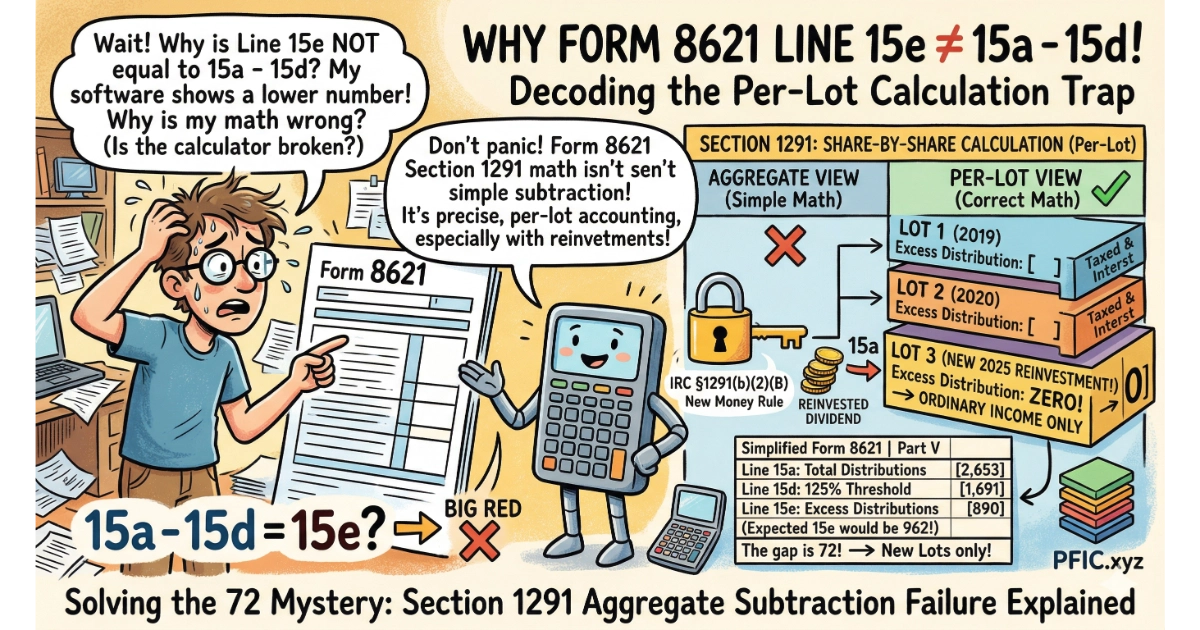

Is an Aggregated 15a − 15d Difference a Calculation Error?

When preparing PFIC workpapers under the Section 1291 (Excess Distribution) method, users often perform a quick "sanity check" on the aggregate summary numbers. A common point of confusion arises when:

— Reddit DIY User

Most practitioners assume that as long as Line 15a is greater than the 125% threshold (Line 15d), the excess distribution (15e) should equal the difference (15a - 15d).

