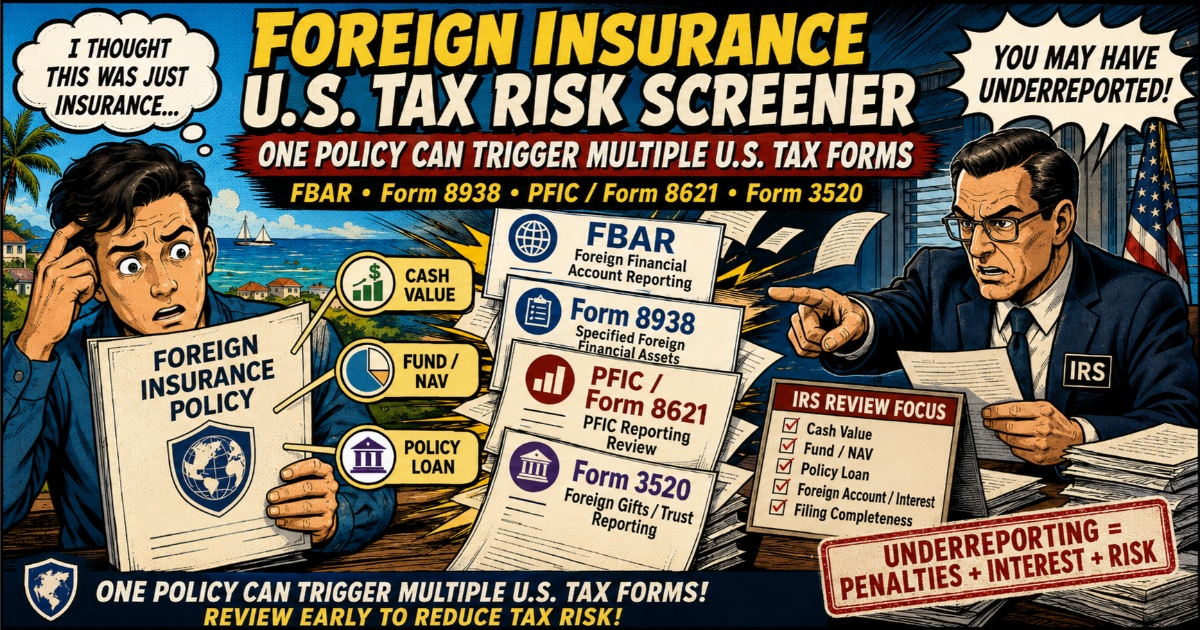

How to Interpret Possible U.S. Reporting Results

The result separates PFIC / Form 8621, FBAR, and Form 8938 into three scores. Use the table below to connect the result to likely follow-up review areas.

| Screener signal | Possible U.S. item | Why it matters |

|---|---|---|

| Cash surrender value / surrender value / policy value | FBAR, Form 8938 | A foreign-issued life insurance or annuity contract with cash value may be reportable if thresholds are met. |

| Account value / fund value / policy value | FBAR, Form 8938, manual review | Account value may mean the policy is more than pure protection and requires the annual statement and policy structure. |

| Fund / unit / NAV / ETF / unit trust / sub-account | Form 8621 / PFIC review | These terms may indicate indirect exposure to non-U.S. pooled investment vehicles. |

| Ability to select or switch funds | Form 8621 / PFIC review | Policyholder or adviser investment control is a high-review signal for investment-linked insurance. |

| Partial withdrawal / surrender / cash dividend | Income tax treatment, possible Form 8621 | Taxable income, gain, dividend, PFIC excess distribution, or other treatment may need review. |

| Policy loan | Income tax treatment, manual review | Policy loan treatment can differ depending on policy structure and U.S. tax characterization. |

| Unclear product type or unclear policy value | Manual review | The policy may need additional review if cash value, account value, fund value, or investment-linked features cannot be confirmed. |

Why U.S. Taxpayers Often Miss Foreign Life Insurance Reporting

U.S. tax residents report worldwide income and certain foreign financial assets. A pure protection term policy is usually lower risk, but a policy with cash value, surrender value, dividends, account value, or investment-linked funds may enter U.S. asset reporting and income tax review.

