Quick Answer: FBAR vs Form 8938 vs Form 8621

What does FBAR report?

What does Form 8938 report?

What does Form 8621 report?

Does filing FBAR or Form 8938 replace Form 8621?

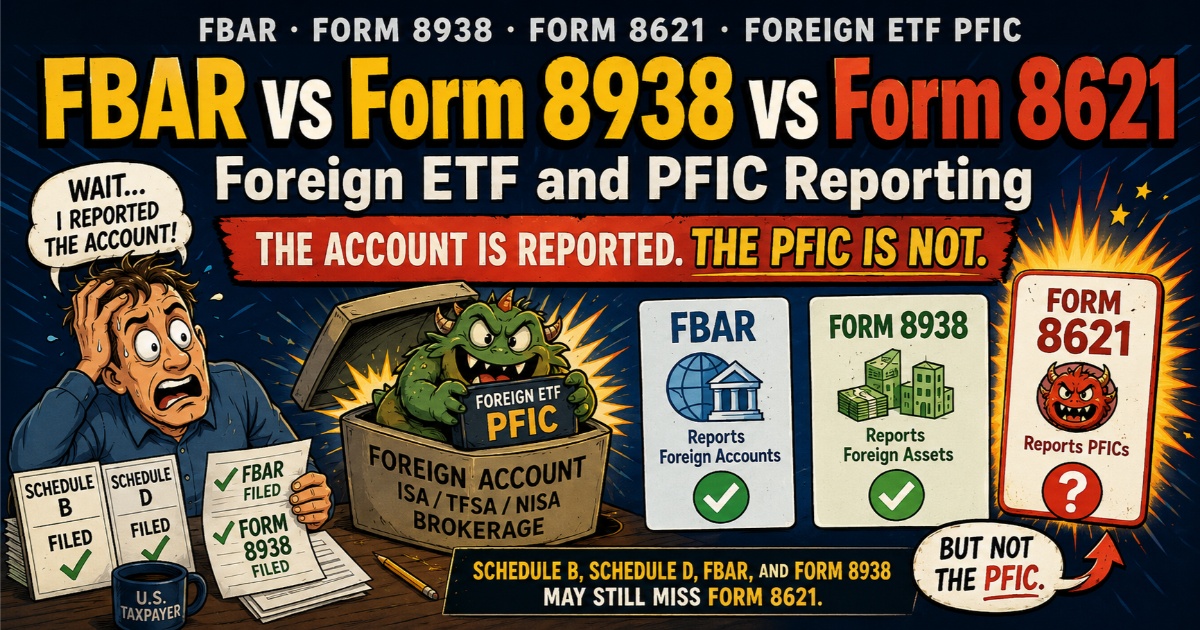

The Golden Rule: Account, Asset, and Fund Are Three Different Things

The most common mistake U.S. expats and their tax advisors make is treating account disclosure as investment reporting.

FBAR and Form 8938 care where the money is held.

Form 8621 cares what the money is invested in.

These are not the same question. They are separate obligations that can overlap but cannot replace each other.

A taxpayer who reports a foreign brokerage account on FBAR and lists the account on Form 8938 has completed account and asset disclosure. If that account holds a foreign ETF or foreign mutual fund, the PFIC question — and Form 8621 — may still be open.

Schedule D Capital Gains Do Not Replace Form 8621

Many taxpayers think they are covered because they reported the foreign account on FBAR or Form 8938, and reported the dividends or capital gains on Schedule B or Schedule D. But for a foreign ETF, foreign mutual fund, UCITS ETF, or other PFIC, that may still be incomplete. The account and income are visible on the return, but the missing Form 8621 is also easier to spot.

FBAR vs Form 8938 vs Form 8621: Side-by-Side Comparison

The table below compares the three forms by what they report, when they are required, and what risk arises if they are missed.

| FBAR (FinCEN Form 114) | Form 8938 (FATCA) | Form 8621 (PFIC) |

|---|---|---|

| What it reports | ||

| Foreign financial accounts | Specified foreign financial assets | PFICs — income, gain, elections, annual reporting |

| Filing trigger / threshold | ||

| Aggregate foreign account value over $10,000 at any time during the year | Starts at $50,000 / $75,000 for U.S.-resident single filers; higher thresholds for joint filers and taxpayers abroad | No single account threshold. Sales, distributions, PFIC elections, or annual reporting may each trigger filing. Small-PFIC exceptions apply in narrow cases. |

| Due date | ||

| April 15, with automatic extension to October 15 | Filed with Form 1040, including extensions | Filed with the income tax return, including extensions |

| Main risk if missed | ||

| Civil penalties; willful cases can be severe | $10,000 initial penalty, continuation penalties, extended statute issues | PFIC tax and interest; missed election timing; §6501(c)(8) statute risk |

What FBAR Reports — and What It Does Not

FBAR is filed with FinCEN, not the IRS. It reports foreign financial accounts — not income, not investments, and not PFIC calculations.