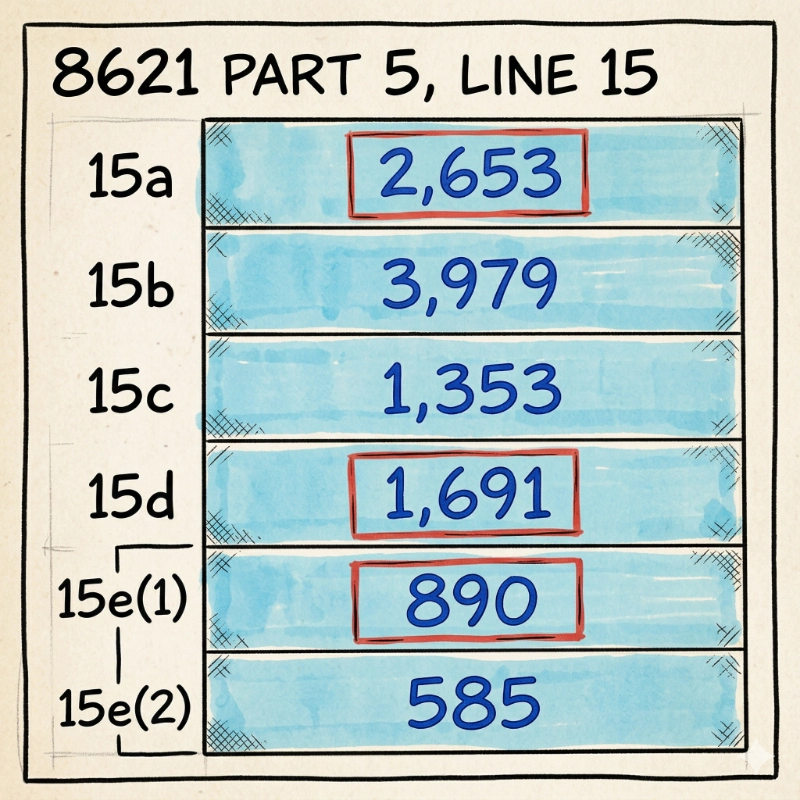

- Line 15a: 2,653 (Total Distributions)

- Line 15d: 1,691 (125% Threshold)

- Line 15e: 890 (Actual Excess Distribution)

- The "Expected" 15e: 2,653 - 1,691 = 962

Observed Discrepancy: 2,653 - 1,691 ≠ 890

Math Check: 962 (Expected) - 890 (Actual Result) = 72 gap

By using this specific user's anonymized case study, we will perform a detailed calculation to uncover the root cause of this 72 discrepancy and determine whether it truly stems from a calculation error.

Form 8621 Line 15e Discrepancy: The "72 Gap" Audit Trail

The taxpayer's 2025 Section 1291 report is based on the following audit trail:

- 2019–2024 (Legacy Lots): 37 prior-year transactions (purchases or reinvestments) constituting the core holding lots.

- 2025 (Current Year): Only 4 new reinvestment transactions within the 2025 tax year.

| Date | Details | Shares | Value (AUD) |

|---|---|---|---|

| 03/27/2025 | Reinvestment | 147.9984 | 149.73 |

| 06/30/2025 | Reinvestment | 1279.0221 | 1297.44 |

| 09/25/2025 | Reinvestment | 130.7071 | 137.53 |

| 12/11/2025 | Reinvestment | 1043.3946 | 1067.81 |

| Total Portfolio Distribution (Line 15a) | 2,653 |

How PFIC Reinvestment Affects Section 1291 Calculations

Dividend reinvestments are among the most complex transactions in Section 1291 accounting. They function as simultaneous events: a taxable distribution is received, followed immediately by the purchase of new shares.

Under Prop. Reg. § 1.1291-2(e)(1), each holding-period lot must be tested separately; excess distribution amounts are then allocated/apportioned under §1291 mechanics. You cannot simply aggregate multiple distributions received on different dates into a single annual sum for testing.

In this case study, multiple same-year reinvestments create a cascading calculation nightmare: the June distribution is allocated to original shares plus the March lot; the September distribution covers original holdings plus the March and June additions; and the December distribution includes all three prior lots. Managing this level of granularity is exhausting, but this is precisely what 8621calculator.com handles in the background.

PFIC Per-Lot Allocation vs Aggregate Calculation

The discrepancy between aggregate math and reported totals is not a calculation error; it is a strict adherence to federal tax law. While Form 8621 only asks for summary totals in Part V, the underlying Section 1291 math must be separated by the holding period of every single share you own.

1. Statutory Authority: IRC §1291(b)(3)(A)

"determinations under this subsection shall be made on a share-by-share basis, except that shares with the same holding period may be aggregated,"

Legal Source: 26 U.S. Code §1291 (Cornell LII)

2. Regulatory Authority: Proposed Treasury Regulation § 1.1291-3(a)

"Gain is determined on a share-by-share basis."

Official Source: Federal Register (Apr 15, 1992)

Summary: Under Section 1291 and associated Treasury Regulations, even shares of the same fund must be treated as distinct "lots" if they have different purchase dates. Each lot must undergo its own 125% threshold test and calculate its own Excess Distribution. Aggregating shares with different holding periods generally does not align with the per-lot approach required under Section 1291.

Why the "72 Gap" Is Not a Form 8621 Line 15e Calculation Error

"(B) No excess for 1st year. — The total excess distributions with respect to any stock shall be zero for the taxable year in which the taxpayer's holding period in such stock begins."

This means §1291(b)(2)(B) directly prevents current-year acquired lots from producing excess distributions for the taxable year in which the holding period begins. The 72 "gap" in our case is the distribution amount allocated to these brand-new lots, not a simple arithmetic failure in the Form 8621 Part V summary.

