💡 Key Takeaways: Form 8621 Line 15f Compliance

- USD Cost Basis & proceeds: Under IRC §1012 and IRC §1001(b), U.S. taxpayers must calculate PFIC cost basis and sale proceeds in USD on transaction dates.

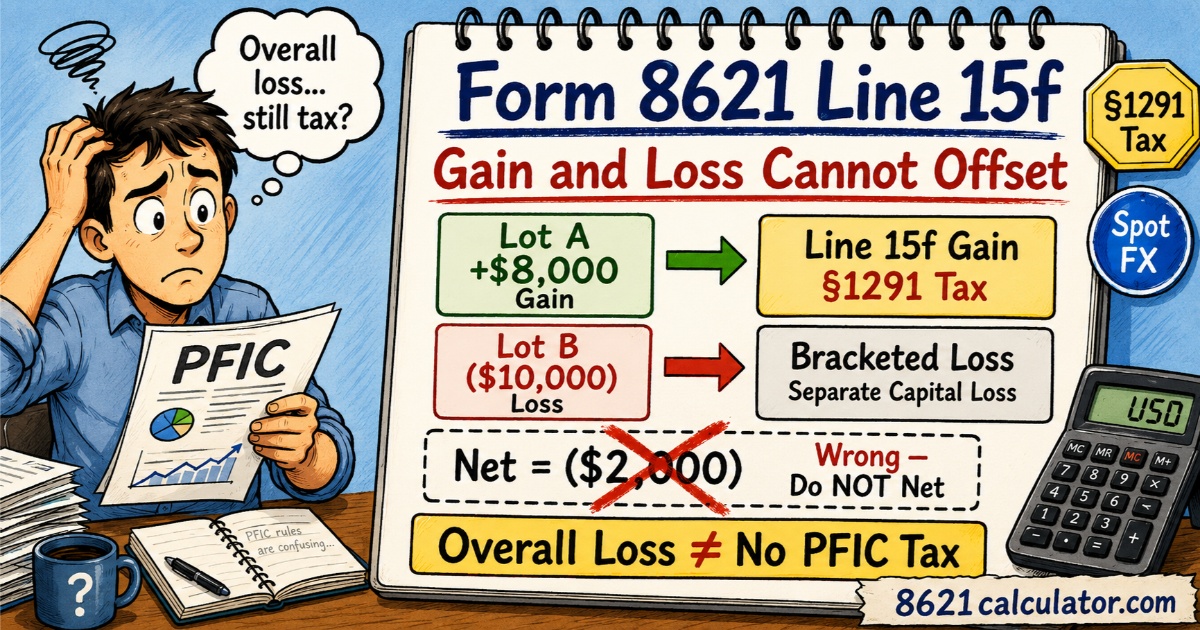

- The No-Netting Mandate: Under §1291, gain lots and loss lots cannot be netted on Line 15f. Gains flow to Line 16 for throwback tax, while losses are reported in brackets.

- Separate Conversion Method: Do not convert the net foreign currency gain to USD at a single rate. Use transaction-date spot FX rates for each purchase and sale separately.

- No Loss Deductions: PFIC losses shown on Line 15f do not offset §1291 ordinary throwback gains or other capital gains on Form 8621.

PFIC Foreign Currency Gain Calculation: USD Basis and USD Proceeds

For a PFIC held in EUR, GBP, AUD, or any non-USD currency, the gain calculation starts in U.S. dollars. For an individual U.S. taxpayer who does not maintain a separate qualified business unit using a functional currency, the PFIC gain calculation is reported in U.S. dollars. The practical result is simple: basis and proceeds must be measured in USD before §1291 is applied. IRC §1012 fixes the USD cost basis on the acquisition date. IRC §1001(b) fixes the USD amount realized on the disposition date.

Use the Separate Conversion Method. Convert each transaction separately. The purchase price converts into USD using the spot rate on the purchase date. The sale proceeds convert into USD using the spot rate on the sale date. Form 8621 Line 15f reports the USD gain:

When the result is a positive USD gain, §1291 treats the full gain as an excess distribution and sends it to Line 16 for the interest-charge computation. Under §1291, asset appreciation and currency movement aggregate into one USD gain. The regime taxes the combined result.

PFIC Losses and the No-Netting Rule on Line 15f

A PFIC disposition loss is still reported on Line 15f. Enter the loss amount in brackets and leave Line 16 blank for that loss item.

When the same PFIC disposition includes both gain lots and loss lots, do not net them. Use separate Part V entries: one Line 15f for the gain lot with Line 16 completed, and another Line 15f for the loss lot in brackets with no Line 16.

| Lot | USD Result | Correct Treatment |

|---|---|---|

| Lot A | $8,000 gain | Line 15f positive amount; complete Line 16. |

| Lot B | ($1,800) loss | Show in brackets; no Line 16. |

| Lot C | $88 gain | Line 15f positive amount; complete Line 16. |

Do not net the three lots into one $6,288 Line 15f number.