Common FBAR-reportable accounts include:

- Foreign bank accounts and savings accounts

- Foreign brokerage accounts

- Certain foreign pension and investment accounts

- Joint foreign accounts and accounts with signature authority

- Foreign mutual fund or similar financial accounts where those accounts qualify

FBAR answers one question: Did the taxpayer have reportable foreign financial accounts?

It does not answer: Did the taxpayer own a PFIC?

What FBAR Cannot Do for PFIC Reporting

FBAR does not:

- report PFIC income or PFIC gain

- calculate §1291 excess distributions

- make a QEF election under §1295

- make a mark-to-market election under §1296

- attach a Form 8621 calculation

- disclose whether the account holds a PFIC

If one foreign brokerage account holds five foreign ETFs, FBAR may report one account. Form 8621 may need to address each PFIC separately.

What Form 8938 Reports — and Where It Falls Short for PFICs

Form 8938 is a FATCA form filed with the U.S. income tax return. It applies to specified foreign financial assets above applicable thresholds, which vary based on filing status and whether the taxpayer lives in the United States or abroad.

Form 8938 may include:

- Foreign bank and brokerage accounts, if they are specified foreign financial assets and the Form 8938 threshold is met

- Foreign stocks held outside a financial account

- Foreign partnership interests

- Foreign trust and pension interests

- Certain foreign financial instruments

Why Form 8938 Does Not Replace Form 8621

Form 8938 may disclose that a foreign asset exists. It does not:

- calculate PFIC tax under §1291, §1295, or §1296

- make PFIC elections

- report §1291 excess distributions

- provide the annual PFIC report required under §1298(f)

A foreign ETF can be both a specified foreign financial asset for Form 8938 purposes and a PFIC requiring Form 8621. These are overlapping rules, not replacement rules.

The Form 8938 Part IV Duplication Rule — What It Means and What It Does Not Mean

There is one technical rule that causes recurring confusion.

If a PFIC is properly reported on Form 8621, the taxpayer may not need to duplicate the full asset detail again on Form 8938. Instead, the taxpayer may reference the Form 8621 in Form 8938 Part IV as an excepted specified foreign financial asset.

In plain terms: if you report a PFIC on Form 8621, you may reference that Form 8621 on Form 8938 Part IV to avoid duplicate listing. But you still have to file Form 8621.

What Form 8621 Reports: PFIC Income, Elections, and Annual Reporting

Form 8621 is the PFIC form. A U.S. person who is a direct or indirect shareholder of a PFIC may need Form 8621 if they:

- receive certain direct or indirect PFIC distributions

- recognize gain on a direct or indirect disposition of PFIC stock

- report information for a QEF election under §1295

- report information for a mark-to-market election under §1296

- make certain other PFIC elections

- are required to file an annual PFIC report under §1298(f)

This is why foreign ETFs and foreign mutual funds create a different reporting problem from ordinary foreign bank accounts.

A foreign bank account is an account. A foreign ETF is an investment vehicle. If that foreign ETF is a PFIC, the taxpayer may need Form 8621 even if the account already appears on FBAR and Form 8938.

What Triggers a Form 8621 Filing Obligation

Form 8621 may be required even without a sale. Triggers include:

- a sale or other disposition of PFIC shares

- a distribution from a PFIC (including dividends and reinvested distributions)

- making or maintaining a QEF or MTM election

- annual reporting under §1298(f) for direct or indirect PFIC ownership

Annual PFIC reporting under §1298(f) can apply to PFICs the taxpayer simply holds — even with no income event and no sale. Limited filing exceptions exist but apply in narrow circumstances.

Why Foreign ETFs and Mutual Funds Are High PFIC Risk

A direct holding of ordinary foreign company stock is not automatically a PFIC. A company must meet the PFIC income test (75% passive income) or asset test (50% passive assets) to qualify — see What Is a PFIC for details.

Foreign ETFs and mutual funds are different. They are pooled investment vehicles. They typically hold passive assets — stocks, bonds, and other financial instruments — and generate passive income. That structure makes many non-U.S. funds PFIC candidates under the PFIC tests in §1297.

Foreign Investment Vehicles with High PFIC Risk

The following investment types are commonly associated with PFIC risk for U.S. taxpayers:

- Non-U.S. ETFs of any kind

- Foreign mutual funds

- Irish-domiciled UCITS ETFs (including VWRA, VWRL, IWDA, CSPX, VUAA)

- OEICs (Open-Ended Investment Companies)

- Unit trusts

- Managed funds

- Investment trusts

- Money market funds outside the United States

- Foreign fund wrappers containing pooled investments

- Local pension and retirement funds holding pooled investments

This is why "foreign ETF" and "PFIC" appear together so frequently in U.S. expat tax discussions. The issue is structural, not incidental.

