Quick Answer: Where Can I Find a Form 8621 Example, Sample Form, or PFIC Calculation?

You can find Form 8621 examples and sample forms online, but a sample form is only useful if it comes with the PFIC calculation workpaper behind it. Under the default §1291 rules, a simple PFIC sale may require line 15f gain, excess distribution allocation, prior-year tax rates, line 16b current-year allocation, line 16c tax, line 16e net tax, and line 16f interest. A blank form or basic Excel template can show the layout, but it usually cannot safely handle multiple lots, DRIPs, partial sales, foreign currency, prior-year tax rates, or long holding periods.

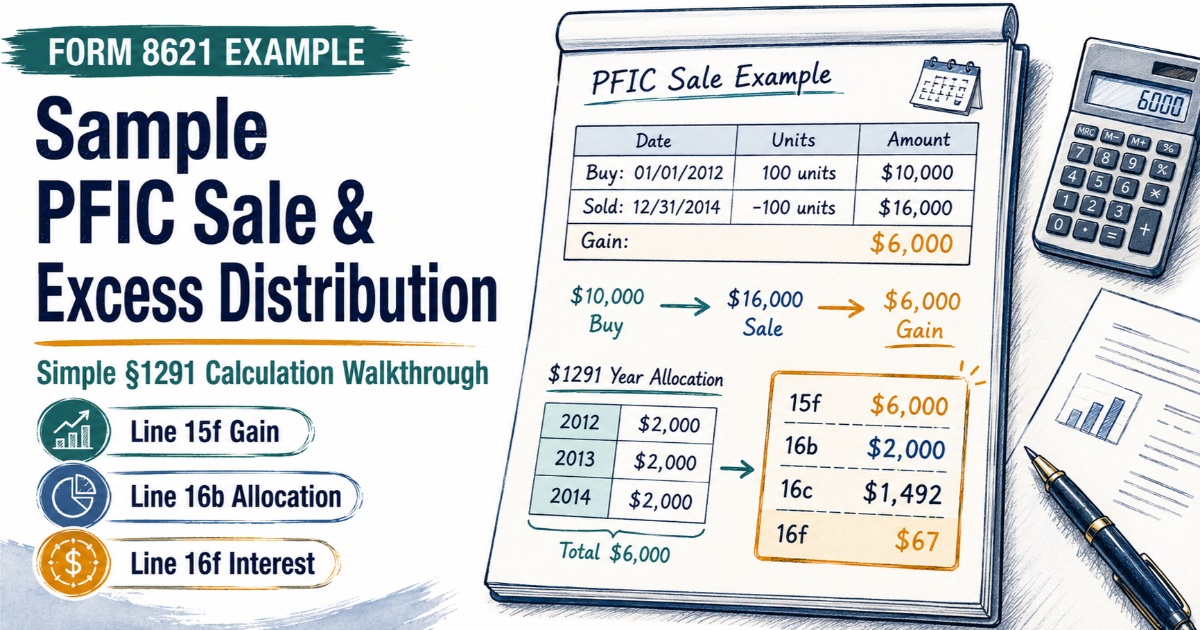

Form 8621 Sample Case: One PFIC Purchase and One Sale

This Form 8621 sample case uses the simplified PFIC sale example published by HodgenLaw: a U.S. citizen buys 100 shares of a foreign mutual fund for $10,000 on January 1, 2012, sells the shares for $16,000 on December 31, 2014, and has no QEF or MTM election.

Form 8621 Sample Case Facts and Transaction Data

The transaction data is intentionally clean:

| Date | Details | Units | Value |

|---|---|---|---|

| 2012-01-01 | Buy | 100 | $10,000 |

| 2014-12-31 | Sold | -100 | $16,000 |

We ran those facts through 8621calculator.com to show how the $6,000 gain becomes a Form 8621-style §1291 excess distribution workpaper, including line 15f, line 16b, line 16c, line 16e and line 16f.

Step 1: Calculate Line 15f Gain From PFIC Disposition

The first calculation is straightforward:

| Line 15f | Gain from disposition of stock of a section 1291 fund | $6,000 |

|---|

Step 2: PFIC Excess Distribution Calculation by Holding Days

Under §1291, the gain is allocated ratably across the holding period. The HodgenLaw template simplifies the holding period as three 365-day years:

Real cases often require exact date counting, acquisition-date rules, sale-date rules, leap years, partial sales, multiple lots and foreign currency support. This template is deliberately simplified to make the concept readable.

Step 3: Form 8621 Line 16b Current-Year and Pre-PFIC Allocation

The current year is 2014, the sale year. The two prior PFIC years are 2012 and 2013. In this simplified example, there are no pre-PFIC years, so line 16b equals the 2014 current-year allocation. The prior-year amounts do not simply become current-year income; they are used to compute the aggregate increase in tax and interest.

| Year | Days | Gain |

|---|---|---|

| 2012 | 365 | $2,000 |

| 2013 | 365 | $2,000 |

| 2014 | 365 | $2,000 |

The “Gain” column shows the portion of the $6,000 PFIC gain allocated to each year under the §1291 excess distribution method.