Correct treatment: Lot A and Lot C are positive disposition gains. They may be combined into one positive Line 15f amount of $8,088 and carried to Line 16.

If Lot A and Lot C were acquired on different dates, they must be shown separately in the Line 16a workpaper. Lot B is reported separately as ($1,800), with no Line 16. Do not use Lot B to reduce the gain.

Common scenarios for this non-netting rule include VWRA/IWDA disposals reported on Line 15f where different blocks are sold, or calculating the Taiwan ETF 0050 disposition gain basis across multiple historical purchase lots.

Form 8621 Line 15e(2) vs Line 15f

| Issue | Line 15e(2) | Line 15f |

|---|---|---|

| What it reports | Distribution excess | Sale gain or loss |

| Trigger | 125% excess-distribution test | Disposition result |

| Line 16 | Yes, if above zero | Yes, if above zero |

| Loss | Not applicable | Brackets only; no Line 16 |

Some software calculates Line 15e(2) as a negative number, then uses it to reduce Line 15f before running Line 16. That is wrong.

Example: FX Movement Creates §1291 Gain

Buy PFIC shares for £100 when GBP/USD is 1.00. USD basis is $100 under IRC §1012.

Sell the same shares for £100 when GBP/USD is 2.00. USD amount realized is $200 under IRC §1001(b).

Line 15f gain is $100:

Under IRC §1291(a)(2), the $100 gain is treated as an excess distribution. The fact that the foreign-currency price did not move does not matter. The taxable result is measured in USD.

Line 15f Workpaper Checklist

A defensible Line 15f workpaper should preserve:

- PFIC name and identifying number

- Lot-level acquisition date

- Foreign purchase price

- Purchase-date spot FX rate

- USD basis under IRC §1012

- Disposition date

- Foreign sale proceeds

- Sale-date spot FX rate

- USD amount realized under IRC §1001(b)

- USD gain or loss

- §1291 holding-period allocation support

Form 8621 Line 15f Frequently Asked Questions

Do I need Form 8621 if I sold the PFIC at a loss?

Yes, if the sale is a reportable PFIC disposition.

A loss goes on Line 15f in brackets. Line 16 is not completed.

The loss may not create Line 16 tax, but the disposition still breaks the small-holder exception logic.

No gain does not automatically mean no Form 8621.

Can I put a foreign-currency gain on Line 15f?

No. Line 15f reports USD gain or loss. Compute USD proceeds under IRC §1001(b), subtract USD basis under IRC §1012, then apply §1291.

I bought the fund before becoming a U.S. taxpayer. Do I only count the U.S. years?

No.

The original purchase date still matters.

You need the full timeline: purchase date, U.S. residency date, PFIC years, sale date, basis, FX rates, and holding period.

Do not treat this as a “from green card date only” calculation.

Can capital losses offset a positive Line 15f §1291 gain?

No. A positive Line 15f amount enters §1291. Capital losses do not reduce the Line 16 tax-and-interest charge.

What if the PFIC was liquidated, redeemed, or became worthless?

Still analyze Line 15f.

If you received cash, use it as proceeds. If it became worthless, proceeds may be zero.

Either way, compute the USD gain or loss against USD basis.

Is the §1291 interest charge deductible?

Usually no.

The Line 16 interest charge is not margin interest, investment interest, or business interest. For an individual taxpayer, it is generally a nondeductible personal interest-type cost.

It increases the tax bill. It does not create a matching deduction.

Does IRC §988 split out the FX gain from PFIC stock?

No. For a §1291 PFIC stock disposition, Line 15f reports one USD stock gain: USD amount realized under IRC §1001(b) minus USD basis under IRC §1012. IRC §988 does not carve the currency movement out of the PFIC stock disposition merely because the share price is denominated in foreign currency.

Form 8621 Line 15f Sources and References

- 🔗 Instructions for Form 8621: Official IRS instructions for completing Form 8621.

- 🔗 IRC §985: Functional currency rules.

- 🔗 IRC §1001: Amount realized and gain/loss rules.

- 🔗 IRC §1012: Basis rules.

- 🔗 IRC §1291: PFIC excess distribution and disposition rules.

- 🔗 IRS Form 8621 Instructions: Current IRS instructions for Section 1291 fund disposition gain, Line 15f, and deemed sale routing.

- 🔗 Toso v. Commissioner summary: Practitioner summary of the Tax Court's PFIC gain/loss no-netting holding.

Current as of May 2026 · Based on Form 8621 (Rev. 12/2025)