This is a worked PFIC §1291 dividend excess distribution calculation example for Form 8621. The taxpayer received a $2,000 PFIC dividend in 2024 after prior-year dividends of $90, $100, and $110. This case shows how the 125% excess distribution test works, how Form 8621 Line 15e and Line 15f are computed, and how the excess amount is allocated by day to prior PFIC years for the Line 16 tax and §6621 interest calculation.

1. PFIC Dividend Excess Distribution Calculation Example for a Dividend: Facts

Taxpayer: U.S. person, no QEF or MTM elections made.

Initial acquisition: 2019-09-05 — one single PFIC block purchased.

Tax year filed: 2024.

Key event: A large $2,000 dividend received on 2024-05-05.

The PFIC transaction table on the right is a teaching ledger — a simplified, modelled dataset built solely to demonstrate the §1291 mechanics (the 125% excess distribution test, holding-period allocation, and interest calculation). Under the statute, only the distributions from 2021, 2022, and 2023 enter the §1291 125% excess distribution test; earlier dividends remain part of the timeline but are excluded from the threshold calculation.

| Date | Details | Units | Value |

|---|---|---|---|

| 2019-09-05 | Purchase | 1000 | $10,000 |

| 2019-10-15 | Dividend | 0 | $70 |

| 2020-06-15 | Dividend | 0 | $80 |

| 2021-06-15 | Dividend | 0 | $90 |

| 2022-06-15 | Dividend | 0 | $100 |

| 2023-06-15 | Dividend | 0 | $110 |

| 2024-05-05 | Dividend | 0 | $2,000 |

Form 8621 Line Mapping for This Dividend Example

| Form 8621 Line | Amount | Meaning |

|---|---|---|

| Line 15a | $2,000 | Total PFIC distribution received in 2024 |

| Line 15b | $300 | Prior 3-year distributions total ($90 + $100 + $110) |

| Line 15c | $100 | Average prior 3-year distribution |

| Line 15d | $125 | 125% threshold ($100 × 1.25) |

| Line 15e | $125 | Non-excess distribution |

| Line 15f | $1,875 | Excess distribution ($2,000 - $125) |

| Line 16a statement | $1,875 | Daily allocation and interest schedule |

2. Step 1 — Form 8621 Line 15b: Prior 3-Year Distribution Average

This step is the PFIC prior 3-year average distribution calculation used for Form 8621 Line 15b and Line 15c. The first calculation requires compiling prior year distributions. Prior dividends are: 2021: $90, 2022: $100, and 2023: $110. The sum of prior distributions is $300, which is reported on Form 8621 Line 15b. Under Line 15c, the average is calculated as $300 ÷ 3 = $100.

For a detailed breakdown of how to track and compile these historical amounts, refer to the Form 8621 Line 15b Prior Year Distributions Guide.