Country-Specific Examples: PFIC Risk Inside Foreign Accounts

The following examples show how the FBAR–Form 8938–Form 8621 gap plays out across common expat jurisdictions.

UK ISA and UCITS ETFs: When Tax-Free Accounts Create U.S. PFIC Exposure

A UK Stocks and Shares ISA may hold Irish-domiciled UCITS ETFs, OEICs, investment trusts, or other non-U.S. funds. The ISA is tax-free in the United Kingdom. That does not make it tax-free or PFIC-exempt for U.S. tax purposes.

The ISA is the account wrapper. The UCITS ETF inside the ISA is the investment. FBAR and Form 8938 may capture the ISA. Form 8621 may still be required for each PFIC held inside the ISA.

👉 See the full guide: UK ISA and SIPP PFIC Guide

Canada TFSA and Canadian ETFs: The PFIC Risk Inside a Tax-Free Account

A Canadian TFSA may hold Canadian ETFs or mutual funds. For U.S. tax purposes, the TFSA tax-free status does not automatically extend to U.S. reporting. If the TFSA holds foreign funds that qualify as PFICs, Form 8621 may still be required.

👉 See the full guide: Canada TFSA and RRSP PFIC Guide

Australia Super and Managed Funds: Account Disclosure Is Not Enough

Australian superannuation funds and managed fund structures often require detailed U.S. tax analysis. The U.S. result depends on the legal structure, account type, and underlying investments. FBAR or Form 8938 may disclose the account. They do not resolve the PFIC question for managed funds held inside the Super structure.

👉 See the full guide: Australia Super PFIC Guide

New Zealand KiwiSaver and PIE Funds

KiwiSaver and PIE fund investments can create PFIC reporting questions for U.S. citizens, green card holders, and U.S. tax residents. Local New Zealand tax treatment does not control the U.S. PFIC result.

👉 See the full guide: New Zealand KiwiSaver PFIC Guide

Japan NISA and Local Investment Trusts

A Japanese NISA may hold Japanese investment trusts, local funds, or non-U.S. ETFs. The NISA tax benefit in Japan does not remove U.S. reporting obligations. If the account holds PFIC investments, Form 8621 may apply regardless of the NISA wrapper.

👉 See the full guide: Japan NISA PFIC Guide

Taiwan ETFs and Indian Mutual Funds

Taiwan ETFs and Indian mutual funds are common PFIC risk areas for U.S. taxpayers with holdings in those markets. Reporting the local brokerage account on FBAR is the starting point — not the end point. Each fund inside the account requires a separate PFIC analysis.

👉 Related guides: Taiwan ETF PFIC Guide · India Mutual Fund PFIC Guide

Three-Layer Review: How to Check a Foreign Account Before Filing

Use this structured workflow to assess foreign account reporting requirements before filing or amending a return.

Layer 1 — Account Disclosure (FBAR and Form 8938)

Ask:

- Is this a foreign bank account, brokerage account, or investment account?

- Did aggregate foreign account value exceed $10,000 at any point?

- Does the account count toward Form 8938 thresholds?

This layer determines FBAR and Form 8938 obligations.

Layer 2 — Asset Identification (PFIC Risk Screen)

Ask:

- What is inside the account?

- Is it cash, or is it an investment vehicle?

- Is it ordinary company stock, or a pooled fund?

- Is it a foreign ETF, mutual fund, UCITS ETF, unit trust, managed fund, or similar vehicle?

- Is it a pension or retirement fund with pooled investments?

This layer identifies PFIC risk and determines whether Form 8621 analysis is required.

Layer 3 — PFIC Calculation (Form 8621)

Ask:

- Was there a sale or disposition?

- Was there a distribution (including reinvested distributions)?

- Is mark-to-market available and was an election made?

- Is QEF available and was an election made?

- Does §1291 apply as the default regime?

- Is annual reporting under §1298(f) required?

- Does a separate Form 8621 need to be filed for each PFIC?

This layer determines the Form 8621 filing requirement and the correct calculation method.

What Happens If Form 8621 Is Missed: PFIC Tax, Interest, and Statute Risk

A missing Form 8621 is not equivalent to a missing FBAR. The risk profile is different and often worse.