Many taxpayers separate "insurance" from "investments" in everyday language. U.S. tax reporting looks past the marketing label. Indian ULIPs, Hong Kong ILAS, Singapore ILPs, China investment-linked policies, Malaysia investment-linked insurance, UK offshore bonds, Canada segregated fund policies, and similar products may all need closer review when they show account value, fund units, NAV, or fund-switching rights.

Foreign Life Insurance with Cash Surrender Value: FBAR and Form 8938

A foreign life insurance or annuity contract with cash value may need to be included in FBAR or Form 8938 threshold analysis. FBAR looks at whether aggregate foreign financial accounts exceeded USD 10,000 at any time during the year. Form 8938 looks at specified foreign financial assets and applies different thresholds depending on residence and filing status.

This is why cash surrender value, surrender value, policy value, account value, and fund value are not just insurance terms. Even when PFIC risk is low, a cash-value policy may still raise FBAR, Form 8938, income, surrender, dividend, bonus, or policy loan questions.

Investment-Linked Foreign Insurance, PFIC Risk, and Form 8621

If a foreign insurance policy contains fund choices, units, NAV, unit trusts, ETFs, mutual funds, sub-accounts, or fund-switching rights, it should not be reviewed only as ordinary insurance. It may require analysis of indirect PFIC exposure and Form 8621 reporting risk.

Form 8621 focuses on whether a U.S. person is treated as a direct or indirect PFIC shareholder in relevant situations. Investment-linked policies, ILPs, ILAS, ULIPs, offshore bonds, and fund-linked insurance wrappers deserve more careful review than ordinary savings policies.

ILAS, ILP, ULIP, Offshore Bonds, and Segregated Fund Policies

Product names vary by country, but the screening logic is similar: cash value, account value, fund units, NAV, sub-accounts, investment options, or fund switching.

Common Foreign Insurance Terms That May Trigger U.S. Tax Review

| Region | Common foreign insurance terms |

|---|---|

| India | ULIP, Unit Linked Insurance Plan, LIC-linked policy, pension plan, money-back policy, fund value. |

| Hong Kong | ILAS, Investment-Linked Assurance Scheme, fund switching, policy value, account value, terminal bonus. |

| Singapore | ILP, investment-linked policy, sub-fund, unit trust, fund value, premium holiday. |

| Malaysia | Investment-linked insurance, investment-linked takaful, ILP, unit fund, fund switching. |

| UK / Canada / Australia | Offshore bond, investment bond, segregated fund policy, insurance bond, unit-linked life policy, with-profits value. |

Foreign Life Insurance U.S. Tax Reporting FAQ

Do I need to report foreign life insurance with cash surrender value?

Is cash value life insurance reportable on FBAR?

Is a foreign annuity reportable on FBAR or Form 8938?

Does a foreign insurance policy with fund value require Form 8621?

Are offshore bonds PFICs for U.S. tax purposes?

Is an investment-linked insurance policy a PFIC?

What is the difference between FBAR, Form 8938, and Form 8621 for foreign insurance?

Is an Indian ULIP a PFIC?

Is a Hong Kong ILAS policy a PFIC?

Is a Singapore ILP a PFIC?

Related PFIC and Form 8621 Guides

- What Is a PFIC?

- FBAR vs Form 8938 vs Form 8621

- Can I File Form 8621 Myself? DIY PFIC Calculation Guide

- India PFIC and Form 8621 Guide

- Hong Kong PFIC, MPF, Unit Trusts and Form 8621 Guide

- Singapore PFIC and Form 8621 Guide

Current as of May 2026 · Based on Form 8621 (Rev. 12/2025)