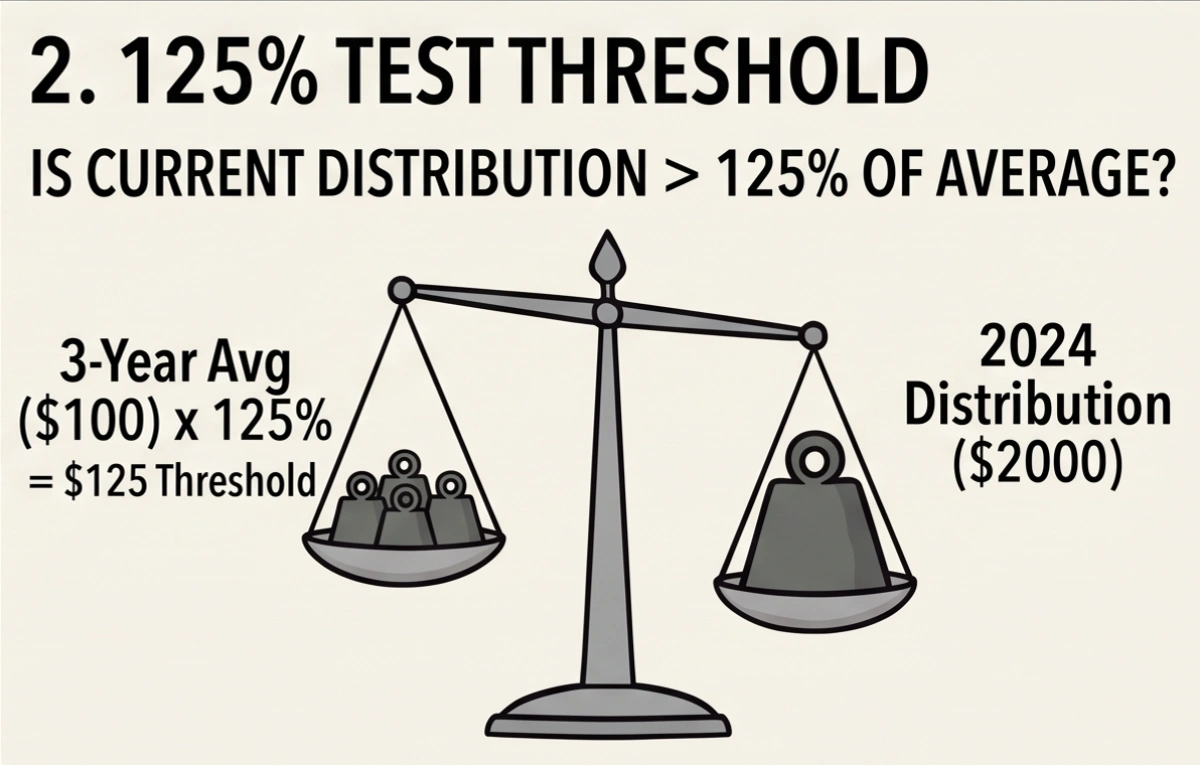

3. Step 2 — Form 8621 Line 15d: 125% Excess Distribution Test

Multiply the 3-year average by 125% to find the threshold: $100 × 1.25 = $125. This is entered on Form 8621 Line 15d. The current year distribution is $2,000 (entered on Line 15a).

The first step in preparing Form 8621 Part V is determining if the current year distribution exceeds the statutory threshold.

125% threshold (Line 15d) = 100 × 1.25 = 125

4. Step 3 — Form 8621 Line 15e and 15f: Non-Excess vs Excess Distribution

The distribution is split into:

- Non-excess portion (amount up to 125% threshold): $125, reported on Line 15e.

- Excess portion (amount exceeding the threshold): $2,000 - $125 = $1,875, reported on Line 15f.

The non-excess portion ($125) represents the amount up to the 125% threshold and is treated as a normal dividend on Line 15e. To understand the calculations, netting rules, and reporting requirements for this non-excess income, see the Form 8621 Line 15e Guide.

