, IWDA, CSPX, VUAA and SXR8

Common investment products and platforms in Germany and their U.S. tax implications. The underlying fund vehicle's registration and domicile determine the PFIC outcome, not the broker or local tax-free status.

| German Fund / ETF | Why It Matters for PFIC | U.S.-Domiciled Alternative |

|---|---|---|

| VWCE — Vanguard FTSE All-World Accumulating | IE00BK5BQT80 · Ireland-domiciled UCITS ETF · not the same as VT | VT |

| VWRL — Vanguard FTSE All-World Distributing | IE00B3RBWM25 · Ireland-domiciled UCITS ETF · distributions need EUR/USD review | VT |

| EUNL / IWDA — iShares Core MSCI World | IE00B4L5Y983 · Irish UCITS wrapper · commonly requires PFIC review | URTH / VT |

| CSPX / SXR8 — iShares Core S&P 500 | IE00B5BMR087 · S&P 500 exposure but not VOO | VOO / IVV / SPY |

| VUAA — Vanguard S&P 500 UCITS ETF | IE00BYX2JD69 · Irish UCITS wrapper | VOO |

| EIMI — iShares Core MSCI EM IMI | IE00BKM4GZ66 · emerging markets UCITS wrapper | IEMG |

| Xtrackers MSCI World UCITS ETF — XDWD / variants | Ireland or Luxembourg UCITS wrapper depending on share class; domicile and fund wrapper require PFIC review | URTH / VT |

| Amundi MSCI World UCITS ETF — CW8 / variants | LU1681043599 · Luxembourg-domiciled UCITS ETF · foreign fund wrapper commonly requires PFIC review | URTH / VT |

| Deka / DWS / Union Investment funds | German or Luxembourg retail fund wrapper; German tax report is not Form 8621 support | U.S. ETFs / direct stocks |

VWCE Is Not VT: German UCITS ETFs vs. U.S.-Domiciled ETFs

Rule: VWCE is not VT. CSPX is not VOO. EUNL / IWDA are not U.S. ETFs. The index may be similar, but the fund wrapper is different. PFIC classification follows the fund domicile and legal vehicle, not the index exposure.

Why Americans in Germany Buy UCITS ETFs Instead of VOO, VTI or SPY

Many German retail brokers (such as Trade Republic, Scalable Capital, comdirect, or ING) restrict retail investors from buying U.S.-domiciled ETFs because U.S. ETFs usually do not provide EU/UK-style PRIIPs Key Information Documents (KIDs). This does not create the PFIC rule itself, but it creates a practical trap: U.S. taxpayers in Germany are often pushed toward buying locally available UCITS ETFs such as VWCE, EUNL, CSPX, or VUAA, which commonly require PFIC review.

One common PFIC-reduction strategy is holding U.S.-domiciled ETFs through a U.S. or international brokerage account, where legally and practically available, as these escape PFIC classification. U.S. citizens should review their brokerage options before assuming they are forced to hold PFIC-eligible UCITS ETFs in Germany.