Official Source: 26 U.S. Code §1291(b)(2)(B) (Cornell LII)

Line 15a (Total Distribution): For shares newly acquired through reinvestment in 2025 (the current tax year), the holding period in "prior years" is zero. Accordingly, 100% of the distribution allocated to these “new” shares is reported here.

Line 15d (125% Threshold): Since these specific lots have no history prior to the current year, there are no preceding three years to average. Thus, the average distribution amount for these lots (the threshold buffer) is mathematically zero.

Line 15e (Excess Distribution): Under IRC §1291(b)(2)(B), the total excess distribution is legally mandated to be zero for the year in which the taxpayer's holding period begins. (For current-year acquired lots, Line 15e cannot equal 15a minus 15d; it MUST be zero.)

Form 8621 Line 15e Math: Step-by-Step Per-Lot Breakdown

As shown in the technical audit trail (Table 1), the distributions allocated to these 2025 "newly acquired" shares total 71.66 (rounded to 72 on the official form).

| Dist Date | Lot Origin (Aquired In) | Holding Days | Dist/Share | Line 15a | Line 15d | Line 15e |

|---|---|---|---|---|---|---|

| 06/30/2025 | Allocated to 1st Reinv. (Mar) | 95 | 0.047400 | 7.0151 | 0 | 0 |

| 09/25/2025 | Allocated to 1st Reinv. (Mar) | 182 | 0.004800 | 0.7104 | 0 | 0 |

| 09/25/2025 | Allocated to 2nd Reinv. (Jun) | 87 | 0.004800 | 6.1395 | 0 | 0 |

| 12/11/2025 | Allocated to 1st Reinv. (Mar) | 259 | 0.037100 | 5.4908 | 0 | 0 |

| 12/11/2025 | Allocated to 2nd Reinv. (Jun) | 164 | 0.037100 | 47.4519 | 0 | 0 |

| 12/11/2025 | Allocated to 3rd Reinv. (Sep) | 77 | 0.037100 | 4.8492 | 0 | 0 |

| Aggregate 15a (New 2025 Lots Only): | 71.6569 | (This sum explains the discrepancy) | ||||

Table 1: Underlying Lot-Level Audit Trail — the $71.66 of "New Money" distribution is the missing link that explains why aggregate workpaper subtraction does not match aggregate excess distribution.

Download the technical lot-level simulation data used in this guide:

Download Lot-Level Excel Simulation (.xlsx)

Because the 72 attributed to the 2025 purchases is purely ordinary income (as there was no holding period prior to the current year), it effectively "soaks up" part of the 15a total without ever touching Line 15e.

If you have multiple dividend reinvestments within the tax year — or multiple new acquisitions prior to those distributions — a workpaper that simply nets total 15a support against total 15d support may be mathematically imprecise. We suggest using 8621Calculator.com for a meticulous lot-level cross-check to verify your results and ensure audit compliance.

Key Takeaway for PFIC Form 8621 Line 15

The math on your Form 8621 Part V is not "broken"; it is simply reflecting the reality of multi-lot accounting.

- Aggregate 15a support - aggregate 15d support = aggregate excess distribution only works cleanly if all shares were held prior to the current tax year.

- If you bought shares or reinvested dividends during the year, your aggregate excess distribution may be lower than the "expected" aggregate subtraction because those new shares are legally barred from generating an excess distribution.

8621Calculator.com prioritizes mathematical transparency, striving to ensure that every figure on your Form 8621 is traceable and derivable from your underlying transaction records—meeting the meticulous lot-level reporting standards required for Section 1291 compliance.

Most DIY attempts fail because PFIC Section 1291 requires lot-level tracking.

If you want a correct calculation with audit-ready workpapers and Line 16a substantiation:

Use the Professional PFIC Report (Price of 2 cups of coffee) ›

Generate compliant Part V summary totals with underlying cost basis layers automatically.

Form 8621 Line 15e FAQ

Why can aggregated PFIC workpaper 15a minus 15d differ from reported excess distribution?

Under Section 1291, excess distribution determinations can be made on a share-by-share or holding-period lot basis, and current-year acquired shares can be barred from producing excess distributions.

What causes the aggregate difference?

If part of total distributions is allocated to shares acquired during the current tax year, Section 1291(b)(2)(B) can require that excess distributions for those shares be zero.

Legal References

- 🔗 IRC §1291(b)(2)(B): Adjustments for holding period and the first-year no-excess rule.