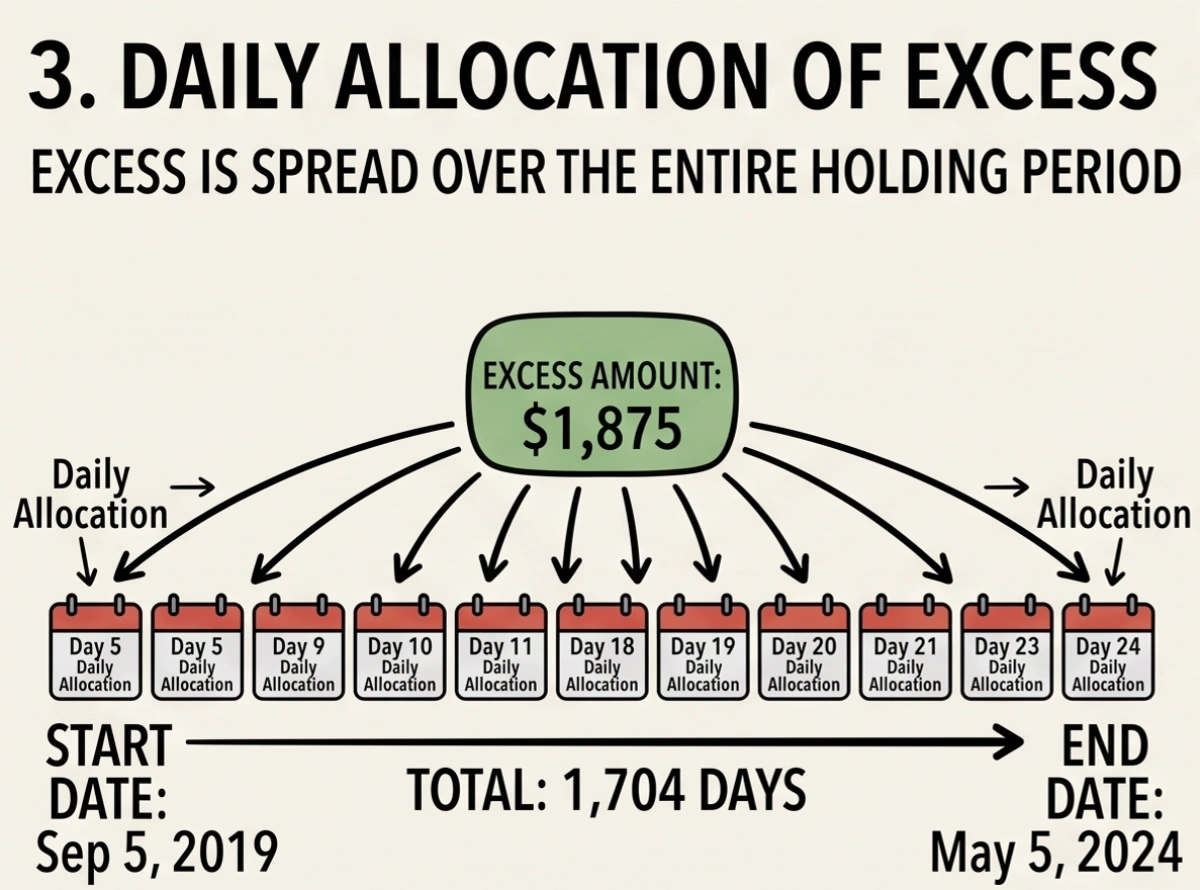

5. Step 4 — Form 8621 Line 16: Daily Allocation of the Excess Distribution

Under §1291, the excess portion ($1,875) is not assigned evenly by tax year — it must be allocated strictly by days held. This is a frequent source of calculation errors.

Holding period determination: 2019-09-05 → 2024-05-05.

Total days held: 1,704

⚠️ Crucial Practitioner Note: Counting both the acquisition and distribution dates yields 1,705 days, which is incorrect under IRC §1223 principles. The holding period begins the day after acquisition. This precise day count drives the entire allocation percentage.

- IRC §1223 — holding period begins the day after acquisition.

- §1291(c)(1)(A) — excess distributions are allocated over each day the PFIC stock was held, including the distribution date.

Daily excess distribution amount: $1,875 ÷ 1,704 days ≈ $1.10035 per day

| Year | Days Held | Excess per Day | Allocation % | Allocated Excess (Form 8621 Line 16) | Tax Treatment |