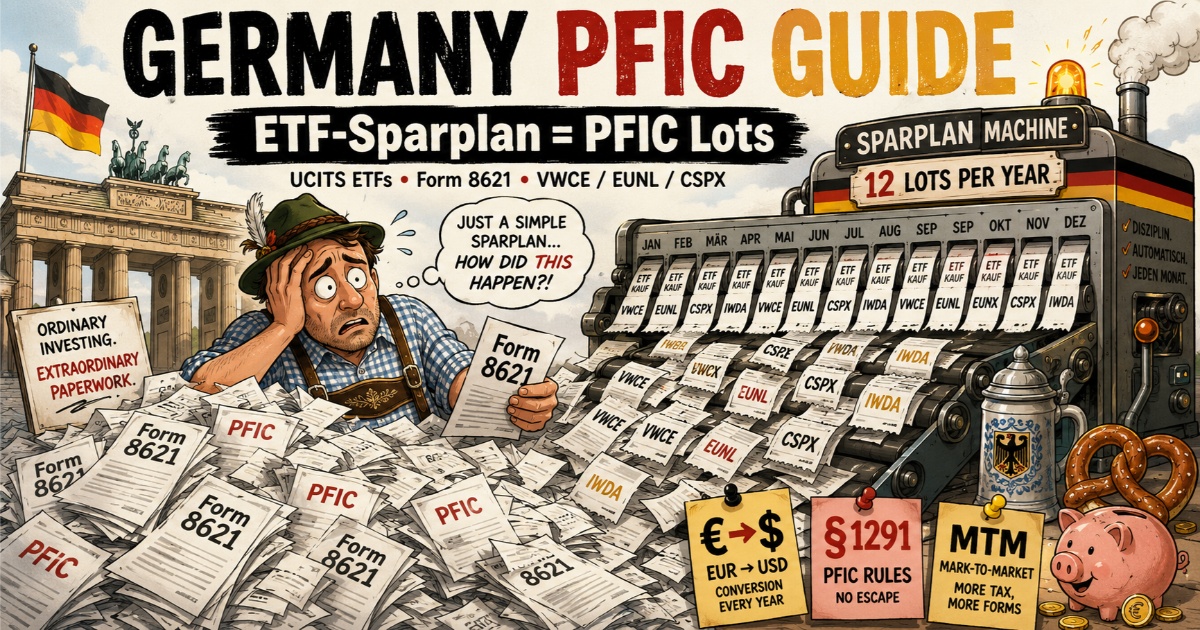

ETF-Sparplan PFIC Problem: 12 New Form 8621 Lots per Year

German ETF-Sparpläne are convenient locally, but they create a significant lot multiplication problem for U.S. tax purposes. A monthly savings plan creates 12 acquisition lots per year for each fund. A 10-year Sparplan into VWCE or EUNL can create 120 acquisition lots before distributions, accumulation income, sales, switches, EUR-to-USD conversion and PFIC election history are even reviewed.

Reconstructing these transaction histories for a default §1291 calculation can be extremely time-consuming and expensive. While a timely §1296 MTM election can significantly reduce future §1291 lot reconstruction problems, the election must be reviewed fund by fund and filed on time. Every lot must still be tracked for basis, meaning that a systematic data solution is needed to avoid compliance failure.

Vorabpauschale, Abgeltungsteuer and Form 8621: Why German Tax Reports Are Not Enough

The German Investmentsteuerreform introduced the Vorabpauschale (deemed advance tax) to tax accumulating funds. While this tax may create German tax paid that is relevant for foreign tax credit (FTC) review, it does not replace Form 8621. Vorabpauschale is a German tax concept and should not be treated as a substitute for a U.S. PFIC distribution, disposition, MTM inclusion, or Form 8621 calculation. Its U.S. treatment and any related foreign tax credit impact require separate review.

For U.S. tax purposes, a PFIC calculation under the default §1291 rules or the MTM election requires actual distributions, realized gains or losses, and U.S. tax basis. This mismatch means that German tax statements cannot be used as a substitute for Form 8621 workpapers. U.S. taxpayers must calculate their U.S. tax positions independently using actual trade dates and transaction spot exchange rates.

U.S.–Germany Tax Treaty: Riester, Rürup, bAV and PFIC Classification

Germany has a comprehensive income tax treaty with the United States. However, the Treaty's Saving Clause preserves the right of the United States to tax its citizens and tax residents as if the treaty had not come into effect. German investment wrappers that defer or reduce German tax do not automatically control the U.S. tax classification of the underlying assets.

- A fondsgebundene Rentenversicherung wrapper does not automatically eliminate Form 8621.

- A Riester or Rürup pension wrapper does not automatically shield underlying non-U.S. pooled funds from PFIC rules.

- A betriebliche Altersversorgung (bAV) company pension requires separate pension and treaty classification review.

Popular wrappers that defer or eliminate domestic taxes (such as a private fondsgebundene Rentenversicherung or a standard Depot) do not automatically shield underlying non-U.S. pooled funds. If the wrapper holds non-U.S. mutual funds, UCITS ETFs, or sub-funds, PFIC classification under IRC §1297 may still occur, requiring Form 8621 reporting unless a specific treaty or statutory exception applies.