The 2014 amount is the current-year allocation for line 16b. The 2012 and 2013 amounts are prior-year PFIC allocations used to compute line 16c tax and line 16f interest.

| Line 16b | Amount allocated to the current tax year and pre-PFIC years | $2,000 |

|---|

Step 4: Form 8621 Line 16c, 16e and 16f Tax and Interest

For the prior-year PFIC periods, the allocated amount for each year is multiplied by the highest tax rate applicable for that year. In this simplified template:

| Year | Days | Gain | Rate | Tax | Interest |

|---|---|---|---|---|---|

| 2012 | 365 | $2,000 | 35% | $700 | $43 |

| 2013 | 365 | $2,000 | 39.6% | $792 | $24 |

| 2014 | 365 | $2,000 | |||

| Prior-year aggregate increase in tax | $1,492 | $67 | |||

In Form 8621 terms, the “Tax” column supports line 16c, and the “Interest” column supports line 16f.

Those prior-year tax amounts are aggregated on line 16c. In this simplified workpaper, there is no foreign tax credit on line 16d, so line 16e equals line 16c. The interest charge is reported on line 16f.

Form 8621 Example Calculation Result

The simplified result is:

| Line | Meaning | Amount |

|---|---|---|

| 15f | Gain from disposition of PFIC stock | $6,000 |

| 16b | Amount allocated to current year and pre-PFIC years | $2,000 |

| 16c | Aggregate increases in tax for prior PFIC years | $1,492 |

| 16d | Foreign tax credit | $0 |

| 16e | Net aggregate increase in tax | $1,492 |

| 16f | Interest charge | $67 |

Condensed Workpaper View

| Line 15f | Holding Start | Holding End | Holding Days | Excess Per Day | Line 16b | Line 16c | Line 16d | Line 16e | Line 16f |

|---|---|---|---|---|---|---|---|---|---|

| $6,000 | 01/01/2012 | 12/31/2014 | 1,095 | $5.48 | $2,000 | $1,492 | $0 | $1,492 | $67 |

Why This Is Not a Normal Long-Term Capital Gain Calculation

DIY filers often start with the brokerage statement and think the result is simple: sell price minus cost basis equals long-term capital gain. That is not the default PFIC §1291 method.

In this example, the $6,000 gain is not simply reported as a clean long-term capital gain. It is first treated as a PFIC disposition gain, allocated over 1,095 holding days, split into current-year and prior-year PFIC portions, and then subjected to prior-year tax and interest mechanics. That is why a Form 8621 example must include the calculation support, not only a filled form layout.

PFIC Calculation Check: Is My Form 8621 Calculation Correct?

Many DIY filers are not only looking for a sample Form 8621. They are trying to answer a more practical question: is my PFIC calculation correct? A workpaper is the sanity check. It should show the source transaction, line 15f gain, holding days, daily allocation, line 16b current-year amount, line 16c prior-year tax, any line 16d foreign tax credit, line 16e net tax, and line 16f interest.

If your result cannot be traced from broker records to Form 8621 lines, a preparer or calculator will have a hard time reviewing it. A sample form can show what the answer might look like, but the workpaper shows why the numbers are there.

What This Simple Form 8621 Sample Leaves Out

This sample case is intentionally clean. Real DIY PFIC calculations often become harder when any of these facts appear:

- Foreign currency: CAD, GBP, EUR or INR basis and proceeds may need historical USD translation.

- Multiple purchases or DCA: each lot may create a separate holding-period allocation problem.

- DRIPs: reinvested distributions can create new units, basis and holding periods.

- Partial sales: sold units and remaining basis must be tracked accurately.

- Pre-U.S. residency years: allocated gain may require separate classification.

Use a PFIC Calculator Before Copying a Sample Form 8621

Form 8621 Example and Sample Form FAQ

Where can I find a Form 8621 sample form?

How do I know if my Form 8621 calculation is correct?

Is PFIC gain reported as capital gain or excess distribution?

How is Form 8621 line 15f calculated?

How is Form 8621 line 16f interest calculated?

Can I use this Form 8621 example for TaxAct, TurboTax, OLT or H&R Block?

Does this example cover MTM or QEF?

Sources

- IRS: About Form 8621.

- IRS: Instructions for Form 8621.

- HodgenLaw: Back to Basics: How to Report Gain on the Sale of a PFIC.

Related Form 8621 Calculation Guides

- Can I File Form 8621 Myself? DIY PFIC Calculation Guide

- §1291 Interest Calculation for Form 8621 Line 16f

- PFIC Foreign Currency Translation Rules for Form 8621

- DIY Tax Software for Form 8621

Current as of June 2026 · Based on Form 8621 (Rev. 12/2025)