|---|---|---|---|---|---|

| 2019 | 117 | $1.10035 | 6.9% | $128.74 | Prior year (Throwback) |

| 2020 | 366 | $1.10035 | 21.5% | $402.73 | Prior year (Throwback) |

| 2021 | 365 | $1.10035 | 21.4% | $401.63 | Prior year (Throwback) |

| 2022 | 365 | $1.10035 | 21.4% | $401.63 | Prior year (Throwback) |

| 2023 | 365 | $1.10035 | 21.4% | $401.63 | Prior year (Throwback) |

| 2024 | 126 | $1.10035 | 7.4% | $138.64 | Current year (Ordinary Income) |

| 2024 | — | — | — | $125.00 | Current year (Non-excess) |

| Total | 1,704 days | $1.10035/day | 100% | $1,875.00 |

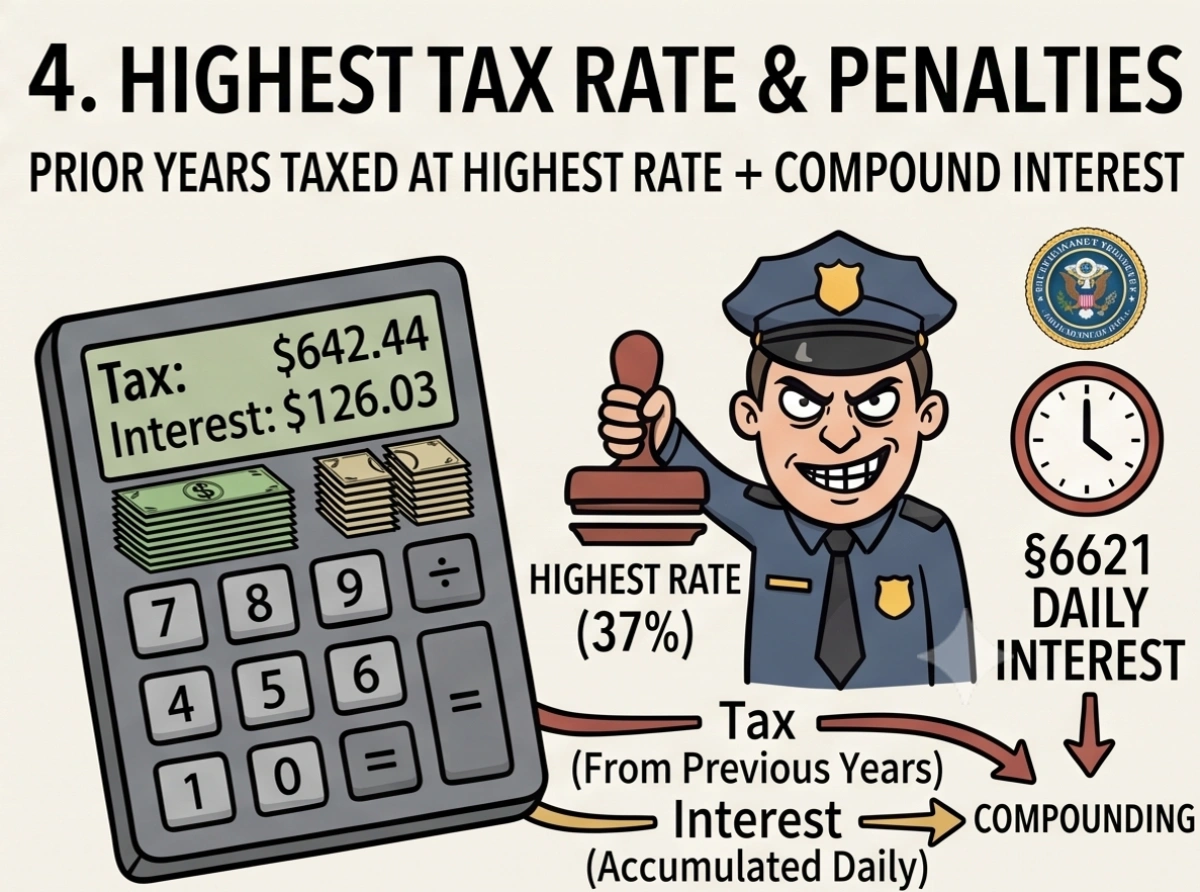

6. Step 5 — §1291 Throwback Tax and IRC §6621 Interest

The "throwback" amounts allocated to prior years are not taxed at the taxpayer's actual historical rate. Instead, §1291 mandates the use of:

- The highest federal marginal income tax rate applicable for that specific prior year (e.g., 37% for individuals in recent years), AND

- Mandatory interest under IRC §6621, compounded daily from the due date of the prior year's return.

This is why §1291 liabilities frequently exceed the income itself — the tax is only the starting point, and the accumulated §6621 interest penalty can be substantial.

| Year | Allocated Amount (from Step 2) | Mandatory Top Rate | Tax Liability | §6621 Interest (Daily Compounded) | Total Due per Year |

|---|---|---|---|---|---|

| 2019 | $128.74 | 37% | $47.63 | $14.96 | $62.59 |

| 2020 | $402.73 | 37% | $149.01 | $40.23 | $189.24 |

| 2021 | $401.63 | 37% | $148.60 | $34.47 | $183.07 |

| 2022 | $401.63 | 37% | $148.60 | $24.48 | $173.08 |

| 2023 | $401.63 | 37% | $148.60 | $11.89 | $160.49 |

| Total Form 8621 Liability for this Distribution | $642.44 | $126.03 | $768.47 | ||

7. Common Form 8621 Line 15b Mistake: Using Raw Cash Dividends in the Next-Year Baseline

A common Form 8621 Line 15b mistake is using the raw cash dividend distribution amount for future calculations. Only the portion of the 2024 distribution that is actually included in 2024 taxable income flows into the next year’s three-year baseline (Line 15b). This PFIC prior distributions calculation is a key compliance check.