German Retirement and Pension PFIC Review: DRV, Riester, Rürup, bAV and Fondsgebundene Rentenversicherung

German pension and insurance products have complex U.S. tax implications. The legal wrapper and the underlying investments must be analyzed separately to determine FBAR, Form 8938, and Form 8621 reporting duties.

| German Pension / Wrapper | U.S. Review Issue | PFIC Risk |

|---|---|---|

| DRV / gesetzliche Rentenversicherung | Usually social-security style analysis; no individual fund ownership during accumulation | Low PFIC risk |

| Riester Banksparplan | Bank savings structure; interest income, FBAR, and treaty review | Lower PFIC risk |

| Riester Fondssparplan | Fund-based retirement product; treaty and fund-level review | High / complex |

| Rürup / Basisrente fondsgebunden | Pension and insurance classification plus fund-level review | High / complex |

| bAV / betriebliche Altersversorgung | Employer benefit, contribution timing, pension classification and fund review | Complex |

| Fondsgebundene Rentenversicherung | Insurance classification and sub-fund review under IRC §7702 | High / complex |

Form 8621 Filing Triggers for Germany: Sales, Switches, Sparplan Lots and Insurance Sub-Funds

| German Action | PFIC Trigger | Germany-Specific Example |

|---|---|---|

| UCITS ETF distribution | PFIC distribution analysis | VWRL, distributing FTSE All-World ETF payout |

| Accumulating ETF records / Vorabpauschale | German tax item and U.S. mismatch review | VWCE / IWDA German tax entries do not replace Form 8621 |

| ETF sale | Disposition review | Sell VWCE / EUNL |

| Sparplan purchase | New acquisition lot | Monthly Sparplan |

| Fund switch | Disposition or exchange review | Sell one UCITS ETF and buy another |

| Robo-advisor rebalance | Automated disposition review | Scalable Capital / robo-advisor portfolio rebalance |

| Insurance sub-fund change | Sub-fund disposition review | Fondsgebundene Rentenversicherung allocation change |

| Money market fund redemption | Money market disposition review | Cash-management or money market fund sale |

| QEF or MTM election year | Form 8621 election reporting | Initial election year and continuation years |

| Pledging PFIC stock as collateral | Constructive disposition under §1298(b)(6) | Lombardkredit or margin loan pledge |

Many German platform actions create no obvious German tax warning, but they are not invisible under U.S. PFIC rules. ETF-Sparplan purchases, UCITS ETF sales, fund switches, robo-advisor rebalances, insurance sub-fund changes, accumulating fund records, distributions, elections, and redemptions can all feed a Form 8621 workpaper review.

A defective or missing Form 8621 can keep the limitations period open under IRC Section 6501(c)(8) for items related to the missing information. If the failure is not due to reasonable cause, the exposure can extend beyond the PFIC item.

Already held German PFICs without filing? Start here: What to Do After Discovering a PFIC.

Advanced Warning — Lombardkredit / Margin Loans: Pledging PFIC stock as collateral may create constructive disposition risk under IRC Section 1298(b)(6). U.S. taxpayers using German portfolio loans, margin, or Lombardkredit should review PFIC consequences before assuming no sale occurred.

Risk Scenario: PFIC Section 1291 Tax and Interest Cost Over Time

Table A models a $10,000 PFIC gain under Section 1291 using actual historical U.S. tax rates and compounding interest. Over time, Section 1291 tax and interest can exceed 100% of the gain. Unreported German assets may require voluntary disclosure or Streamlined Filing Compliance Procedures to resolve the exposure.

Table A: PFIC Section 1291 Interest Calculation Over Time

(Single purchase on yyyy-01-01 → sale on 2025-12-31)

| Period | Tax | Interest | % Consumed |

|---|---|---|---|

| 5 years | $3,440 | $590 | 40.3% |

| 10 years | $3,622 | $1,227 | 48.5% |

| 20 years | $3,630 | $2,396 | 60.3% |

| 30 years | $3,689 | $4,891 | 85.8% |

| 33 years | $3,714 | $6,200 | 99.1% |

| 35 years | $3,679 | $6,930 | 106.1% |

German Depot funds and retail accounts are often long-term holdings. Without QEF information or a valid MTM election, a later sale, redemption, or fund switch can trigger §1291 excess-distribution treatment, deferred tax, and IRC §6621 interest. See our §1291 vs MTM 10-Year Tax Comparison to model the cost.

Germany Form 8621 Filing Guide: Depot, UCITS ETF and ETF-Sparplan Data

Step 1: Identify the Account Wrapper

The wrapper does not decide PFIC status by itself. Identify whether the asset is held in:

- Tagesgeld / Festgeld / bank deposits: usually no PFIC stock.