PFIC Tax, §6621 Interest, and Missed Election Timing

A missing Form 8621 can leave the following issues unresolved:

- Unreported PFIC tax under the default §1291 regime

- Unreported §6621 interest charges on deferred PFIC tax

- Lost or delayed QEF election opportunities, unless late-election relief is available

- Lost or delayed mark-to-market election opportunities, unless late-election relief is available

- Incomplete annual PFIC reporting under §1298(f)

- Missing historical basis, distribution, and election data

- Statute-of-limitations exposure under §6501(c)(8)

Why PFIC Cleanup Becomes More Expensive Every Year

Late PFIC remediation requires reconstructing the full holding period from the original acquisition date. That reconstruction requires:

- Original purchase dates and purchase prices

- All sale dates and sale proceeds

- All distributions (cash and reinvested)

- Foreign exchange rates at each event date

- Year-end fair market values for MTM elections

- Prior-year calculations and prior-year election history

Records become harder to obtain with each passing year. Brokers may not retain older transaction history. This is why PFIC cleanup is typically more expensive — and more technically risky — after several years of missed filings.

Practical Checklist: When to Check for Form 8621 Before Filing

Review PFIC exposure if you hold any of the following:

- Foreign ETFs of any domicile

- Foreign mutual funds

- Irish-domiciled UCITS ETFs

- Unit trusts

- OEICs

- Managed funds

- Investment trusts

- Money market funds outside the United States

- Local pension funds with pooled investments

- ISA, TFSA, Super, KiwiSaver, NISA, CPF, or similar accounts holding funds

Be especially careful if:

- you sold a foreign fund in the tax year

- you received distributions from a foreign fund

- dividends were automatically reinvested

- you are entering Streamlined Filing

- your CPA or EA asked for Form 8621 data

- you were quoted a per-fund PFIC fee

- your foreign broker did not issue a Form 1099

- you have several years of old foreign fund history

If any of these apply, do not stop at FBAR or Form 8938. Check Form 8621 separately.

The Simple Rule for U.S. Expats with Foreign Accounts

If you only have foreign bank accounts with cash, FBAR and Form 8938 may cover the main obligations.

If you have foreign brokerage accounts, check the holdings list.

If the holdings list includes a foreign ETF, foreign mutual fund, or other pooled investment vehicle, check PFIC.

If a PFIC is present, check Form 8621 before assuming the return is complete.

FBAR reports the account. Form 8938 reports the asset. Form 8621 reports the PFIC. All three can apply at once. None of them replaces the others.

FAQ: FBAR, Form 8938, Form 8621, and Foreign ETF PFIC Reporting

Is FBAR the same as Form 8938?

Is Form 8938 the same as Form 8621?

If I filed FBAR, do I still need Form 8621?

If I filed Form 8938, do I still need Form 8621?

Are foreign ETFs PFICs?

Are Irish-domiciled UCITS ETFs PFICs?

Does a tax-free ISA, TFSA, Super, KiwiSaver, or NISA avoid PFIC?

Do I need one Form 8621 per account or per fund?

What if I never sold the foreign ETF?

Does Form 8938 Part IV mean I can skip Form 8621?

What should I check first if I think I have a PFIC?

Official Sources and Reference Links

- 🔗 FinCEN FBAR Filing: BSA E-Filing System — FinCEN Form 114

- 🔗 IRS FBAR Overview: IRS.gov — FBAR

- 🔗 IRS Form 8938 Overview: IRS.gov — FATCA and Form 8938

- 🔗 IRS Form 8938 Filing Thresholds: IRS.gov — Who Must File Form 8938

- 🔗 IRS Instructions for Form 8938: Instructions for Form 8938 (PDF)

- 🔗 IRS Form 8621: Official IRS Form 8621 (PDF)

- 🔗 IRS Instructions for Form 8621: Instructions for Form 8621 (PDF)

- ⚖️ IRC §6501(c)(8) — Open Statute: law.cornell.edu — §6501

Recommended Reading

- 🔗 What Is a PFIC? IRC §1297 Income and Asset Tests

- 🔗 Form 8621 Filing Exemption Rules

- 🔗 Streamlined Filing and Late Form 8621

- 🔗 §1291 vs MTM vs QEF: PFIC Election Comparison

- 🔗 Form 8621 Line 16a Statement Guide

- 🔗 Missed vs Defective Form 8621 Filing

- 🔗 UK ISA and SIPP PFIC Guide

- 🔗 Canada TFSA and RRSP PFIC Guide

- 🔗 Australia Super PFIC Guide

- 🔗 New Zealand KiwiSaver PFIC Guide

- 🔗 Japan NISA PFIC Guide

- 🔗 Taiwan ETF PFIC Guide

- 🔗 India Mutual Fund PFIC Guide

- 🔗 EA vs CPA vs Tax Attorney for PFIC and FBAR

Current as of May 2026 · Based on Form 8621 (Rev. 12/2025)