The remainder—allocated to prior years and subject to §6621 interest—is not treated as a 2024 distribution and is therefore strictly prohibited from being included in the baseline for future years.

| 2024 Amount | Source | Included in 2024 Income? | Included in Future 125% Baseline? |

|---|---|---|---|

| $125.00 | Non-excess distribution (Line 15e) | ✅ Yes | ✅ Yes |

| $138.64 | Current-year portion of excess distribution | ✅ Yes | ✅ Yes |

| $1,736.36 | Prior-year allocated excess (subject to top rate + §6621 interest) |

❌ No | ❌ No |

| $263.64 | Total includable PFIC income for 2024 baseline | ✅ Yes | ✅ Yes |

Therefore, when performing the 2025 §1291 excess-distribution test, the correct three-year baseline must be:

| Year | Incorrect Method (uses raw cash received) |

Correct Method (uses only includable income) |

|---|---|---|

| 2022 | $100 ✅ | $100 ✅ |

| 2023 | $110 ✅ | $110 ✅ |

| 2024 Baseline | $2,000 ❌ (Wrong) | $263.64 ✅ (Correct) |

| Line 15b — Total | $2,210.00 ❌ | $473.64 ✅ |

| Line 15c — 3-year average | $736.67 ❌ | $157.88 ✅ |

| Line 15d — 125% threshold | $920.83 ❌ | $197.35 ✅ |

For the full §1291 Line 16 mechanics beyond this dividend example, see the PFIC §1291 excess distribution calculation guide.

8. Why Real PFIC Dividend Cases Become Harder with DRIP and Multiple Lots

The case study above models the easiest possible PFIC scenario: one single purchase block and one distribution per year. There were no additional buys, no dividend reinvestments (DRIPs), no partial sales, and no multi-currency issues.

Real PFIC accounts rarely look like this. Once a taxpayer dollar-cost averages, reinvests dividends monthly, or sells only part of a position, §1291 calculations must be performed separately for every single tax lot (block).

Consider a standard mutual fund where dividends are reinvested monthly for 10 years. That single holding creates:

- 1 original acquisition block

- + 120 new monthly reinvestment blocks (each with its own holding period start date)

- = 121 distinct tax lots requiring individual tracking.

When a subsequent excess distribution occurs, the §1291 engine must compute 121 separate daily holding period allocations, track 121 separate includable income histories for future baselines, and calculate interest on 121 separate schedules. This is why manual Excel spreadsheets fail for real-world PFICs.