- Depot / ETF-Sparplan: fund-level PFIC review.

- Managed portfolio: test each ETF or fund position.

- Insurance wrapper: if wrapper is not respected as U.S. insurance, test each sub-fund.

- Riester / Rürup: treaty, pension, and PFIC analysis required.

Step 2: Identify the Fund Domicile

Ticker and exchange do not control PFIC status. Domicile and legal form are the first screen.

| Fund | ISIN | Domicile |

|---|---|---|

| Vanguard FTSE All-World UCITS ETF | IE00BK5BQT80 | Ireland |

| iShares Core MSCI World UCITS ETF | IE00B4L5Y983 | Ireland |

| iShares Core S&P 500 UCITS ETF | IE00B5BMR087 | Ireland |

| Vanguard S&P 500 UCITS ETF | IE00BYX2JD69 | Ireland |

Ireland, Luxembourg or German fund domicile usually means PFIC review, not U.S. ETF treatment.

Step 3: Count the PFIC Entities

Form 8621 exposure usually scales by PFIC entity, not brokerage account.

- 5 UCITS ETFs in 1 Depot: potentially 5 PFIC tracks.

- 1 ETF-Sparplan held for 10 years: potentially 120 monthly purchase lots per fund.

- 1 insurance wrapper holding 6 sub-funds: potentially 6 PFIC review tracks.

- 100% U.S.-domiciled ETFs: usually no Form 8621.

De minimis rule: Under Treas. Reg. Section 1.1298-1(c)(2), the $25,000 single / $50,000 joint threshold can remove annual Section 1298(f) reporting for dormant Section 1291 funds only when there is no excess distribution and no gain from sale or disposition during the year.

Step 4: Choose the Treatment Path

| Regime | Germany Reality |

|---|---|

| Section 1291 Default | Default for most German Depot funds if no valid election was made. Triggers excess-distribution tax and IRC Section 6621 interest. |

| Section 1296 MTM | Possible only for marketable PFIC stock regularly traded on a qualified exchange. Often more practical for exchange-traded UCITS ETFs. |

| Section 1295 QEF | Usually unavailable in practice unless the fund provides a valid PFIC Annual Information Statement. German retail funds, Irish UCITS ETFs and Luxembourg UCITS funds rarely provide AIS data suitable for QEF. |

Germany PFIC Case Studies: German Investment Funds, QEF Myths and Form 8621

Case 1 — German Fund-of-Funds: One German Investment Fund Can Become Several PFIC Tracks

Original Case Source: Reddit r/USExpatTaxes — “Taxes with German Investment Fund” ↗

Bad assumption: “My German fund is just one local investment account, and I already listed it on FBAR.”

Local asset: A German investment fund held by a U.S./German dual citizen. The fund combines multiple underlying funds and is managed as one product from the German investor’s perspective.

PFIC issue: A German pooled investment fund may be a PFIC. If the product is a fund-of-funds, the U.S. analysis may not stop at the top-level German account. The underlying fund positions may create separate PFIC tracks, separate holding periods, separate acquisition lots, and separate Form 8621 calculations.

U.S. result: German fund reporting, German tax statements, and FBAR disclosure do not replace Form 8621. If the taxpayer has missed prior U.S. returns, the cleanup may require determining whether PFIC values exceeded the de minimis threshold, whether any sales, switches, reinvestments, or distributions occurred, and whether Streamlined Filing Compliance Procedures should be reviewed before simply selling the fund.

Case 2 — The QEF Election Myth: Why EU Funds Usually Do Not Solve PFIC Reporting

Original Case Source: Reddit r/USExpatTaxes — “PFIC with QEF election in European Union (US citizens)” ↗

Bad assumption: “I can buy European funds in Germany and simply make a QEF election to avoid punitive PFIC treatment.”

Local asset: EU-domiciled funds considered by U.S. citizens moving to Germany and earning in euros.

PFIC issue: A QEF election under IRC Section 1295 is only useful if the foreign fund provides a valid PFIC Annual Information Statement with the required U.S. tax data. Most German retail funds, Irish UCITS ETFs, Luxembourg UCITS funds, and EU platform funds do not provide U.S.-style PFIC AIS data to ordinary retail investors.