9. PFIC Dividend vs PFIC Sale: Why the 125% Test Applies Only to Dividends

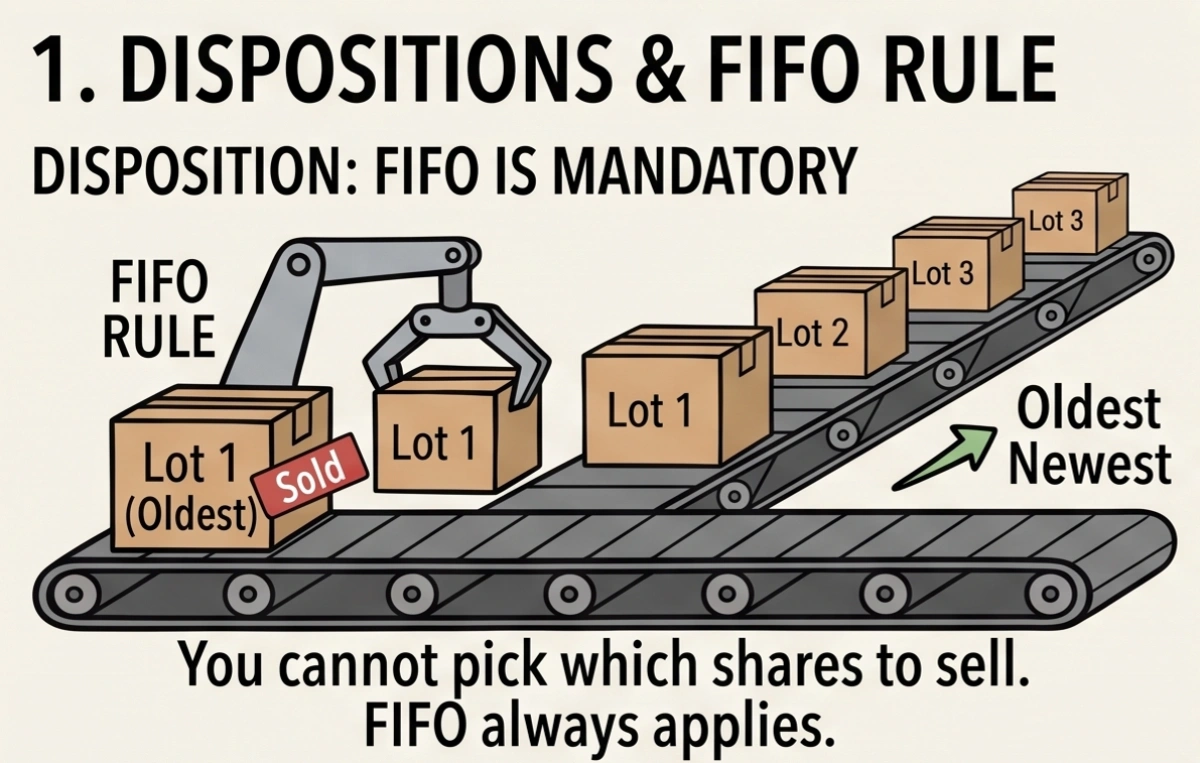

Disposing of a PFIC via sale or redemption is mechanically different than analyzing a dividend. Under IRC §1291(a)(2), the entire gain realized on the disposition is treated as an excess distribution. The 125% threshold test does not apply to dispositions. This article does not compute a sale case. For a worked disposition example, see the separate PFIC §1291 sale excess distribution example.

Crucially, the regulations require strict First-In, First-Out (FIFO) ordering (Treas. Reg. §1.1291-1(b)(7)(ii)) to determine which blocks are sold. You cannot use specific identification. Once multiple lots exist, accurately tracking gains, holding periods, and basis under mandatory FIFO in Excel becomes unmanageable.

Why Excel Fails for PFIC §1291 — The Four Levels of Spreadsheet Breakdown →

Form 8621 §1291 Dividend Excess Distribution FAQ

What is a PFIC dividend excess distribution?

How is the 125% PFIC excess distribution test calculated?

Is a PFIC dividend always an excess distribution?

Does Form 8621 Line 15b use raw cash dividends?

Does the 125% test apply to PFIC sales?

What is the difference between a PFIC dividend excess distribution and a PFIC sale excess distribution?

How is a PFIC excess distribution allocated to prior years?

Why is §6621 interest charged on PFIC excess distributions?

Sources

- IRS: About Form 8621.

- IRS: Instructions for Form 8621.

- IRS: IRS Form 8621 PDF.

- Cornell Law (LII): 26 U.S. Code § 1291 — Interest on Excess Distributions.

- Cornell Law (LII): 26 U.S. Code § 6621 — Determination of Rate of Interest.

- Cornell Law (LII): Treas. Reg. § 1.1291-1 — Taxation of U.S. persons that are shareholders of PFICs.

- Cornell Law (LII): Treas. Reg. § 1.1291-2 — Taxation on distributions by PFICs.

- IRS: Quarterly Interest Rates (IRC §6621).

Related Form 8621 Calculation Guides

- Can I File Form 8621 Myself? DIY PFIC Calculation Guide

- Form 8621 Line 16a Statement Example

- §1291 Interest Calculation for Form 8621 Line 16f

- PFIC Foreign Currency Translation Rules for Form 8621

- PFIC Tax and Form 8621 Rules

Current as of May 2026 · Based on Form 8621 (Rev. 12/2025)