U.S. result: Without a valid PFIC Annual Information Statement, QEF is usually not a practical solution. The taxpayer is often left with either the default Section 1291 regime or, where the fund qualifies as marketable stock and the election is timely made, a Section 1296 mark-to-market election. This is why German investors holding VWCE, EUNL, IWDA, CSPX, VUAA, Deka, DWS, Union Investment, or other EU funds should not assume that “QEF election” is available just because an advisor mentions it.

German Broker Data Needed for Form 8621: Trade Republic, Scalable, ING, DKB and Comdirect

To prepare reliable U.S. tax workpapers, you must gather specific historical transaction records from your German platforms. German tax statements are not sufficient on their own.

| Platform | Data Needed for Form 8621 |

|---|---|

| Trade Republic | Sparplan executions, buys, sells, distributions, tax report |

| Scalable Capital | transactions, rebalances, distributions, year-end values |

| ING / DKB / Comdirect / Consorsbank | Depot transactions, ETF purchases, sales, tax statements |

| Flatex / Degiro | transaction CSV, dividend report, position report |

| IBKR | activity statement, FX, trades, dividends |

Lower-PFIC-Risk Investing Options for U.S. Taxpayers in Germany

Managing PFIC compliance can be costly. For U.S. taxpayers looking to reduce or eliminate Form 8621 reporting, the following local options represent alternative investment strategies:

- U.S.-Domiciled ETFs: Holding VOO, VTI, SPY or VT avoids PFIC rules. While local EU PRIIPs rules make these difficult to purchase through German brokers, they can be held through U.S. or international brokers where practically and legally available.

- Direct Operating Stocks: Purchasing individual shares of operating companies (such as SAP, Siemens, Allianz, BMW, or major U.S. individual stocks) does not trigger PFIC rules, as these are operating entities rather than passive funds.

- Direct Government Bonds: Purchasing German government bonds (Bunds) or U.S. Treasuries directly does not trigger PFIC classification.

- Cash Deposits: Standard Tagesgeld, Festgeld, and bank deposits are low-risk cash assets, though interest remains taxable in both jurisdictions.

Related PFIC Technical Guides

- 🔗 What Is a PFIC under IRC Section 1297?

- 🔗 Form 8621 Filing Exemption Rules for PFIC Stock

- 🔗 What to Do After Discovering a PFIC

- 🔗 Section 1291 Excess Distribution and Interest Calculation

- 🔗 Section 1291 vs MTM 10-Year PFIC Tax Comparison

- 🔗 PFIC Foreign Exchange Translation Rules for EUR and USD

- 🔗 PFIC Election Strategy: Section 1291 vs MTM vs QEF

- 🔗 EA vs CPA vs Tax Attorney for PFIC, FBAR, and Streamlined Filing

Germany PFIC FAQ: VWCE, ETF-Sparplan, Vorabpauschale, Riester and Form 8621

Do I need Form 8621 for a German ETF-Sparplan?

Are VWCE, EUNL, IWDA, CSPX or VUAA PFICs?

Does German Abgeltungsteuer eliminate PFIC tax?

Does Vorabpauschale count as PFIC income for U.S. tax?

Can I make a Mark-to-Market election on UCITS ETFs held in Germany?

Can I make a QEF election for German, Irish or Luxembourg funds?

Are Riester or Rürup accounts exempt from PFIC?

Are German investment-linked insurance policies PFICs?

Can I avoid PFIC by buying VOO, VTI or SPY through a U.S. broker?

Does the $25,000 PFIC filing exception apply to German funds?

Does a German Depot need FBAR or Form 8938 if I already file Form 8621?

Are Deka, DWS or Union Investment funds PFICs?

Does Trade Republic or Scalable Capital create PFIC problems?

Is my Trade Republic or Scalable Capital tax report enough for Form 8621?

Sources and References

- 🔗 IRS Form 8621 and Instructions: Official IRS guidance for PFIC reporting obligations.

- 🔗 IRC §§1291–1298: Statutory framework governing PFIC taxation.

- 🔗 Treas. Reg. §1.1296-1: Regulatory rules for Mark-to-Market elections.

- 🔗 U.S.–Germany Income Tax Treaty: Treaty framework for income and pension analysis.